A consumer proposal in Canada is a negotiated debt settlement arrangement made between a debtor and his creditors through a licensed Consumer Proposal Administrator under the Bankruptcy and Insolvency Act.

So what happens when two people are liable to repay the same debt?

It is possible for two people to file a joint consumer proposal to deal with debt. Whether or not you need to depends on the answers to a few questions.

Are you both in debt?

Do you both need relief from your debts?

Is a consumer proposal the right solution for both of you?

Let’s deal with some basics first.

What is a Joint Consumer Proposal?

Consumer proposals may be filed jointly by more than one person as long as all or substantially all of their debts are similar.

To understand this definition we need to look at two factors: similar and substantially.

Similar can be interpreted as meaning that both parties are liable to repay the same debt. So if both a husband and a wife have co-signed on a bank loan or have joint names on a credit card, they each owe that debt.

Substantially is a bit trickier. The law doesn’t actually define exactly what substantially is, but it has been interpreted to mean 90% of their debts are the same. This 90% rule is not strictly enforced – it is more of a guideline but essentially it would only make sense to file a consumer proposal together to deal with combined or joint debts.

For example, John and Mary are married. John owes $40,000 in credit cards and other debts. Mary is joint on $20,000 of the debts and has another $2,000 in her own debts. 90% of Mary’s debt is similar to John’s so they are eligible to file jointly.

owe more than $1,000 to their creditors (even as a co-borrower),

be unable or unwilling to pay their debts as they come due,

have assets (the things that they own) that if sold, wouldn’t pay off their debts.

Advantages and Disadvantages

Should you file a joint proposal?

No one can be forced to file a consumer proposal. Even if you are married and one spouse decides to file, the other spouse is free to file or not, depending on their own decision.

There are two main advantages to filing a joint consumer proposal:

The debt limit to file a consumer proposal is increased to $500,000 for a joint proposal, from $250,000 for an individual (excluding any mortgages on a principal residence).

Some costs can be saved and therefore more money may be available to offer the creditors increasing the chances of success while keeping your payments affordable.

The downsides of filing jointly:

a record of having filed a consumer proposal will appear on both parties credit report so you both will find your ability to borrow limited for a period of time;

both persons are responsible for making the full payment (it’s like another joint obligation). So if one person doesn’t make the payment, the other must or the proposal will be annulled once you miss 3 payments.

Possible Scenarios

The only way to decide whether or not you should file jointly is to consider what makes the most sense for the family and their creditors. Each case is different and whomever you are working with to deal with your debts should walk you through all possible options.

While the most common approach when debts are substantially the same between spouses is to file a joint consumer proposal we have seen cases where:

One spouse files a proposal and the other keeps doing what they have always done.

One spouse files a proposal and the other files bankruptcy.

Both spouses file their own proposals because that’s what makes the most sense for them.

Do you both need to file a consumer proposal? Maybe, but you don’t have to. At the end of the day each of you should do what makes the most sense for you and for the family. Contact us today to book a free consultation so we can help you review the pros and cons of each alternative for both of you.

I’d like to tell you about someone who came to talk to me about filing a consumer proposal. I’ll call him Paul (not his real name). What makes this an interesting story is that at his initial consultation meeting Paul had some very good questions about what we do, in particular how a consumer proposal administrator compared to other debt advisors. Quite frankly I could tell that he had done his homework. It was a good lesson in how to interview anyone who you are considering talking to for advice about managing your debt.

What is a Consumer Proposal Administrator?

A consumer proposal administrator is someone who is responsible for the administration of a Consumer Proposal, a procedure to settle your debts filed under the Bankruptcy and Insolvency Act. A consumer proposal administrator must by law be a Licensed Insolvency Trustee. No-one else can file a consumer proposal in Canada. Other agencies may advertise consumer proposals, but they would have to refer you to a consumer proposal administrator to file one.

How Are Proposal Administrators Licensed?

Paul first asked if I was registered with OACCS, an Ontario association for credit counsellors. I explained that no, as consumer proposals administrators, we are licensed by the Office of the Superintendent of Bankruptcy. I told him he could find the name of our firm, Hoyes Michalos & Associates Inc, and my name as a trustee in their directory and that the same applied to any firm or trustee licensed to administer proposals.

Is Your Consultation Free?

He then asked how much his first meeting was going to cost and what he had to pay upfront if he decides to file a consumer proposal. I explained that the meeting was no charge, and he does not make his first payment until after signing, and filing his proposal documents with the government.

I also explained that the fees we are allowed to charge are set by the government. I also explained that the fees we get paid come out of the proposal payments. Debtors do not make any additional payments to the trustee. No upfront payments, no extra payments during the proposal. All licensed consumer proposal administrators work this way, but not all debt advisors do. You should not have to make any payments before a solution has been reached.

Check Referrals and Reviews

We then discussed the Better Business Bureau. He noticed that while we had an A+ rating, we had 1 (that is right 1) complaint filed. I knew about the complaint, so I let him know that someone who had filed a consumer proposal filed the complaint when he was unable to get credit after completing his consumer proposal. The complaint was not really about our service or about the consumer proposal, but rather the fact that they were having trouble getting credit afterwards because they had not yet re-built their credit history. We responded with the Better Business Bureau who received no reply to our comment from the complainant. Again, I was impressed that Paul looked, and asked the right question.

Check Government Warnings & Don’t Be Pressured

He let me know that he spoke with 2 debt consultants and I gave him my usual warning and directed him to read the government warnings about debt settlements. I found it interesting that he told me that one such company was calling him every few days asking him if he was getting in more debt and if he had made a decision. Talk about a pressure tactic! I told him I normally send one follow-up email just to make sure he doesn’t have other questions but that you should never feel pressured to sign up for any procedure.

If Necessary, Get A Second Opinion

Paul then told me he had a meeting with another company before making a decision. I don’t know who he is meeting with, but I told him to make sure he is dealing with a licensed consumer proposal administrator and I told him again how to search the government database. Second opinions are good, but they should come from someone reputable.

It took a few days before I heard back from Paul. That is normal, most people take around 3 weeks to make a decision. I am glad he did his research and I know he will be making a well informed decision.

It’s important to feel comfortable with the decision you make about how to deal with your debt. Paul took advantage of the fact that as trustees we offer a free no, obligation consultation and asked all the right questions. Visit our list of commonly asked consumer proposal questions for additional information.

Ellen Roseman, a columnist for the Toronto Star, author of many personal finance books, and a well known consumer advocate talks with Doug about the state of financial literacy in Canada, and Ellen is encouraged that Canada now has a Financial Literacy Leader (Jane Rooney, our guest last week).

While financial literacy programs are important, Ms. Roseman makes the point that

If I’m not in the market to buy a house, you can talk to me all you want about mortgages, but I’m not going to pay attention. You have to hit people when they are ready to listen and absorb information, which is usually when they are on the cusp of making a purchase.

Where Do We Get Advice?

You have to deliver financial information at the right moment, using a “just in time” model, which is tricky. That’s why Ellen believes that we tend to get advice from people with a vested interest: the car salesman, the banker, the mortgage broker, and the real estate agent. The problem is that, as Ms. Roseman says, “they all have skin in the game”, so consumers need to find someone to give them advice who is not biased. Ellen Roseman hopes that the Financial Literacy Leader’s new database of information will help consumers find answers to their questions from unbiased sources.

But are there unbiased sources of financial information? It’s not the banks. Ms. Roseman says:

There are too many people in the financial literacy game who are biased. People have a lot of trust in the banks. The banks are biased. They support their shareholders over their consumer’s interests. They are always trying to return more money to their shareholders. That means that a lot of their marketing is king of gimmicky.

For example, bank’s sell “balance protection insurance” on credit cards to low income Canadians. What does Ms. Roseman think of that product?

They don’t need it. It’s not a good product. It’s sold by banks very sneakily, and it doesn’t even cover your balance. It only covers your minimum payment….You’ve got to realize that banks are not your friend.

Wow.

Sadly, it’s true. Banks are not your friend, but that’s true of all businesses. Businesses exist to earn a profit, not to look out for your best interests. So where can you turn for good advice?

Ellen Roseman suggests following journalists with large media organizations, who are not usually connected to any specific financial interest. Unfortunately they tend to be writing about issues that are “trendy and hot”, so they may not have the advice you need, when you need it. She also advocates reading articles by personal finance bloggers, who are ordinary people with an interest in personal finance. Their blogs generate lots of comments, so that’s a good way to learn important financial lessons, based on the experience of ordinary Canadians.

Ellen Roseman’s Practical Tips

So Ellen’s number one tip before you make a financial decision: Google it. Do your research from many sources, so you can form your own opinion.

Tip Number Two: when researching a company, search on Google for the “company name + complaints”. If a lot of previous customers are complaining, that’s a warning sign for you.

Tip Number Three: Always ask yourself “what’s the worst case scenario?” If you are hiring a moving company, the worst case scenario is that your possessions are damaged or lost in the move, so to protect yourself take pictures of your possessions at the start of the move.

Be Alert For Scams

By considering the worst case scenario we can also be alert for scams. Seniors often fall victim to telephone and email scams. Ellen’s advice:

You must be a lot more suspicious. Never say “yes” right away. Don’t buy from a door to door salesman until you have completed your research.

It takes time, attention, and work, but if you make a mistake it may take a long time to recover.

How Can We Improve Financial Literacy in Canada?

Educate consumers to consider the downside.

When you tell people “motherhood” stuff their eyes glaze over, but if you say “look at this person’s really bad experience, this happened for these reasons, it can happen to you to if you’re not careful” at least you will get their attention.

That’s what Ellen does in her column in the Toronto Star. She tells stories to educate consumers about the downside of bad financial decisions, so we can all learn from other’s mistakes.

Explain the downside. Explain the risks. Do your research. Be suspicious. Watch your money.

Doug Hoyes: Welcome to Debt Free in 30, I’m Doug Hoyes. My guest today is Ellen Roseman, a columnist for the Toronto Star and author of many books on personal finance. It’s Financial Literacy Month, so I invited Ms. Roseman on the show and started by asking for her take on financial literacy in Canada.

Ellen Roseman: Well we finally have a financial literacy leader, this was something that came out of the taskforce on financial literacy’s report a few years ago and just took forever to get started, but Jane Rooney is in that job as of last March and she is going really quickly in terms of consulting and putting together a financial literacy strategy and she’s focusing on groups that tend to be somewhat disadvantaged.

She started with seniors, people over 65. I got some criticism from readers saying seniors are very different and it’s true, the over 65 to probably 75 are much more active and connected than the over 75, and I think that’s where the real problems lie, with the over 75 group. Now she’s looking at newcomers to Canada and Aboriginals and all this is good. So she’s going to — as well they have a database of resources, so like a central clearing house where you can find all kinds of financial literacy tools and help.

As for Canadians’ state of financial literacy, I think it’s still hit or miss. I think the learning that people in the education field are realizing is that if I’m not in the market to buy a house you could talk to me all you want about mortgages but I’m not going to pay attention, you have to hit people when they’re ready to listen and absorb information, it’s usually when they’re on the cusp of making a purchase of some kind.

So you have to be delivering it at the right moments and that can be tricky and I think that’s a good reason why most people listen to advice they get from people with a vested interest, you know the salesman, the banker, the mortgage broker, the real estate agent. Those are the ones who are giving them information during the transaction and what they need to do is say, you know they all have some skin in the game, I want to find someone who is not into this transaction who can just give me objective information.

So that’s where I’m hoping the Financial Literacy Database will help you find good objective information about you know how to pick a real estate agent, how to pick a mortgage broker, what you should know about penalties if you take a five year mortgage and then you have to break it in midstream and so on.

Doug Hoyes: Do you think that’s possible? Do you think it’s possible that there can be unbiased advice? So I understand what you’re saying, there’s going to be this database with all these resources. So let’s say that me, as a bankruptcy trustee, I write an article about your credit report and how things work on your — I have no vested interested in a credit report, I don’t sell that service, it has nothing to do with me but then do I have the expertise to be putting the information out there? Is there really anybody who is both unbiased and yet also has the expertise to advise consumers?

Ellen Roseman: Well I think that you made a good point, that there are too many people in the financial literacy education game who are biased and people have a lot of trust in the banks. The banks are fully biased, they support their shareholders over their consumer’s interests, they’re always trying to return more money to their shareholders and that means that a lot of their marketing is kind of gimmicky.

I just got a report from someone who followed a bunch of low income Canadians around and they all have balance protection insurance on their credit cards. They don’t need it, it’s not a good product, it’s sold by banks very sneakily and it doesn’t even cover your balance, it just covers your minimum payment if you get sick or if you die. You know you got to realize that banks are not your friend.

So everybody has a bias of some kind, you’re probably better off if you’re dealing with journalists who are full time employees of you know the media corporations because they’re usually not connected to any specific financial interest, but then you know they’re looking at the stuff that is trendy and hot and will score well on the internet.

I like the personal finance bloggers, there’s quite a lot of them in Canada and they are just ordinary people who took an interest in their money and started writing about it and it’s not so much what they write, it’s the fact that the popular ones get many, many comments from other people and if you go through a couple hundred comments to somebody’s blog post from other interested citizens who have taken an interest in their money you start to get a sense of the truth and you get a sense of what to look for and what questions to ask.

I was at a financial literacy conference yesterday and there was someone there who did a lot of research with Canadians about money and he said there’s a big difference between people under 50 and people over 50. The over 50 tend to trust much more and when they go for advice they will get a couple of recommendations and they will sign up right away and then they’ll put their trust in someone and they will keep that trust there until the very end, unless of course they run into problems. They trust the media as well and I get a lot of those people saying you know, “whatever you say that’s what I’m going to follow”.

So that’s not the best approach. They said people under 50 are much more sceptical, they do realize that there’s no one truth, there’s many truths and they do a lot of searching on the internet before they even start looking for a financial advisor. So they’ll go to maybe five or ten or 15 different sites and check out what’s going on and what the articles are all about and what the comments are saying and then they’ll start looking. So they’re at least comparison shopping online, which doesn’t take all that long and can really equip you much more and make you less trusting because I think in today’s world you can’t be that trusting.

The people who write to me get into trouble because they’re not that trusting and they don’t do their online research. The ones that really upset me are when they deal with companies that I know of that are just scoundrels and you know they lose their money, sometimes they can get a refund on their credit card, but they’ll write to me and they’ll say “Boy oh boy I wish I had checked your website”, because I’ve got a few of those on my website, or “I wish I’d gone online and seen that the Better Business Bureau gave them an F and then there’s an alert”.

They do it afterward, they don’t do it ahead of time and there’s lots of information on the internet. So you have to always just try to avoid that speed and impulse to you know do it quickly, get it over with and do the research ahead of time instead of later and then realize how much warning there was on the internet that you didn’t pay attention to at the time.

Doug Hoyes: So your number one tip then for people is Google, is that kind of what you’re saying?

Ellen Roseman: Yes, yes very much so. I know that for certain older people they’re not that used to the internet and it’s hard. But with a tablet it makes it so much easier and what I always put in my searchers is “company name + complaints” and that usually brings up complaints and those are worth reading. And then go to the Better Business Bureau, see what kind of grade they have, if it’s anything to do with the home go to homestars.com where they have ratings out of ten.

Go to the Ministry of Consumer Services in Ontario, they have a consumer beware list and they also have lots of information about shopping and what your rights are and just get a little bit more acquainted with the information online. There’s another interesting site, I don’t go to it often but it’s called Gripevine and it was started by Dave Carroll, who is a Canadian musician, who did this amazing YouTube video a number of years ago called United Breaks Guitars.

Where the airplane threw his guitar onto the tarmac and damaged it and then wouldn’t pay him back and he got so many views on YouTube that he became a celebrity and went around the world and now does customer service stories and did a book, and Gripevine is his idea and there’s a few of these around where they try and bring the consumer and business together online to resolve their problems. So that’s another one to look at.

Doug Hoyes: Well I’ll put those links in the show notes then because I think those are good resources. So really it’s up to me as a consumer to do my own thinking, my own research in advance. That’s the bottom line on what you’re saying.

Ellen Roseman: Yeah and you know it depends on the size of the purchase too. If it’s a $50 purchase you’re not going to put as much time into it. But I get people, like somebody wrote to me about a move where they’d been in a house for 40 years and they were taking everything out of the house and the moving company was packing it and they were moving it somewhere else and she was upset.

Well first of all this is an older woman, she got the name from friends who were happy and she said that nothing was damaged but she found that some of the items that were in her basement didn’t make it to her new place and she had no proof. She didn’t take any photos, she didn’t seem to have you know any way of proving that stuff that was in her old house didn’t move to her new house and I thought what kind of trust did she have?

You know it’s always good to try and think ahead, like the other habit of mine is to say “what’s the worst case scenario”. When I’m moving my entire household the worst case scenario is either things get damaged or they disappear so how can I avoid that, well I’ll take photos of everything. It’s not so hard you have a cell phone now with a camera and just keep photographing things.

So always think what’s the worst thing that can happen before you go ahead because especially with anything to do with your home bad things happen. So when they say “give me 100% of the money because I got to buy my supplies”, you say if I pay you a 100% I have no leverage if things go wrong and I can’t bargain with you because I paid you the entire amount so I’m going to keep my down payment as low as possible. So that kind of habit of mine helps a lot.

Doug Hoyes: Yeah those are very good pieces of advice and they’re practical things too. We’re going to take a quick break. I have a few more questions with Ellen Roseman right here on Debt Free in 30.

Segment Two

We’re back to continue my conversation with Ellen Roseman, a columnist with the Toronto Star. In the previous segment we were talking about seniors and in the whole aspect of financial literacy you mentioned that Jane Rooney in her new role this year, seniors was the first area that they focused on. You wrote an article back, I guess it was middle of October, October 21st, the title was Let’s Protect Seniors From Being Exploited.

So this is kind of the theme that you’re talking about here and as I said you know last week we had Jane Rooney on the show and she was talking about her efforts on behalf of seniors. So we know it’s a serious problem. You ended the column and the last two sentences were, “Financial literacy is crucially important, but it’s not a panacea. Let’s put money into enforcing consumer laws and protecting the vulnerable from tricksters”. So what are the things you’re worried about there, what are you advocating there?

Ellen Roseman: There’s a lot of fraud and scams aimed at seniors, both online and telemarketing. I hear those complaints all the time and every time you think that you know what the scams are, there are new ones that come up. I once spoke to a group of retired teachers and someone said “you know I was really I thought pretty smart about things but then I got this call from someone saying that they were from Microsoft and they thought my computer had problems and it could crash and I would lose my photos and I was so grateful I thought “that’s great, now you’re helping me”, and then you know that’s a well-known scam but she just hadn’t heard of it.

They’re very clever at playing on your fears and your needs and again you have to just get a lot more suspicious and if somebody calls you or sends you an email, you know never say yes right away. Hang up, do some research, ask for a phone number and call them back, sometimes they never want you to call them back so they won’t even give you a phone number, and a lot of that people come to your door as well.

There are, maybe not so much in London, but in Toronto door to door sales people are just relentless and they have all kinds of ways that they can talk their way into your house and then put something in your basement, a water heater and now they’re trying to rent you a furnace as well, which is a horrible economic proposition because you probably pay double or triple the cost of the furnace over a 15 year period.

You just have to be you know firm, say “no if I want a furnace I’ll call you back, I’ll let you know” and don’t get into any kind of a relationship with a door to door seller, a phone seller or even online. And now a lot of companies are telling you they want you to pay your bills electronically and they’ll send you an email saying your new bill is ready.

So the scammers are getting into that too and they’re pretending to be the bank or the phone company and saying “your new bill is ready and by the way your last two payments didn’t go through and click here so we can update your account”. So again just be really cautious and there are a lot of tricks going on.

Doug Hoyes: So you’ve got to be suspicious, you’ve got to be sceptical but ultimately it’s up to you because I guess really what you’re saying is there’s a new scam every day, you can’t sit around waiting for the government to protect you because the government isn’t going to be able to protect you. You really have to have your eyes open and that transcends every area of finances, right. If I’m going in for a car loan I’ve got to think about that too, maybe I’m not being scammed but I better know what the numbers are going in.

Ellen Roseman: Yes, yes exactly and do a little bit of shopping first and find out, you know, what are the various deals that you can get on car financing. It all takes time, it all takes attention, it’s no fun but if you make a mistake you know it can be so long till you dig yourself out of your mistake and if you’re not lucky it ends up on your credit record and there could be a collection agency involved.

I think the internet is still a pretty good source of scams. Often people will see free trial and it’ll be a cosmetic or a drug or vitamins and so they sign up for the free trial and then they’re told there’s just some shipping costs to Canada and they need your credit card to cover the shipping costs, which are under $10.

But then in the course of giving them your credit card they slip in some sneaky language that you probably didn’t even see saying that it’s actually a monthly subscription and there you are caught getting these monthly packages in the mail that cost about $75 or $80 each and every time you try and cancel you get a new package and it can be just horribly annoying and scary and hard to get out of. So the internet is probably a breeding ground for very many things that can take your money away.

Doug Hoyes: It’s almost as if you’re saying that if you were the head of you know financial literacy education in Canada, and I’m putting words in your mouth here but tell me if I’m wrong, you’re almost saying that it’s not just about understanding how the math works, it’s really about taking that big step back and saying I’ve got to be sceptical, I’ve got to be suspicious, not in a bad way but I’m the only one who can protect myself, no one else is going to be able to do it so yeah it’s going to take some work.

But maybe what we need to do to promote financial literacy in this country is to show everyone the downside, like you said earlier, here’s the risk of making that decision. If that’s what all our education was directed towards, here’s all the bad things that can happen if you sign that piece of paper, I wonder if that would wake people up more than having online calculators or something. I don’t know if that would work or not.

Ellen Roseman: Yeah, I agree. I think that when you tell people motherhood stuff they turn off, their eyes glaze over. But if you say look at this person’s really bad experience, this happened for these reasons it could happen to you too if you’re not careful. At least you get their attention, at least you get them reading it and tell it in the form of a story. It might be hard for the government to do that but I certainly try to do that in my column and people learn a lot they say because they remember these stories and some of them are incredible.

Like I just did one the other day about a woman who bought a car and she had a loan for the car and she was paying it faithfully and then a bailiff shows up at her door and he’s collecting for another bank and he says you know “I’ve got the paperwork that shows you in default on the loan” and she says “you’re not even my bank”. So afterwards someone said she could have fought the bailiff but she didn’t so they towed her car away.

Then it turned out that the dealer had briefly sold the car for a very short time to someone else before she had it, the person never actually took possession or anything else, but they reused the same form and the bank got confused and went after the vehicle that this woman had instead of the other woman’s vehicle. So that’s kind of stuff people remember and they just think, “what will happen if it happens to me?”

So you’ve got to be careful and you’ve got to be suspicious and you’ve got to stand up for your rights. This woman spent two days, taking time off work, just chasing the dealer and chasing the bank and trying to get them to stop selling the car at an auction, which you know she’d never get the car back and then she’d never repay the loan because she wouldn’t even have the vehicle anymore.

Doug Hoyes: Yeah and I read that article you wrote and I guess the message there is if you’re buying a vehicle, and you wouldn’t think you need to do this when you’re buying a brand new vehicle, but you can go to Service Ontario. I think you mentioned it in your article, you can do a lien search, a PPSA search on the vehicle if you have the VIN number and you can see if there’s anything registered against it.

There shouldn’t be any need to do that in the case of a new car but here you go, there’s a classic example. So that’s what it comes down to I guess, that’s what it comes down to and I think you’re right, the articles you write in the Toronto Star a lot of them are, “well here’s what happened to this person”, this is a real story, it’s a warning flag for everyone else to not fall into that trap.

Well I think there you go, we’ve invented a new theory of financial literacy education here today and that is explain the downside, explain the risks in the form of a story, that’s what we’re going to remember a lot more than me giving a lecture on proper budgeting techniques. That’s what people are going to remember.

Ellen Roseman: Yes that’s right and you can budget all you like but if you’re wasting money through not paying attention to your consumer purchases you’ll have much less money to save in the future. And so yeah you have to look at the future, but you also have to look at what you’re doing with your money on a day to day basis and are you paying too much, are you not doing your research, are you falling for tricks.

And it’s probably helpful for people to spend an hour a week maybe calling some of their suppliers and asking them “do I have the best deal, do you have a better deal for me, what am I paying for, do you have new plan that’s come out since I got my current plan?” and often that can save you some money that you can then put into RRSP.

Doug Hoyes: I think those are fantastic, practical pieces of advice. I really appreciate you being here, thanks very much Ellen.

Ellen Roseman: Okay, thanks Doug. Bye.

Doug Hoyes: Great, thank you.

Third Segment

Doug Hoyes: Welcome back. It’s time for the 30 second recap of what we discussed today. My guest today was Ellen Roseman who believes that financial literacy is important but also believes that we often go to biased sources for financial advice, like the banks, and that can lead us to buy products we don’t need. A better source of advice is independent journalists and personal finance bloggers who share advice from their own personal experience.

That’s the 30 second recap of what we discussed today. So what’s my take on this? I fully agree that financial literacy education must be more than just discussing budgeting techniques. Ellen’s column does a great job of sharing stories so that we can learn from the mistakes of others and ultimately I believe that’s the best way to promote financial literacy.

For every financial decision you make, ask yourself “what’s the downside?”, “what are the risks?”, then do your own research from independent sources and make an informed decision. That’s our show for today. You can find full show notes with links to everything we discussed today at hoyes.com. You can also subscribe to the show on iTunes or any other podcasting service. Thanks for listening. Until next week, I’m Doug Hoyes, that was Debt Free in 30.

Bonus Segment

Welcome back. My guest today is Ellen Roseman, a columnist with the Toronto Star and she’s already given us some great practical advice and some thoughts on how to improve financial literacy in Canada. I don’t think it’s an exaggeration to say that she wrote the book on financial literacy in Canada. In fact she wrote two books specifically on that topic, Money 101: Every Canadian’s Guide to Personal Finance; and Money 201: More Personal Finance Advice for Every Canadian.

Her most recent book is Fight Back: 81 Ways to Help You Save Money and Protect Yourself from Corporate Trickery. I’ll put links to all those books in the show notes. The radio show portion of Debt Free in 30 is only 22 minutes long so I had to edit out some great practical advice that Ellen gave. It’s great advice, easy to do with virtually no cost and it could save you a lot of money. So here’s more practical advice from Ellen Roseman.

Before the break we were talking about some practical things you can do and Ellen your comment was, hey if I’m hiring a mover to move all my stuff, and this applies in every facet of your financial life, think about what the worst case scenario is and protect yourself for it, one thing you can do then is take a photograph of all the stuff that’s being moved so you know that it ends up where it’s supposed to be. Where else does taking picture make sense you know in the financial world?

Ellen Roseman: It makes a lot of sense with your home insurance policy where they advise you to do an inventory every year. Now I know all of us have a lot of stuff in our house and if you’re going to write it all down it could take you weeks and weeks. So do a photograph of all the major rooms, you know taking pictures of the things in the room that tend to be more valuable. Some people now use the video feature and they just do the video and maybe talk a little bit about here’s this and here’s this and here’s this because if there’s a fire in your house, all of a sudden you have no memory anymore of what it was in every room, so it’s good to have.

Doug Hoyes: That’s great additional advice from Ellen Roseman, and that wraps up the bonus segment here on Debt Free in 30.

The message today is that financial literacy is a lot more than just learning how to balance a chequebook or make a budget. That’s obviously important, but even more important is to develop the mindset that you are in charge of your financial life.

Be suspicious. Be skeptical. Think. And do simple things like take pictures of your stuff on a regular basis, for insurance purposes, or before you move. It’s easy to do, and it make save you a lot of time and trouble in the future.

Thanks for listening. I’ll be back next week with a new edition of Debt Free in 30.

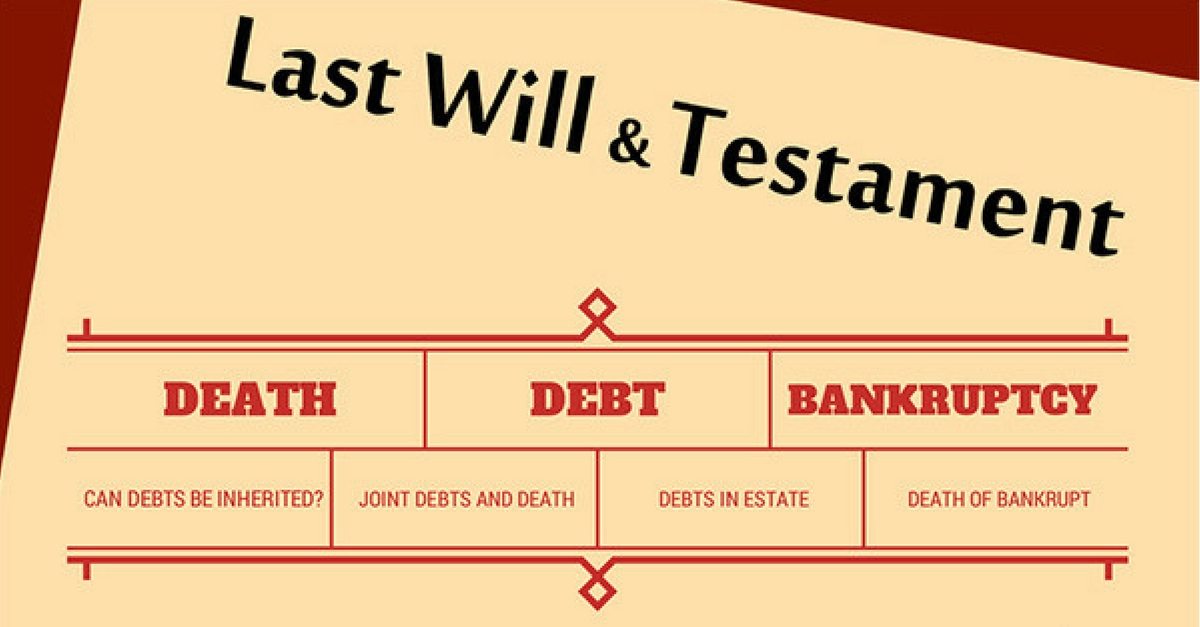

If someone dies, does responsibility for payment of their debts survive their death? Could you be held responsible for the debts of your spouse or parents after they die?

To answer this question we need to address three specific issues:

Can debts be inherited?

Is there money in the estate?

What happens to joint debts?

We will also talk about what happens when a bankrupt person dies and whether or not a deceased individual (that is their estate) can declare bankruptcy.

Inherited Debts

It is important to know that debts cannot be inherited nor can they be transferred upon death without your agreement. In Canada, you cannot become liable for anyone else’s debt by virtue of marriage or death.

The only exception to this rule is if you signed for the debt yourself, either as a joint debtor or as a guarantor.

In fact, the only way anyone becomes liable for a debt is by “signing on the dotted line”. If you didn’t sign for it or agree to pay it, it’s not your debt.

Upon the death of an individual, the lender will still expect to receive payment. Each lender will follow different procedures. It is not unusual for the lender to request payment from the surviving spouse or relative, even though it is not legal to attempt to collect from someone who is not the debtor.

The proper procedure is for the creditors to look to the estate of the deceased individual for payment. If the person who died had assets, such as investments or a house, the executor or trustee of the estate is responsible for ensuring that all legitimate outstanding bills and debts are paid out of the proceeds of the estate. They should notify all creditors of the death by providing a copy of the death certificate and request that accounts, including credit cards, be closed.

While a will cannot pass responsibility for debts on to any surviving person, it does provide for the distribution of assets. These assets however cannot be distributed to any heirs until all valid debts have been paid. This may require the sale of assets in order to generate cash to pay off debts.

If there is insufficient funds in the estate to cover of the debts of a deceased individual, the remaining unpaid balance should be written off as noncollectable unless they are considered joint debts or are guaranteed by a survivor.

Joint Debts After Death

Collections for joint debts may vary by lender and by type of debt. Lenders may first look to the estate for payment or, perhaps in the case of a mortgage, allow the joint debtor to continue with the existing payment terms.

In the event there are insufficient funds in the estate to pay joint debts in full, creditors will look to the joint debtor, or co-signor to make up the balance of the loan. This unfortunately is one of the leading causes of insolvency among seniors in the event that debts are more than can now be paid on one reduced income.

You should be careful to understand what debts you are legally responsible for in the event of the death of a spouse or relative. You are only liable to pay debts you have contractually agreed to pay and have signed for. Debts cannot be inherited or left to anyone in a will.

Unfortunately after a traumatic event such as the death of a spouse the surviving spouse is often vulnerable to collection tactics, so we strongly recommend that you consult a lawyer or trustee to fully understand the rights of creditors in the event of the death of a debtor.

What Happens If A Bankrupt Dies?

If a bankrupt dies before they are discharged, the trustee will obtain a copy of the death certificate and contact the executor to determine what further actions are required. If the deceased had life insurance, and if the beneficiary was the estate, the life insurance proceeds will be forwarded to the trustee for distribution to the creditors. (In most cases a spouse or child is the beneficiary, in which case the life insurance proceeds are not paid to the trustee).

If the bankrupt is eligible to receive a CPP death benefit the benefit is paid to the trustee, for distribution to the creditors. However, pursuant to section 136 (1)(a) of the Bankruptcy & Insolvency Act the trustee is required to pay reasonable funeral expenses of the bankrupt, so in many cases the death benefit is used to pay funeral expenses, and is not distributed to the creditors.

Can A Deceased Person Declare Bankruptcy?

It is very unusual, but it is actually possible for a dead person (or more accurately the estate of a dead person) to declare bankruptcy. For example, if the deceased has assets worth $100,000 and debts of $200,000, a bankruptcy or more likely a consumer proposal could be used to divide up the $100,000 in assets among the estate’s creditors. In this example each creditor would get approximately half of their money, and the executor of the estate would know that all funds were distributed fairly to all creditors.

Occasionally when I meet with someone considering bankruptcy, after reviewing their situation, I tell them they are “creditor proof” and so many not need to file bankruptcy right now. What does being creditor proof mean? Does it really mean they are protected from creditors? Well, yes and no. More importantly, how does that affect whether or when they might need to file for bankruptcy?

Purpose of bankruptcy is creditor protection

The reason someone files for bankruptcy in Canada is to protect their wages or assets from collection actions from their creditors while they eliminate their debt. Debt collectors and creditors can take you to court and eventually apply to garnish your wages. However not all income can be garnished, like pension income, or you may not be working. And you may not own anything. In this case, your creditors don’t have anything to collect from.

To be creditor proof or collection proof, means you have no income or assets that can be seized for debt repayment. If you don’t have any wages or assets for creditors to seize, you have nothing to protect and so bankruptcy may not be necessary.

Does that mean I can’t be sued? No, you can still be sued. The difference is that even if you are sued there is little that can be done, you are in effect judgment proof in terms of the actions creditors can take. You don’t have any wages that can be garnisheed and you don’t have any assets that can be seized.

Collection of government debts is different. Certain rules don’t apply to the Canada Revenue Agency (formerly known as Revenue Canada). The CRA does not need to go to court to take action to collect from monies they might owe you. If you owe money to the government for tax debts, student loans or liability to CMHC, the government has the right to take your tax refunds and HST cheques until that debt is paid in full.

Can creditors take money from my bank account? If you owe money, say a credit card debt, at the same bank you deposit money, your bank can certainly take money out of your account to repay your credit card debt. This is call the right of offset. Other creditors can get a Court order and take money out of your bank account. And the CRA doesn’t even need a court order to do so.

Will the collection calls stop? No. Your creditors will continue to call however you can simply say you are not working and have no money to pay them.

Can I be forced into filing bankruptcy? Not really. The threat to petition someone into involuntary bankruptcy is a collection tactic, nothing more.

What are your debt options if you are creditor proof?

If you are in this situation, it is important to review the cost of filing for bankruptcy versus the benefits of bankruptcy. If you file bankruptcy there is a minimum monthly payment to cover the costs of administration of your bankruptcy.

For some the correct answer is to do nothing until you are back to work because then you will be at risk of your creditors garnishing your wages. Once you know you will return to work, you should talk to your trustee so decisions can be made about the best time to file bankruptcy to keep your costs as low as possible.

If you do owe money at the bank where you have an account where any monies you receive are deposited, say your unemployment insurance or pension, we recommend that you open an account at a new bank and have your deposits (and any automatic payments) transferred there to avoid any chance your bank will seize future deposits.

If you have a large tax refund that can be seized, it may be more beneficial to save enough, or borrow from family, to cover the cost of filing bankruptcy so you don’t lose any tax refunds.

For others, the stress of dealing with the collection calls is too much to handle in addition to being off work. Some want to know that they can have their debt problems solved sooner rather than later. Again, if you can afford the minimum payments, and expect to return to work soon, you can choose to file early if you wish.

If you have debts and are not sure if you have income or assets that can be affected, contact us today to book a free, no-obligation consultation. We’ll tell you honestly if we think it would be better for you to wait to file bankruptcy because you are creditor proof.

What is financial literacy and it is something the government can teach or promote? November is financial literacy month in Canada. Our guest, Jane Rooney is Canada’s Financial Literacy Leader. We ask her those tough questions.

What is Financial Literacy?

Back on show #3 Gail Vaz-Oxlade said:

Financial Literacy is knowing what you need to know in order to build a rock solid financial foundation. But it’s not just about the knowing. It’s also about the doing.

Jane Rooney’s definition of financial literacy is:

Having the knowledge, the skills and the confidence to make responsible financial decisions.

Combing those defiinitions, financial literacy is:

Knowing what you need to know

When you need to know it, and

Having the confidence to

Do what you need to do.

What Role Should the Federal Government Play in Promoting Financial Literacy?

Which brings us to the central question: should the federal government promote financial literacy, or should the private sector or charitable organizations lead the charge?

There are numerous resources already available if you want to learn about money. Every bank, financial planner, credit counsellor, mortgage broker and bankruptcy trustee wants to help you improve your financial literacy skills, and they want to make a buck doing it. And that’s where it gets difficult. How do you know if you are getting good advice, or just a sales pitch?

Jane Rooney was appointed by the federal government to be Canada’s Financial Literacy Leader, and as she explained on today’s show her role is to take all of the resources that already exist, and bring them together. She is working with all stakeholders, to ensure that all Canadians know where to find the resources they require. She is also looking for gaps in the resources that exist. She hopes to encourage others to create them, or the government may take a more active role in creating the necessary resources directly.

Ultimately no-one is unbiased, so we conclude that it’s up to each individual to do their own research and decide for themselves what resources they require to be fully informed and protected consumers.

Doug Hoyes: Welcome to our special Financial Literacy broadcast here on Debt Free in 30. I’m Doug Hoyes.

It’s the month of November, and if you are in the money business you know that in Canada November is Financial Literacy Month.

So why should you care?

Many reasons. One reason is that Financial Literacy Month is a creation of the federal government, so it can be argued that your tax dollars go towards promoting financial literacy in Canada. You want to know if your tax dollars are being wisely spent.

Why is the federal government spending your tax dollars on financial literacy?

Good question, so to find out I’ve invited Canada’s Financial Literacy Leader to be on the show to answer that question, and many others.

Gail Vaz-Oxlade: Financial literacy is knowing what you need to know in order to build a rock-solid financial foundation. But it’s not just about the knowing, it’s also about the doing. And the big gap we have had so far is that it’s fine to say, yes, I know I should contribute to my RSP but if I’m not actually contributing to my RSP then I’m not getting any further ahead. Yes, I know I shouldn’t be carrying a balance on my credit card but if I’m actually carrying a balance on my credit card then that knowledge component is in direct conflict with the behaviour.

Doug Hoyes: I like Gail’s definition of financial literacy. It’s knowing what you need to know, when you need to know it, and doing it. But how do you learn what you need to know? The problem, as I see it, is that you want unbiased advice and most people are trying to sell you something, so their advice is biased.

If I go to the bank to get advice on an RRSP the bank may recommend that I get an RSP loan to top up my RRSP. That may be very good advice, or not. Is the bank telling me to get an RRSP loan because that’s what I should do, or is it because they’re trying to sell me both a loan and an RRSP? I don’t know.

Who can teach financial literacy in an unbiased manner?

Obviously, Gail is doing her best, but she doesn’t have unlimited resources to maintain a training program for the entire country. It costs money.

So if a single person can’t afford to help the entire country, and if the banks and other big organizations are biased because they’re trying to sell us something, who else can we turn to for help?

Perhaps the answer is the federal government. On the surface, it doesn’t appear that they are biased. They don’t appear to sell loans, or credit cards or any other financial product. Perhaps they should be leading the charge for financial literacy.

As it turns out, they are.

On April 10th, 2014 the Financial Consumer Agency of Canada, an agency of the federal government, appointed a Financial Literacy Leader. Her name is Jane Rooney. So I phoned her up to see what she’s doing.

Jane Rooney: Jane Rooney speaking. May I help you?

Doug Hoyes: Hi. It’s Doug Hoyes calling. How are you doing today?

Jane Rooney: Hi there. I’m great. How are you?

Doug Hoyes: I am good. Thank you very much.

Of course, I didn’t just phone her out of the blue. I e-mailed her first and she agreed to talk to me. So I thanked her for taking the time to talk to me and then we started with the basics. My first question to her was “what is her definition of financial literacy?”

Jane Rooney: The definition of financial literacy that we have adopted was coined by the Task Force on Financial Literacy. And it’s having the knowledge, the skills and the confidence to make responsible financial decisions.

Doug Hoyes: Okay. So that’s pretty straightforward. So your mandate then as the Financial Literacy Leader, so what specifically are you trying to accomplish?

Jane Rooney: The mandate at my office is to develop a national strategy for strengthening financial literacy of Canadians. And to do that I have a mandate to collaborate and coordinate financial literacy initiatives among all stakeholder groups. So private sector, public sector and the non-profit sector. And, ultimately, what we’re trying to accomplish is helping Canadians better manage their money.

Doug Hoyes: So your job is to bring everyone together. So you —

Jane Rooney: Exactly.

Doug Hoyes: So you listed off a number of different groups there. And I guess my question is there’s all these different groups who are already doing things, you’re going to be kind of the coordinator, you’ve got the big banks, you’ve got financial planners, credit counsellors, obviously, they’re very active, there’s lots of resources available on the internet. So, with all of that activity, why is it necessary for there to be a coordinator like you with the federal government to get involved in promoting financial literacy?

Jane Rooney: So important to have a focal point for financial literacy so that Canadians can understand where to go to to get information. And it’s an opportunity to coordinate efforts that are already underway because, you’re right, there are lots of great activities that are already underway. But with a coordinated approach, common goals that we’re all trying to improve financial literacy for Canadians, a coordinated effort will improve, we hope, the results of our financial literacy efforts.

So it’s bridging the different groups. So bridging the opportunity is to bring together non-profits with, say, public sector entities, like the federal government, or provincial entities or even private sector. So it’s an opportunity to coordinate efforts, to bring people together to one area to understand what’s available for people to help improve their financial literacy.

Doug Hoyes: So you were appointed … I think it was April of 2014. So we’re about, let’s say, half a year into your appointment. So what bridging, what accomplishments have you had so far, how have you made progress so far in improving the financial literacy for Canadians?

Jane Rooney: To date, I have appointed fifteen members to a national steering committee. And those are champions from different sectors. So I have fifteen members of non-profit organizations, public sector organizations and private sector entities to help me develop the national strategy. They are to help me champion and undertake activities within their own sectors.

I’ve gone through a fulsome consultation process on helping improve the financial literacy for seniors. So I’ve met with … along with Minister Sorenson, the Minister of State for Finance, and Minister of State Wong for Seniors. We’ve worked through a five-city consultation process and an online consultation. And we will be launching a senior’s strategy to improve financial literacy for seniors in the very near future.

We have re-fielded the Canadian Financial Capability Survey. So in 2009 the largest Financial Capability Survey was first fielded. We have re-fielded it and the results will be available during Financial Literacy Month. I will be releasing them early November. And so we’ll have a very good sense of where Canadians are at in terms of their knowledge and their skills around money matters.

And we’ve also developed a resource database. So, again, it’s to bring Canadians to the resources that are available to help them strengthen their financial literacy. And that database will be fully launched in the month of November, during Financial Literacy Month. So there’s material, there’s tools, information about workshops, from all walks of life. So across provinces, nationally available, workshops that are available in person. So it’s an opportunity for Canadians to learn who’s out there to help them, what information’s available to help them in a one-stop shop resource database.

Doug Hoyes: And that’s really the main thrust of it then is to make sure people know where to go to find those resources. So it’s not necessarily that you are creating the resources. It’s there are resources out there, let’s make sure people can find them. Is that one of the main things?

Jane Rooney: Exactly. We want to reduce duplication of effort and bring people to what already exists. So it’s not reinventing the wheel, it’s actually pointing people to the resources that already exist.

It’s also an opportunity to identify are there gaps, is there anything that’s missing out there? And then we at the FCAC could identify whether or not we’re the best place to fill the gap with a new product or whether there are others out there that are best placed to fill that gap.

Doug Hoyes: That’s the first part of my conversation with Jane Rooney, Canada’s Financial Literacy Leader. After the break, you’ll hear her answers to more questions, including her view on the main financial literacy issues we face. And I also ask her to summarize her accomplishments since being appointed Financial Literacy Leader about six months ago. Those questions and more after the break. You’re listening to Debt Free in 30.

Announcer: You’re listening to Debt Free in 30. Here’s your host, Doug Hoyes.

Doug Hoyes: Before the break I asked Jane Rooney, Canada’s Financial Literacy Leader, to explain why, with all of the resources out there, she thought it was necessary for the federal government to get involved in financial literacy. She explained that there are lots of resources but there is no focal point to bring all of those resources together, and one of her jobs is to determine if there are any gaps in the financial literacy resources available to Canadians. So I asked her to tell me what gaps she sees and to give her view on what she sees as the main financial literacy issues in Canada. Here’s her answer.

Jane Rooney: So I mentioned a survey that was conducted. And the results were described in five different areas. So people are having trouble planning ahead. That means planning ahead for short-term goals, savings goals and long-term goals like planning for retirement.

People are having trouble keeping track of their money, so that means basic budgeting skills, knowing what their income is, knowing what their expenses is and how much is left over.

We know that people are having trouble staying informed about financial products and services. As you know, it’s a very complex financial marketplace, and more and more new products and new ways of accessing products is coming out, like mobile. So it’s important for us to know and that things are being done to help improve people staying informed.

The other two areas that were evaluated were choosing products. And the choosing products … people, once they know what’s available, are finding products that suit their needs. But, again, the definition of financial literacy, it’s so important for people to know what are the products and services, what are their rights and responsibilities, what questions should they ask so that they are choosing a product that best suits their needs.

And then, as a final area that they’re looking at in terms of improvement, is around … sorry, I’m forgetting the last one. But all that to say is this first three, planning ahead, staying informed and keeping track of money are the key areas that we know people need help with. And so my focus is what products are already out there and connecting Canadians with those products so that they can improve those skills.

Doug Hoyes: Gotcha. And I think getting people to ask questions is probably the most important of all those things you listed off. If we would all take a step back and ask questions before we signed on the dotted line, we would probably be in a lot better shape.

So your group is in the process, you said, of drafting a national strategy for financial literacy. And I’ll put a link in the show notes to the material on your website that talks about what you’ve addressed.

So the first phase you mentioned is with respect to seniors, strengthening financial literacy for seniors. And I’m curious, so why did you start with seniors? I’m sitting here thinking, well, I guess the people we need to talk to are the young people because they’ve got their whole lives ahead of them. Why did you start with the focus on seniors? Are there some issues that are unique to them? Why seniors?

Jane Rooney: Yes. So the first phase of the consultation was around seniors. And there are two other phases. One is around priority groups, so helping low income, Aboriginal, newcomers to Canada, people with disabilities, help strengthen their financial literacy. Phase three is about youth and adults.

And all those phases of consultations will be done this year. And all of that information will be fed into a national strategy on financial literacy. So it’ll be a national strategy for all Canadians that’s inclusive, it’s relevant and it’s accessible to Canadians. So it’ll be across the lifespan, how can we help people.

Now, why did we start with seniors, key information … seniors were found in the Financial Capability Survey as having a higher need. They answered the questions with less confidence than other segments of the population.

There’s also recent statistics that show seniors and near seniors are higher levels of debt as they enter their senior years. But also higher levels of bankruptcy rate. So there’s a key concern there. And with a growing population in near seniors and current seniors, really important to tackle that audience.

It’s also important to note that the Financial Consumer Agency of Canada was actually given funding for youth, developed a financial literacy program for youth back in 2007. So we actually tackled, at the agency, information for youth and developed a program called The City: A Financial Life Skills Resource. And we worked very closely with provinces and territories across Canada to integrate financial education into the school curriculum.

So youth continues to be a key focus and you will see youth reflected in the national strategy. It’s important to start young and it’s important to repeat that information all throughout one’s life course.

Doug Hoyes: Yeah, and you’re absolutely right with the seniors, they do have the highest level of debt because they’ve been around long enough to accumulate it. It’s, kind of hard for an eighteen-year-old to have mortgages, and car loans and lots of credit cards and everything. And I think you’re right, they as a result become more susceptible to bankruptcy and other factors when they get downsized or have other issues.

So what’s next then? You talked about drafting the national strategy. So what’s the timeline on having that completed and what do you see as the next steps?

Jane Rooney: Well, very exciting times. We’re actually going to be launching our phase two consultations. So that’s consultations around the priority groups, low-income Canadians, Aboriginal Canadians, newcomers to Canada, people with disabilities. So what are the unique challenges that those people face that we can address in the national strategy. Those consultations will be launched shortly. And the online consultation paper is open until December 10th for comment.

We’re also going to be launching consultations during the month of November, Financial Literacy Month, around children, youth and adults. So, again, it’s an opportunity for all Canadians and stakeholder groups, people who work with Canadians, to have their say about what are the unique challenges that these groups face and how best can we reach those groups with key information, at teachable moments, through what types of activities.

The phase three consultation paper will be available until December 31st for comment. Once we’ve analyzed all the input that we’ve received, the final version, a national strategy for all Canadians will be launched in 2015.

Doug Hoyes: Gotcha. So the seniors was the first consultation and the consultation phase is closed. And the results of that phase are going to be released in November; is that what you said?

Jane Rooney: We’re going to be releasing the national … sorry, seniors strategy, very shortly, actually.

Doug Hoyes: Very shortly, okay.

Jane Rooney: That was as a result of Economic Action Plan 2013 where the government put a priority on developing a strategy for seniors, improving their financial literacy. And we will deliver on that very shortly. And it’ll be publicly available, the seniors strategy, on FCAC’s website.

Doug Hoyes: Okay, good. And what I’ll do in the show notes is I’ll put all the links to the website. And it’s very well laid out. You’ve got all the different segments there. So that should make it easier for people to follow along. So I appreciate you joining me. Is there anything else you would like to add that we haven’t covered, anything else in conclusion?

Jane Rooney: Sure. I’d like to say I’m honoured to have been named Canada’s first Financial Literacy Leader. And I’m really pleased and proud that the Government of Canada has made such a commitment to financial literacy. And by having a focused office for financial literacy, I hope Canadians will be able to find the resources to help them improve their skills.

And, finally, Financial Literacy Month is the month of November. There are lots of activities that are happening. So I would invite people to come to FCAC’s website, look at the calendar of events, find out if there’s an activity or an event happening in a community near you that you might want to be involved in.

Doug Hoyes: That’s my conversation with Jane Rooney, Canada’s Financial Literacy Leader. I’ll be back after the break to wrap up the show. You’re listening to Debt Free in 30.

Segment 3

You’re listening to Debt Free in 30. Here’s your host, Doug Hoyes

30 Second Recap

Welcome back. It’s time for the 30 second recap of what we discussed today.

My guest today was Jane Rooney, Canada’s Financial Literacy Leader. Ms. Rooney gave her definition of financial literacy, discussed her mandate, and described her accomplishments during the first six months of her tenure, and laid out the plan for drafting a National Strategy for Financial Literacy for Canada.

She agreed that there are lots of groups involved in financial literacy, and lots of resources available. She sees her job as a facilitator, bringing together the different groups, and identifying gaps in the resources available and working to fill those gaps. She is working towards a National Strategy on Financial Literacy, and is consulting with Canadians with a goal to have the strategy ready to go in 2015.

That’s the 30 second recap of what we discussed today.

Should The Federal Government Promote Financial Literacy?

So what’s my take on this? We covered a lot of topics today, and I don’t have time to comment on every topic, so I’ll pick the most controversial area, and that is “should the federal government be involved in promoting financial literacy?”

That’s a difficult question.

As I said during the show, there are lots of resources out there. Every bank, financial planner, credit counsellor, mortgage broker and bankruptcy trustee wants to help you improve your financial literacy, and they want to make a buck doing it. And that’s the difficult issue. How do you know if you are getting good advice, or just a sales pitch?

That’s why there may be a role for the federal government.

I’m a taxpayer, so I don’t want my tax dollars spent on anything unnecessary, but since the government has many partners in this endeavour, and those partners are helping with the funding, it may be a positive step to have the government co-ordinating the efforts of the private and not for profit sector.

Or not. It’s too early to tell.

Perhaps the government is also biased. The National Conference on Financial Literacy, to be held on November 6 and 7 in Vancouver, is sponsored by Visa and all of the big banks. If you are getting funding from the big banks, are you unbiased?

See what I mean about this being a difficult issue? I don’t want the government using my tax dollars, but I also worry about the big banks funding the exercise, so it would appear to be a no win situation. Or not. It may work out great. Jane Rooney is obviously very passionate about this project, and I’m sure she will do everything in her power to advance the cause of financial literacy in Canada, and that’s a very noble objective.

I’ll keep a close eye on this, and if there are any significant developments I’ll report back on future episodes.

I’m interested in your thoughts, so feel free to post your comments on our website at hoyes.com, that’s h-o-y-e-s.com, where you can also find full show notes, transcripts, and links to everything we talked about on the show.

To get this show automatically every Saturday morning, please subscribe on iTunes or any other podcasting service.

Thanks for listening.

Until next week, I’m Doug Hoyes, that was Debt Free in 30.

Bonus Segment

Doug Hoyes: As is often the case on these shows I run out of time on the radio only portion of the show, so for our podcast listeners I’d like to do a more complete wrap up of what we discussed.

First, I think we had two very good definitions of financial literacy today.

I started with Gail Vaz-Oxlade’s definition:

Gail Vax-Oxlade: Well, financial literacy is knowing what you need to know in order to build a rock solid financial foundation. But it’s not just about the knowing, it’s also about the doing.

So Gail’s definition is about both know and doing.

Here’s Jane Rooney’s definition:

Jane Rooney: Having the knowledge, the skills and the confidence to make responsible financial decisions.

Jane’s definition includes the word “confidence”, and I like that word. When you are sitting at a car dealership or the bank haggling over the interest rate on your car loan, you need the confidence to be able to stand your ground and walk away if you aren’t getting a good deal.

If I had to make up a definition of financial literacy I’d combine the best of both of those definitions and say financial literacy is

Knowing what you need to know

When you need to know it and

Having the confidence to

Do what you need to do.

It’s a combination of timely skills, confidence, and actually getting it done.

I asked Gail what her solution was, and she said she created a website to help people. Here’s what she said:

Gail Vaz-Oxlade: I created a website called mymoneymychoices.com, because there was nowhere, anywhere [laughs], anywhere on the internet, nowhere in a financial institution, nobody had a plan. Everybody was talking about financial literacy and there was a huge debate about what should be included in financial literacy, but nobody was willing to step up and give a plan. And so what I did was I created the roadmap, and the roadmap starts at step one – you can’t get to step two until you do step one. You do step one, then you do step two, and so on, all the way through to the end. The idea being that you actually have to take the steps to make your financial foundation firm if you want to be considered financially literate.

Doug Hoyes: So this is a money making thing for you. What’s the cost of this?

Gail Vax-Oxlade: There is no money to be made off this. There is no cost. I know –

Doug Hoyes: [Laughs]. What, are you nuts there, Gail? I mean come on.

Gail Vax-Oxlade: That’s what everybody says. Everybody says so how are you monetizing this, Gail? And I’m not monetizing it. In fact, this has cost me probably about $20,000 of my own money so far in order to put this program in place in terms of coming up with the structure and paying someone to build the website and purchasing the pictures that go on the website and all that other stuff. I am not interested in monetizing this. What I am trying to do is get Canadians – because I can’t be everywhere, Doug.

Doug Hoyes: [Laughs]

Gail Vax-Oxlade: And this is the thing, is that everybody wants me. And so what this does is this tells you exactly what I would tell you to do if I showed up at your door. If I showed up at your door the first thing I would make you do is do a spending analysis. So the first step in the My Money My Choices Program is to do a spending analysis. I’d make you make a budget, I’d make you make a debt repayment plan.

The nice thing about the programme is it’s structured in such a way that it’s a learn one teach one system. So when I do my spending analysis, not only do I move to the next activity but then it becomes incumbent on me to find somebody to teach to do a spending analysis. And that’s how I hope the program will spread across Canada. I’m just about to implement a fundraising campaign to get some money to do some advertising, because I think that’s an important step. And I have only so many resources to commit to this, so that will be my next step.

Doug Hoyes: And since we recorded that interview Gail has started a fund raising campaign; I’ll put a link in the show notes if you want to contribute.

But again I come back to my earlier point: who can teach financial literacy in an unbiased manner?

Obviously Gail is doing her best, but she doesn’t have unlimited resources to maintain a training program for the entire country. It costs money.

So if a single person can’t help the entire country, and if the banks and other big organizations are biased, because they are trying to sell us something, who else can we turn to for help?

That’s where Jane Rooney and the federal government can play a role, but as I said earlier, even the government receives funding from the big banks, so even they could be subject to some bias.

O what’s my solution?

I think the answer is obvious.

You have to be the boss. You have to take care of yourself.

You should use all of the resources available to learn everything you can about money management.

Join Gail’s my money my choices group.

Go the government’s website and review all of their resources.

Go to my websites and read all of the free material.

Ask questions.

Do more research.

Whenever you are getting advice, ask yourself “what are they trying to sell me?” By asking the tough questions, you can get answers, and you can make an informed decision.

It’s not easy, but that’s my ultimate solution to improving financial literacy in Canada.

We must take responsibility for ourselves. That’s the solution.

That’s our special financial literacy show for today.

Please subscribe on iTunes, and leave a review because that helps the show, and whether you agree or disagree please leave your comments on the show notes on hoyes.com.