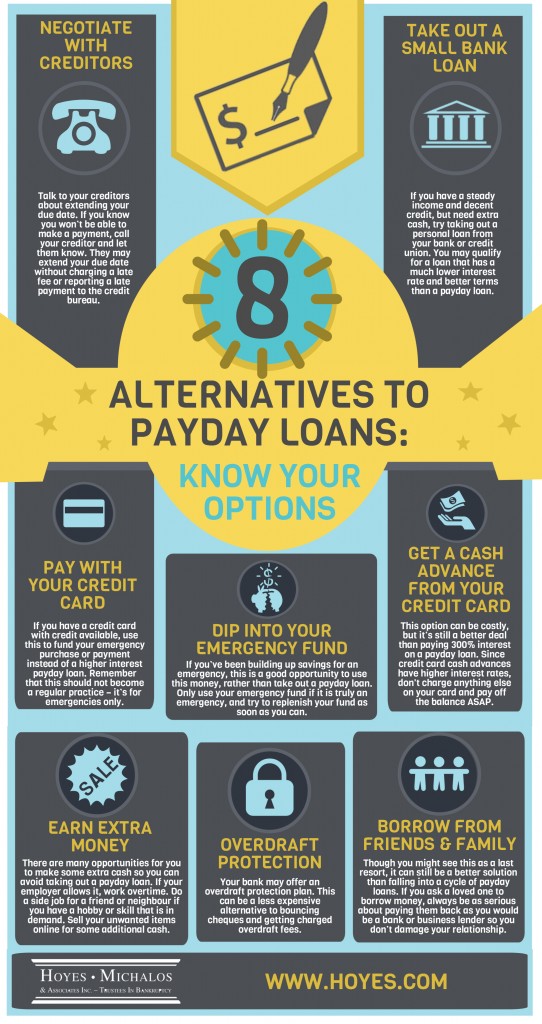

There are many reasons why someone would file for personal bankruptcy in Canada as a means of dealing with their debts and getting a fresh start, but there are equally good arguments not to declare bankruptcy.

Here are 5 common reasons why bankruptcy may not be your best choice and why you might want to avoid bankruptcy:

- Bankruptcy would be too costly – Costs of a personal bankruptcy are based on assets and income. From an asset stand point, equity in a house, multiple vehicles, RESP’s, and contributions to RRSP’s in last 12 months are a few assets that must be realized by a bankruptcy trustee. As for income, individuals have to pay surplus income based on what they earn over the course of the bankruptcy. This could be as long as 21 months if a filing bankruptcy for the first time. In this case, if you still need relief from overwhelming debt issues, an alternative would be a consumer proposal. Consumer proposals are governed by the same laws as personal bankruptcy, but protect assets and income through a monthly payment over a maximum period of 60 months. These consumer proposals are still filed with a trustee in bankruptcy though.

- You’re not insolvent – Being “insolvent” means that an individual cannot pay debts as they become due. It also means debts could be paid in full if assets were sold. For example, if someone has $100,000 equity in their house even if they have $60,000 in credit cards and lines of credit, they are considered to be solvent. In this example, they could remortgage, obtain a bank loan or consider a debt management plan as alternatives to dealing with the $60,000 in unsecured debts.

- Prior bankruptcy filed – A first time bankruptcy runs for 9 or 21 months based on income, where as a second time bankruptcy will last for 24 or 36 months. Also a second time bankruptcy stays on a credit report for 14 years. A third or more bankruptcy requires a court hearing and will likely be longer than 36 months. If someone needs protection from their creditors and to deal with their debts but wants to avoid a multiple bankruptcy, again, a consumer proposal is an effective alternative.

- Judgement Proof – There are limits on what creditors can do to a person’s financial situation so protection from creditors without a bankruptcy in place is possible. If someone is only receiving pension income or employment insurance and they have no significant assets, their wages likely cannot be garnished by a creditor. Bankruptcy is filed to protect someone from losing assets and having their wages taken by a creditor. If you don’t have any assets or income that can be garnished, then you are considered ‘judgement proof’. Filing bankruptcy may not be necessary except for emotional reasons (you just don’t want to deal with the stress or calls).

- Professional and Personal Reasons – For some people they feel that a personal bankruptcy will be too emotional and that there is a stigma attached in which they cannot handle. Certain professions such as a lawyer, accountant, and bankers have rules where bankruptcy may be a consideration to their continued employment, but for most people there is no impact on their job. As for credit rating, there are set rules on how a bankruptcy is reported on a credit report. Consider the pros and cons of a bankruptcy or consumer proposal appearing on your report to the impact that clearing up your debts will have on your future credit potential.

Bankruptcy is a last resort option. No matter what your situation, it’s important to factor in all of the pros and cons of filing bankruptcy so you make the choice that is right for you. Contact us today for a free consultation so we can explore all your debt relief options and give you a plan to be debt free.