Whenever I meet with someone to discuss filing bankruptcy or consumer proposal one of the questions I ask is, “do you bank where you owe money?”. If the answer is yes, I strongly advise that they open a new bank account before going bankrupt or filing a consumer proposal, at a bank where they have never done business or had credit card debt.

Let me make this clear, if you bank at a financial institution where you owe money, there is a really good chance that they will freeze your bank account when they get the bankruptcy or consumer proposal papers.

Once your bank account is frozen your car payment and rent cheque will bounce.

I consider it so important to open a new chequing account that we provide a tip sheet on how to open a new account and why this is important.

Click to read a printable pdf version of our fact sheet below.

Yes, this is a lot of work, but consider that the bank can take money from your account if you don’t make the switch. You need to make sure that they can’t put through charges to your bank account after your bankruptcy or consumer proposal starts. This is money you need for your rent, utilities and groceries; you don’t want to put that at risk.

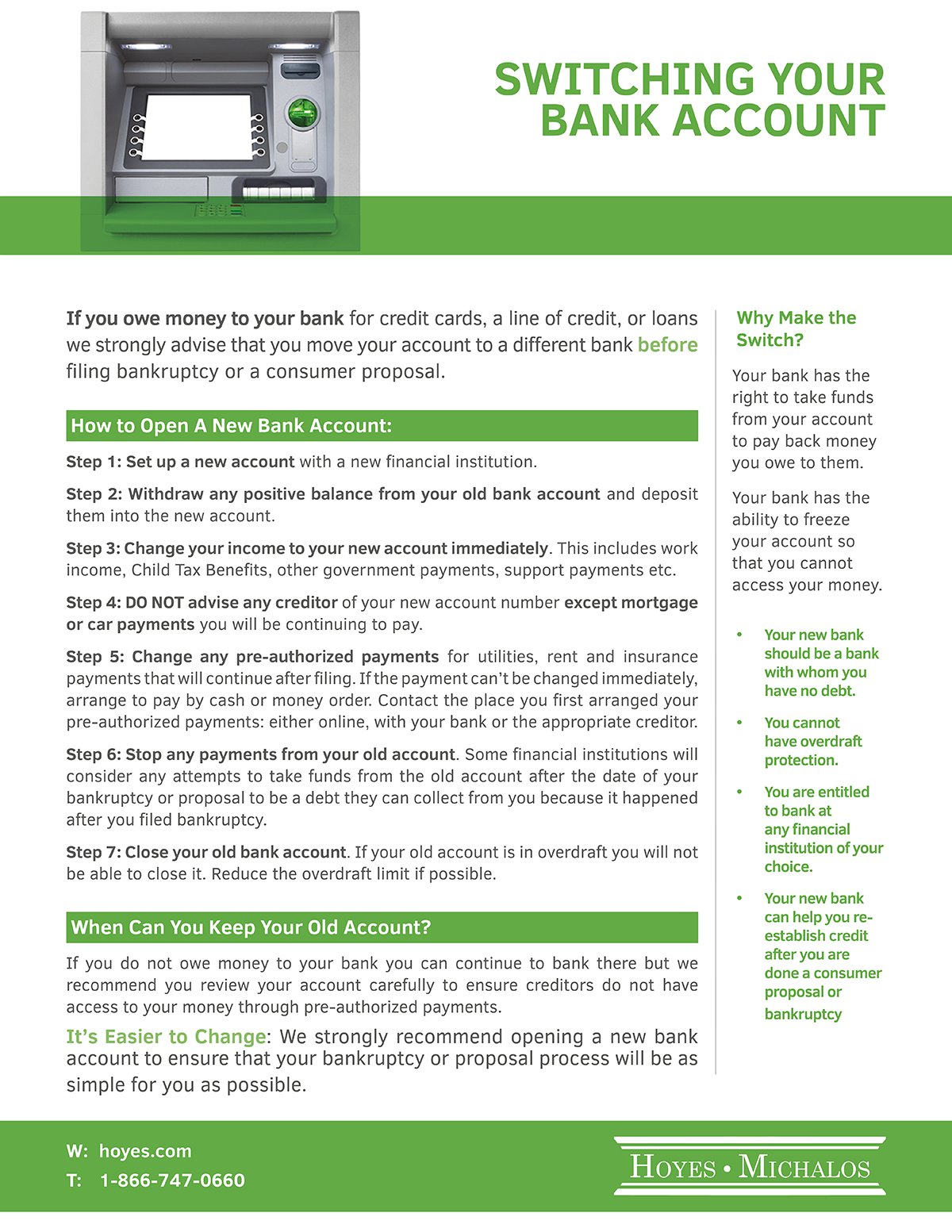

Step 1: Set up a new account with a new financial institution.

Step 2: Withdraw any positive balance from your old bank account and deposit them into the new account.

Step 3: Change your income to your new account immediately. This includes work income, Child Tax Benefits, other government payments, support payments etc.

Step 4: DO NOT advise any creditor of your new account number, except mortgage or car payments you will be continuing to pay.

Step 5: Change any pre-authorized payments for utilities, rent and insurance payments that will continue after filing. If the payment can’t be changed immediately, arrange to pay by cash or money order. Contact the place where you first arranged your pre-authorized payments: either online, with your bank or the appropriate creditor.

Step 6: Stop any payments from your old account. Some financial institutions will consider any attempts to take funds from the old account after the date of your bankruptcy or proposal to be a debt they can collect from you because it happened after you filed bankruptcy.

Step 7: Close your old bank account. If your old account is in overdraft you will not be able to close it. Reduce the overdraft limit if possible.

If you bank where you have a credit card or other debt, it is very easy for the bank to take the payment from your account if you don’t make the payment on time. Even another bank where you owe money can debit your account if you have given them permission to do so.

Opening a new account may be a hassle because you have many expenses automated for your convenience. It will take time to contact everyone to switch over all of the expenses in your account, but the change will let you keep better control of your money.

Yes, I understand you really like your bank and have been there for years, but if someone at the bank forgets to tell the computer not to take money from your bank account, bankruptcy or a consumer proposal will not stop it since the computer could debit your account without your knowledge. We do notify your creditors promptly about your bankruptcy or proposal, but it will take time for the notifications to reach the right people and for their changes to take effect in the banking computer systems. Once such a non-permitted transaction is discovered, your bankruptcy trustee can apply to court to get the money back, but that may take days or even weeks. In the meantime, your rent cheque has bounced and you can’t buy groceries.

But how do I close my account if I am in overdraft?

You can’t. You just have to make sure that no more charges go through that account. The overdraft becomes a debt that is included in your bankruptcy or consumer proposal.

Since overdraft is a form of credit, you can’t have overdraft protection on your new bank account. To ensure that you don’t overdraw your balance after bankruptcy, create a budget that will help to ensure that you are able to meet all of your bills going forward.

To make the point clear- Protect yourself, get a new bank account!!

Which bank should I pick?

Here’s how you pick a new bank:

- As discussed above, it has to be a bank where you don’t owe any money.

- If you get paid by cheque, because you are a new customer, your new bank will likely put a 10 day hold on all deposits. (You may be able to reduce or eliminate the hold period by making the deposit with a teller, and not at the machine). If possible, bank at the same bank your employer uses, because it’s easier for the bank teller to instantly clear your cheque (without a hold period), because they can see that there is enough money in your employer’s bank account. After you have deposited a few paycheques you can ask the bank to remove the hold on your deposits.

- If you get paid electronically (most people do), you can pick a “virtual” bank like Tangerine or Simplii Financial. They don’t have branches, but most of their services are free, so you can minimize service charges by using an on-line bank.

NOTE: We don’t endorse or recommend any bank, so ask about services and service charges before you decide on which bank to use.

If you are considering a consumer proposal or bankruptcy as a way to eliminate your debt, contact us to book a free, no-obligation consultation at your nearest Hoyes Michalos location. We’ll review your debts and your banking arrangements and help you make a plan that will eliminate your debt.

I’m looking at several options at the moment, including bankruptcy. I currently bank with CIBC and have credit with them, so I’ve opened an account with PC financial as per the advice in the article. What I’m wondering is whether CIBC can tap into PC Financial, as it is an affiliate bank.

Can you advise?

Hi Stacey. As a general rule, if you formerly banked with CIBC we do NOT recommend banking with PC Financial, since you are correct, they are owned by CIBC. I am not aware of any case where CIBC took money out of a PC Financial account; operationally they are two separate banks. However, since there are many banks to choose from, we believe that out of an abundance of caution if you have debt with CIBC you should open your new account somewhere other than CIBC.

The following statement below is from the bankruptcy-canada.com website:

“There is a common misconception that payday loans cannot be included in a personal bankruptcy or consumer proposal. This is absolutely false.

The first step is to close the compromised bank account.”

I’m in Ontario. If a person has a current payday loan that needs to be repaid, I thought that closing the bank account was fraud. You’ve signed documents giving them permission to debit your bank account so if you intentionally close the bank account you’re not making the money available to them.

Hi Kathryn. It is not fraud to close your own bank account. If you have a payday loan or any other debt that you cannot pay, and you are considering filing a consumer proposal or bankruptcy, or advice is as follows:

1. Meet with a licensed trustee to review your options. If a consumer proposal or bankruptcy is the option you decide, then:

2. Open a new bank account at a new bank, where you have no debts, and notify your sources of income (employer, the government, etc.) of your new bank account so that your direct deposit paycheque goes to the correct account.

3. Once your income is transferred to the new account, you should close the old bank account so that no creditor has access to it.

4. When you file your bankruptcy or consumer proposal we will notify all of the creditors, and they will then communicate with us.

It generally takes creditors a few days or longer to process your bankruptcy or consumer proposal and shut off the automatic payments they have programmed. That’s why closing the bank account is essential protection for you. If you leave money in that bank account they may continue to take payments even after the bankruptcy has started.