UPDATE – Posted April 15, 2014 – Cash Store Financial Services Inc. Files for Bankruptcy Protection

The Cash Store’s problems continue, as they have now filed for bankruptcy protection (under the CCAA, a form of bankruptcy protection used by large corporations). They are now likely to be de-listed from the Toronto Stock Exchange. The Cash Store will apparently “stay open for business”, but that will not include making loans in Ontario, which they are currently prevented from offering.

Original Post – February 18, 2014:

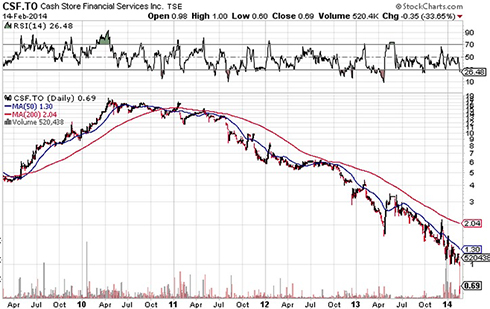

You don’t need to be a stock market analyst to understand the severity of the current financial state of Cash Store Financial Services Inc. As you can see from the chart below, Cash Store shares have dropped from around $19 in early 2010 to a low of 60 cents on Friday. That’s a big drop.

Cash Store payday loan lender struggling under new rulings

The only payday loan lender listed on the Toronto Stock Exchange, the Cash Store operates 510 branches across Canada under the “Cash Store Financial” and “Instaloans” brands.

What happened?

Payday lending has become a less profitable business due to recent legislative changes. Payday lenders are limited in what they can charge (no more than $21 for every $100 payday loan), and they are no longer permitted to continually “roll over” a loan. This happens when the borrower pays off one loan by taking out a new loan.

To counter this new legislation, Cash Store began offering short term lines of credit, in the hopes that these types of loans would not be subject to the payday loan rules. The Province of Ontario took a different position however claiming that despite the name change, debtors were effectively using these as payday loans.

Basically, Cash Store Financial has come under the microscope of the Province of Ontario. This began with a charge, and subsequent guilty plea by Cash Store, to operating as payday lenders without a license in Ontario. Then the province made a claim that these new ‘lines of credit’ were effectively payday loans in disguise.

The Ontario Superior Court of Justice agreed with the Ministry of Consumer Services and in a ruling released on February 12 prohibited them from acting as a loan broker in respect of its basic line of credit product without a broker’s license under the Payday Loans Act, 2008 (the “Payday Loans Act”).

The Province is taking this one step further by stating that they want to deny new licenses to Cash Store Financial Services. According to a recent press release:

“the Registrar of the Ministry of Consumer Services in Ontario has issued a proposal to refuse to issue a license to the Company’s subsidiaries, The Cash Store Inc. and Instaloans Inc. under the Payday Loans Act, 2008 (the “Payday Loans Act”). The Payday Loans Act provides that applicants are entitled to a hearing before the License Appeal Tribunal in respect of a proposal by the Registrar to refuse to issue a license. The Cash Store Inc. and Instaloans Inc. will be requesting a hearing.”

It would appear that, for now, the Cash Store is not permitted to offer any payday loan or line of credit products in Ontario.

So what’s my take on this?

I am not a fan of payday loans. They are very expensive. Even with the new rules, a payday lender can still charge you $15 for every $100 you borrow, so over a two week loan that’s almost 390% in annual interest.

I’m pleased that the government is enforcing the rules, but I don’t think you need the government to protect you from payday lenders. You can protect yourself, quite easily, by following this one simple step: Never take out a payday loan.

If you have a short term cash crunch, talk to your creditors about deferring your payment until the next payday; that’s a lot cheaper than paying 390% interest.

If you have more debts than you can handle and you are already on the payday loan treadmill, give us a call immediately, and we’ll show you how to get help with payday loans and get off the payday loan hamster wheel.

I wanted to know in regards to all of the articles on the cash store, if you have a loan with them, are you required to pay them back, if they are in this situation?

Legally, yes, just because your lender is having problems that does not mean that you can avoid the loan. Even if they went out of business they could sell their loan portfolio to another lender, who would have the right to collect on it. So, if you can afford to deal with the loan, you should. If you can’t pay it back, and/or if you have other loans, you should give our office a call to consider your options.

Are you a lawyer? Reason i ask is because i find it very hard to believe that a company that was convicted of operating without a payday lender license can call it a legal loan in the first place and secondly since the judgement that the line of credit was in fact the same as a payday loan all loans give after the conviction in November a not worth the paper they are wrote on which is why they are not charging customers any interest on them now. If you read their collection policy and carefully read how it is written you will see what i am talking about. Remember this is a bankruptcy firm site. They make money if you file bankruptcy so they will not give all of the facts as they have a stake in this.

Hi Dave. Thanks for your comments. No, I am not a lawyer. As you correctly state I am a bankruptcy trustee, and Hoyes Michalos is a firm that does bankruptcies and consumer proposals, and you are correct that we “have a stake in this”. I’m the guy people come to when they have more payday loans than they can pay back and it causes them a lot of trouble, and that’s why I’m trying to get the word out about how payday loans work.

I don’t understand your comment that we will “not give you all of the facts”. In my follow up post on April 16: https://www.hoyes.com/blog/why-is-cash-store-filing-for-bankruptcy-protection/ I link to the 500 pages of court documents in this case, and I encourage everyone to read them.

The point is this: if you owe The Cash Store money they can attempt to collect it. In Ontario they are not currently permitted to offer new loans, which is causing them serious cash flow problems, necessitating their application for bankruptcy protection.

Can a payday loan company publish their judgement if they win in small claims court? For example, put the person’s name and photo on the wall of their store or in their window?

Hi William. A judgment is a matter of public record, so if a creditor obtains a judgment in court, it does appear in court records, and on the debtor’s credit report.

I’m not a lawyer, so I can give you an authoritative answer on your question about posting someone’s name and photo on the wall of their store or window, but I would assume that doing so would violate privacy laws, and would probably be considered a form of harassment, unless the debtor agreed in advance to that treatment.

I for one am happy to see them go, I’m sorry that people are out of work but this company should be out of business. I think you make a lot of very good points on Payday Loans and Bankruptcy issues for people who take out these loans. I’m working on getting Predatory Lending laws in Canada, I believe its well overdue.

In one of the articles I read you mentioned the percentage of people who filed for Bankruptcy who had taken out Payday Loans. I wonder if you have any numbers on people who may have taken out loans with Companies such as Citifinancial, Wells Fargo etc., I am sure a lot of people that you helped were victims of these Companies and their predatory ways.

Hi Donna. You are correct that all lenders that have high interest rates cause problems. We see it with payday loan companies, and with finance companies. It is a significant percentage of people with debt who have these high interest loans. We are working on updating our xxx study so stay tuned for more detailed numbers.

Hi Doug, I live in BC and had a loan with Cash Store.

My account was transferred over to Money Mart. I ended up paying my account at Money Mart and also full amount of my loan from Cash Store.

Money Mart felt sorry for me and gave me the full amount back and my loan with them which is my whole pay cheque. I am on OAS & CPP so very little money to live on…It is like I am on a treadmill!

Could you advise me as to a better way to go? My bank will not lend me money.

Thank you

Hi Marion. The correct strategy for you will depend on your circumstances. On a limited income you could simply offer your creditors a set amount each month, based on what you can afford. You could advise them that you can’t afford to pay anything and stop paying them. They can’t garnishee your wages (because you don’t have any), but they can still pursue you for the money. You could also file bankruptcy. Here is a link to bankruptcy trustees in British Columbia who could meet with you (for free) to help you make your decision.