Now that the Ontario government has restricted debt advisors from charging up-front fees before completing a settlement with creditors, many debt relief companies are switching their business tactics. What they now offer is so called consumer debtor protection services, debt assistance or consumer proposal referral programs.

Table of Contents

What is consumer debtor protection and what are they selling?

There are varying levels of disclosure about exactly what services are offered by these different debt help companies. What they propose is to help you eliminate your debt through some form of debt repayment program. This however is where things get a little cloudy. In almost all cases what they are selling is a consumer proposal and what they really offer is a consumer proposal referral program.

Some debt assistance companies are a little clearer in what they say they do, some a little less.

- The may be up front admitting that they have a consumer proposal representation program.

- Others are just advertising ‘government programs’ that can help you reduce your debts by up to 70% without admitting they really mean proposals through the Bankruptcy & Insolvency Act.

- The last group advertise consumer proposals, yet they are not licensed to administer such a program and do not make that clear.

What typically happens when you contact one of these debt help companies is you work with a debt manager or debt advisor, often over the phone, who will talk to you about your finances then have you sign a contract for their services. The person you are speaking to is more than likely a salesperson, whose job is to get you to sign on the dotted line and agree to make payments before going further.

What they do:

- They will ask you to sign a contract before doing any real work.

- They may or may not help you prepare a budget.

- They may or may not talk to you about all your debt relief options.

- They will ask you to complete various forms which provide the information necessary to complete the consumer proposal documentation required by the federal government to file a consumer proposal.

- One you have completed your paperwork AND you have paid all their fees, they will refer you to a licensed insolvency trustee.

In other words they are charging fees to manage the preparing of your debt proposal file, nothing more.

Can debt assistance advisors negotiate a better deal for you?

Here’s the funny part. All of the steps in the previous section (with the exception of the upfront fee contract) from reviewing your budget and financial situation, to helping you review all your options, and preparing the paperwork will be done by a licensed insolvency trustee for free.

So since your trustee will help you prepare the documentation at no charge, that begs the question, can these debtor assistance companies protect you by negotiating lower debt repayments?

First of all let’s start with the idea that the debt counsellor you are dealing with is negotiating with your creditors. In almost all cases they are not. They may look at your situation and help you decide how much you can afford to offer your creditors however that’s not necessarily worth the large fees they charge, especially when a trustee will do this anyway.

But wait, these debt assistance companies often say the trustee won’t negotiate on your behalf and that they are there to protect the debtor’s interests. While it’s true a licensed insolvency trustee represents the interest of all parties in a consumer proposal, including creditors and debtors, a reputable trustee will not negotiate a proposal that won’t work or make you file bankruptcy if that’s not the right solution. If you think they do either of those, get a second opinion – from another licensed insolvency trustee.

There are two criteria that need to be met when you offer your creditors a consumer proposal to reduce your total debt:

- You need to offer the people you owe as much money (or more) than they would be entitled to receive if you were to file an assignment in bankruptcy; and

- You need to offer the people you owe enough money to agree to the deal.

The first criteria is a mathematical exercise. It is based on your income, family size, and the things that you own. Your debts don’t actually factor into the cost of filing bankruptcy.

The second criteria is a bit more fluid – you need to offer the people you owe enough money that they are willing to accept the deal. You’d think that as long as you offer more than they’d get in a bankruptcy that would be enough, but it is not. The major Canadian banks and credit companies have unofficially agreed that they expect a minimum of 30% of what you owe as a proposal offer. It is possible to offer less, but unless you have very special circumstances, they won’t accept anything less.

Offering a lowball proposal, or one with strange terms, can actually harm your situation, not protect you. The creditors may ask for even greater terms, or worse, vote down the proposal meaning you are no longer protected from the actions of your creditors. They will now begin calling for payment or pursuing legal action.

What to look for in debtor assistance ads and what is misleading.

There are typical terms and wording that you should be aware of that can help you identify who these types of unlicensed debt providers are.

- Consumer Proposal Representation Program. This is fancy language for we will charge you to fill out the paperwork.

- Bankruptcy trustees are mandated to represent your creditors’ best interests. This is not true. Licensed Insolvency Trustees are Officers of the Court and have a duty of care to all stakeholders

- Trustees must maximize the amount paid to your creditors. Similar to the point above and this is not entirely true. Trustees have an interest in assuring that the proposal will be successful. That means all parties, debtor and creditors, must be satisfied.

- Stay of proceedings. Anything that mentions stopping wage garnishments, credit calls or legal actions means they are referring to a program under the Bankruptcy & Insolvency Act, which can only be filed by a licensed insolvency trustee.

- Assistance in submitting a consumer proposal – this is a fee for service business to help you fill out the paperwork.

- Federal Government legislated option or program – the only federal debt relief programs are a bankruptcy or consumer proposal through a licensed insolvency trustee.

- We are not trustees in bankruptcy – my favourite, at least they are admitting they are not licensed.

Read Online Reviews and Complaints

If you come across any of these consumer debtor protection style ads, I recommend you do more research about how the company operates, including online reviews and complaints including those with the Better Business Bureau.

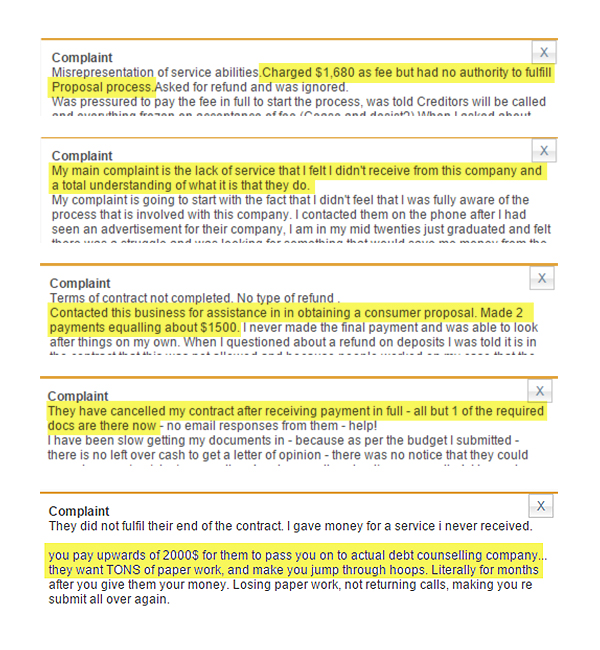

Here is a portion of just a few online complaints we quickly found for these types of debt help companies which highlight the lack of protection and service they can provide:

As you can see, the fees for this type of debtor assistance can be quite high. This more often than not would negate any potential savings they may be able to recommend to the licensed insolvency trustee when negotiating the terms of a successful proposal. More often than not, you will actually end up paying more.

What is also concerning in these reviews is that many of their clients did not understand the services offered, and did not know they were just paying to be referred to a trustee.

If you need protection from your creditors, your best legal option in Canada is a bankruptcy or consumer proposal.

My recommendation is that if you are considering making a proposal to your creditors, contact a licensed insolvency trustee directly. To be sure that the agency you turn to for debt assistance or advice is trustworthy:

- Do a reputation check.

- Make sure they are trained and certified

- Make sure they are licensed and accredited to provide the services they are selling

- Protect yourself by confirming they are a licensed insolvency trustee. Search their name, or the name of the company, with the Office of the Superintendent of Bankruptcy.

Another great resource for consumer protection information is the Financial Consumer Agency of Canada’s article “Debt reduction companies: Beware of too good to be true offers”.

It is in your best interest to know who you are dealing with and what exactly they are offering. Never sign a contract without doing a thorough investigation and review first.