Reviewing your credit report at least once a year is part of a healthy financial routine. What you should be on the lookout for is errors or out-of-date information.

Why you should check your credit report annually

This annual routine is important because you don’t want inaccurate information to hold you back from achieving your financial goals. Here are some big reasons to check your credit report:

Before making a major purchase with financing, like a house or car, the prospective lender will want to review your credit file. Inaccurate information may mean that you are declined or offered a higher interest rate.

Identity theft is becoming more prevalent. You may not realize that somebody has obtained a credit card in your name until seeing the details on a credit report.

Many employers require a credit check as part of the hiring process.

Creditors and collection agencies may update one credit report, but not all. It is important to verify that your credit report is correct within each credit bureau, because a lender, employer or potential landlord could check any one report (and odds are they may only check one), impacting whether you will be approved.

Below are links on where to get your free credit report and how you can apply to have errors corrected. We also explain what the typical credit report looks like.

In Lesson 3 I talked about how paying your bills on time and keeping your balances low are the 2 most important things you can do to improve your credit score. However, your credit score is only as good as the information that is on your credit report. Credit bureaus get their information from your creditors and mistakes do happen. In fact, they happen all the time, in my experience it’s very rare to see a credit report where everything is perfect. It’s up to you to make sure that the information reported about you is accurate. The first step in rebuilding credit, is to get a copy of your report, a free version is all you need. Credit bureaus are required by law to provide you with a free copy of your credit report once a year. The best source is directly from TransUnion, Equifax or your bank if they offer you that service for free in their app or online banking platform. Companies like Credit Karma or Borrowell also provide free reports, but in my experience, these reports only present summary information, and their information may be somewhat out of date, so they may not be exactly the same as what’s on your actual credit report. Potential lenders don’t see reports from these FinTech companies, lenders will look at either TransUnion or Equifax, so don’t rely on a middleman, go right to the source to make sure the information on your credit reports is correct. You can request a copy from each credit bureau online, by mail or by phone. I’ll put links to the online application in the description below and on our website Hoyes.com, but you can also go to Equifax.ca or TransUnion.ca and search their websites for free credit report. If you phone or mail in your request it can take 3 weeks to receive your copy in the mail. Both credit bureaus will want to verify that you are who you say you are. If you are applying by mail, they’ll require you to send copies of your ID with your application. If you’ve recently moved, a copy of a phone bill or lease agreement will provide evidence of your correct address. If you’re applying online, they’ll ask you some questions to verify your identity. Your free credit report won’t tell you your credit score, but since what you’re doing at this stage is checking for inaccurate information, you don’t need your credit score. The next question is when should I check my credit report? Well, if you’re rebuilding your credit after filing a bankruptcy or proposal, we recommend waiting at least 2 weeks after your discharge or completion before requesting a copy of your report. You want to wait long enough for the government to report your completion date to the credit bureaus, and this is done weekly. Can you check your report while you’re in your bankruptcy or proposal? Yes, but the credit bureaus may not fix any errors until your filing is complete, so to avoid frustration I generally recommend you wait unless you’re really eager to ask the credit bureaus to correct errors. Eventually you can review your report once a year to check for errors and potential fraud or identity theft. If you want to see your credit report for free more than once a year, you can order a free report from Equifax, than 6 months later order a report from TransUnion and keep alternating every 6 months. And yes, you can pay Equifax and TransUnion directly to get your credit report as often as you want, but to start a free version is all you need. Once you have your report, it’s time to check for errors. I’ll cover what to look for in the next 2 lessons.

We recommend getting a copy of your credit report directly from TransUnion or Equifax, Canada’s two major credit bureaus. As an alternative, you can get a copy through your bank if they offer you that service for free in their app or online banking platform.

Companies like Credit Karma or Borrowell also provide free reports, but our experience is that these reports do not always agree with what the credit bureaus have on file, and their information may be somewhat out of date. Potential lenders don’t see reports from these FinTech companies. Lenders will look at either TransUnion or Equifax, so you want to check that these sources are correct.

Both credit bureaus will want to verify that you are who you say you are. They will require you to send copies of 2 pieces of ID with your application. If you have recently moved, a copy of a phone bill or lease agreement will provide evidence of your correct address.

Here’s how to get your credit report for free:

Online

FREE online credit reports are normally only available from TransUnion. However, due to the coronavirus, Equifax is currently making credit reports available for free.

You just need to answer a few personal questions to confirm your identity as well as provide your address and social insurance number. One your identity is confirmed, you will be able to immediately print your credit report.

Please note the online system does not work perfectly. You may need to request a copy by phone or mail instead.

Telephone

Calling each credit bureau is one way to obtain your credit report free of charge.

Equifax Toll Free 1-800-465-7166

Trans Union Toll Free 1-866-525-0262

Each credit bureau requires similar information: social insurance number, date of birth, address (including postal code), credit card number (even if it is no longer active).

Estimated Waiting Period: You would typically receive your credit report within one to two weeks.

Mail or Fax

This is the other free method. Mail and fax are technologies that may seem old fashioned, but they are still effective. You can complete the credit request forms for Equifax and TransUnion and then submit by mail or fax.

Equifax:

National Consumer Relations

P.O. Box 190, Station Jean-Talon

Montreal, Quebec

Fax: 514-355-8502

TransUnion

Consumer Relations Centre

PO Box 338 LCD1

Hamilton, Ontario L8L 7W2

Turnaround time is typically one to two weeks.

What if I find an error on my credit report?

Credit bureaus get their information from various creditors and sometimes mistakes are made in both reporting and recording. If you do find errors, it is important to get these mistakes corrected as soon as possible. You can follow the links to the dispute resolution procedures for Equifax and TransUnion. You will need to provide proof of the error and will need to be diligent in following up to ensure the issue is corrected.

If you have been bankrupt or filed a consumer proposal, the notice of your filing will be removed from your credit report after a certain period of time. If you believe your notice should be removed, use this dispute resolution process to contact the appropriate agency. Each bureau keeps records for a different length of time but generally the notice of your bankruptcy or proposal should be removed:

A first bankruptcy will be removed after six to seven years following your discharge (depending on the credit bureau). This is extended to 14 years for a second bankruptcy.

A consumer proposal will be removed from your credit report 3 years after all your payments have been completed.

Another common issue we see is that creditors will incorrectly report individual debts as ‘included in a bankruptcy’ when they may have been included in a consumer proposal. The correct legal proceeding is reported to the credit bureau by the Office of the Superintendent of bankruptcy and will appear in the legal section of your credit report. These debts should be purged from your report six years after the last activity. For some creditors this will be the last payment date, for others it may be the date of filing bankruptcy or a consumer proposal.

For more information on how to review your credit report try our Free Online Video Course on Rebuilding Credit. Get a step-by-step plan on how to manage your credit score, how to review your credit report and fix errors and discover what types of credit you need to rebuild credit.

Your free report won’t tell you your credit score. But since what you are doing at this stage is checking for inaccurate information, you don’t need your credit score.

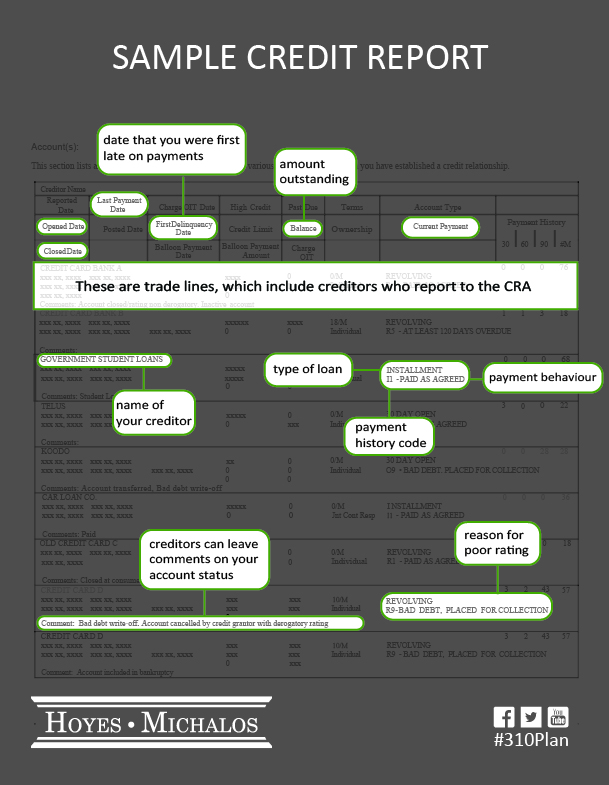

Each creditor that reports to the credit reporting agencies will have their own line where they report on your payment history. These are called trade lines. Creditors will report your history with a letter followed by a number. The letters are loan codes and the numbers are payment history codes. Let’s decode them together:

Loan Codes

I – Installment loan (repaid over time with a set number of scheduled payments e.g. car loan)

O – Open credit (pre-approved loan amount that can be used repeatedly up to a limit, and paid back e.g. line of credit)

R – Revolving credit (automatically renewed after debt is paid off e.g. credit cards)

C – Sometimes used in place of revolving credit

M – Mortgage loan

Payment History Codes

0 – Too new or approved, but not used

1 – Paid within 30 days or as agreed (on time)

2 – Late payment: one month behind

3 – Late payment: two months behind

4 – Late payment: three months behind

5 – Late payment: more than 30 months, but not yet rated “9”

7 – Making payments under a debt plan (could be a consolidation order, orderly payment of debts, consumer proposal or debt management plan)

8 – Repossession

9 – Written off as bad debt, sent to collection or bankruptcy

Your credit report will include your legal name, birth date, and a note about whether or not your social insurance number is on file. It will also include a list of all known addresses, employers, and phone numbers. All of these will be listed starting with your most recent, and ending with the oldest known entry.

Below is a sample of how your credit report from Trans Union will look.

Joint Debts: Did you sign on the dotted line? Today we talk about if and when you might be responsible for your spouse’s debt and how one spouse filing bankruptcy might affect the other. To answer these questions I talk with Hoyes Michalos Licensed Insolvency Trustee Jason Quinney about joint debts and co-signed loans. Jason explains what a joint debt is, what happens to a co-signer if a debt goes unpaid and clears up the misconception that joint debts settled in a bankruptcy or consumer proposal need to be filed individually.

What are joint debts?

Joint debts are debts that you sign documents with legally with another person. Since you co-signed the documents, both you and the co-signer are jointly liable for repayment of the loan. You cannot contract out of a joint debt without the permission of the creditor. This is important since that means you can’t agree to split the debt 50/50 in a separation or divorce. This is one of the risks of considering a joint consolidation loan with your spouse.

Common examples of joint debts include lines of credit, mortgages and credit cards.

Joint credit cards can come in two forms, both a joint card and a supplementary card.

A Joint Credit Card is where individuals have signed for the card and are responsible for the whole amount of the debt (not just half of it). The liability for joint credit cards in a divorce can prove to be a problem if not handled correctly during the separation.

A Supplementary Credit Card is an additional credit card for your spouse, adult child or anyone that you wish to give the card to. Liability for supplementary cards depends on the clauses in the primary credit card contract agreement. In most cases the supplemental card holder has no responsibility for the debt because they did not sign the paperwork. However this is not always the case for all credit cards. They may assume liability for all or part of the debt by using the supplementary card. You should read your specific contract very carefully.

A common misunderstanding is that just because you are married, you are liable for your spouse’s debt. This is not true. Getting married does not make you automatically responsible for your spouse’s debt. If you did not sign for the debt, you are not legally responsible for it. If your spouse files bankruptcy or a consumer proposal, and you are not considered a joint debtor, their bankruptcy or proposal will not affect you.

How will filing bankruptcy or a consumer proposal affect my co-signer?

A co-signer is generally needed because an individual poses a lending risk and the creditor feels that by having a guarantor on the debt, they have ensured that two people are now responsible for repayment of that debt.

If you file bankruptcy, your creditors can, and likely will, pursue your co-signer for collection. Your bankruptcy will not, however, affect your that person’s credit report as long as they continue to make payments on the co-signed debt.

What is a joint consumer proposal or bankruptcy?

If both spouses share substantially the same debts as joint debtors they have two options; they can each file a bankruptcy or proposal or they can file a joint bankruptcy or joint consumer proposal.

Filing jointly is a process that covers both individuals at a lower cost than filing separate insolvencies.

Your trustee would look at each of you individually, your incomes, your debts and your situation to decide if a joint or individual filing is possible and makes most sense.

It is even possible, and not uncommon, for divorced or separated spouses to file jointly to deal with debts from their previous marriage.

If you’re unsure whether your debts are joint or you’re wondering how a joint bankruptcy or consumer proposal process works, contact a Licensed Insolvency to review your situation and discuss all of your options. If in Ontario, contact Hoyes, Michalos for a free no-obligation consultation with one our local licensed bankruptcy trustees.

FULL TRANSCRIPT show #39 with Jason Quinney

For more information about joint debts, co-signers and how to deal with joint debts during a separation or divorce, listen to our podcast or read the full transcript below.

Doug Hoyes: Welcome to Debt Free in 30 where every week we take 30 minutes and talk to industry experts about debt, money and personal finance. I’m Doug Hoyes. It’s the end of the month so that means it’s time for another Frequently Asked Questions show here on Debt Free in 30.

Every day we gets lots of phone calls to our 310PLAN help line and dozens of people every week email the Hoyes Michalos team with questions. I keep track of those questions and we answer the most common questions on our frequently asked questions shows.

We get a lot of questions about what will happen to my spouse if I have debts and what happens to co-signers? So, today we’re going to answer all of your frequently asked questions about spouses, co-signers, supplementary card holders and joint debts. Before we get to those questions let me tell you some facts.

If you’re a regular listener to this show you’ll know that every two years we do a detailed study of everyone who files a bankruptcy or consumer proposal with Hoyes Michalos. We call it our Joe Debtor study and we talked about it back on show #36 which aired on May the 9th. You can go to Joedebtor.ca to read all about it. Here’s some interesting facts from that study. Of all the people who go bankrupt or file a consumer proposal, 40% are married or common law and 28% are separated or divorced. That means that more than two thirds of everyone we help either has a spouse or did have a spouse and it’s very likely that they had debts together. What do I mean by debts together? To answer that question and lots of other questions about whether or not your spouse is responsible for your debts, I’m joined today by Jason Quinney, a trustee who works in the Hoyes Michalos offices in Barrie, Vaughn and our Jane and Finch office in Toronto. Jason, welcome the show, how are you doing today?

Jason Quinney: Good, Doug.

Doug Hoyes: So, let’s start with that question, then. What does it mean to have debts together? So, explain that to me.

Jason Quinney: Well, having debts together, I mean a lot of couples when they go get loans they have to get a co-signer, so they co-sign debts together.

Doug Hoyes: So, the key point there is, we have both signed for the debt.

Jason Quinney: Yes.

Doug Hoyes: So give me some examples of where people would both be signing for the same debt.

Jason Quinney: Well, they could go into the bank for a line of credit. Sometimes you need a co-signer so they would both sign together for that line of credit.

Doug Hoyes: Why is the bank asking for a co-signer? What’s the typical reason that two people would be signing?

Jason Quinney: Usually it’s so they could have two people to collect from.

Doug Hoyes: Okay, so the bank wants their butt covered. It’s a lot easier to get money from one person then, or from two people as opposed to one.

Jason Quinney: Yep.

Doug Hoyes: So, a line of credit would be an obvious one. What types of debts are often joint where two people are signing for them?

Jason Quinney: Mortgages.

Doug Hoyes: That would be anther common one.

Jason Quinney: Yeah.

Doug Hoyes: So, what about credit cards. So, there are two different ways a credit card can have two people associated with it. You can have a joint credit card or you can have a supplementary credit card. So, let’s start with the legal concept, what’s the difference between, you know, legally, between a joint credit card and a supplementary credit card?

Jason Quinney: Well, a joint credit card would be a co-signed. So, both of you signed for it, where a supplementary credit card is when you get a credit card and then they ask you if you want another credit card for your spouse.

Doug Hoyes: And that’s a pretty common thing, you fill out the form and you’ve already qualified so-

Jason Quinney: And they always ask you if you want a supplementary one.

Doug Hoyes: You tick the box, boom there it is. So, your spouse, if we want to use that example, and the supplementary card could be for anyone, it could be for your adult child, it could be for your mother I guess. But let’s take the simple scenario of two spouses. So, I tick the box and say yep I’d like a supplementary card for my wife. Now, she hasn’t signed for it, so is she legally responsible if that card doesn’t get paid?

Jason Quinney: Legally, no.

Doug Hoyes: Because she didn’t sign for it.

Jason Quinney: Because she didn’t sign for it.

Doug Hoyes: Okay. So, let’s talk about real life then, tell me some stories about what happens in real life with supplementary card holders.

Jason Quinney: Well, in real life they will go after the second person.

Doug Hoyes: They will go after them. And so what happens? The first person has to go bankrupt, can’t pay, then they start getting the phone calls, the letters whatever.

Jason Quinney: To go after the second person.

Doug Hoyes: So, how do I know, if I’m listening to this today and I’m going gee, oh yeah we’re behind on the credit card bill, I wonder if I’m a joint card holder or a supplementary card holder. How can I figure that out?

Jason Quinney: Well, the easiest way to figure that out would be to look at your credit card statement.

Doug Hoyes: So, if both names are on the credit card statement.

Jason Quinney: Then likely –

Doug Hoyes: Likely we’re both liable for it.

Jason Quinney: Exactly.

Doug Hoyes: So, okay if we both signed for the debt, we’re both liable, and so does that mean I’m 50% liable, my co-signer is 50% liable?

Jason Quinney: No, a lot of people think that though. A lot of people think that they would be just responsible for half of the debt. But no, they would actually be responsible for the whole amount.

Doug Hoyes: So, it’s not 50/50, it’s 100%/100%.

Jason Quinney: Yep.

Doug Hoyes: So, if my co-signer, my joint card holder doesn’t pay, the bank is coming after me for the whole shot.

Jason Quinney: Correct.

Doug Hoyes: Okay, so that’s a pretty important distinction, then. So, just to review then, a joint debt is signed by both people.

Jason Quinney: Yes.

Doug Hoyes: So, if you remember signing the loan application form or the credit card application form, you’re joint.

Jason Quinney: Yes.

Doug Hoyes: It’s pretty much that simple. If you don’t remember signing for it, legally, well, maybe you forgot, but legally if you didn’t sign for it you may not legally be responsible but practically speaking okay, well, you’ve used the card it’s not uncommon that they’re coming after you for it.

Jason Quinney: Yep.

Doug Hoyes: Okay. So, in general, is my spouse – somebody I’m married to – automatically responsible for my debts because we’re married?

Jason Quinney: No.

Doug Hoyes: Now I get people coming into my office all the time saying well, the credit card company phoned me and my spouse isn’t paying, so they said I’m married I’ve got to pay, you’re saying that’s not the case.

Jason Quinney: Correct

Doug Hoyes: Why not?

Jason Quinney: Well, because you haven’t co-signed for it, you’re not joint on the debt; they can only go after the one person.

Doug Hoyes: So, it all comes down to who signed for it.

Jason Quinney: Exactly.

Doug Hoyes: It’s as simple as that. So, if my spouse didn’t sign for it, they’re not liable.

Jason Quinney: Yes.

Doug Hoyes: Simple as that, okay. So, let’s take this a step further then, let’s say that I’m in deep financial trouble, I decide to go bankrupt, my spouse does not decide to go bankrupt.

Jason Quinney: Okay.

Doug Hoyes: How does my bankruptcy legally affect my spouse?

Jason Quinney: Legally it’s not going to affect her at all, as long as the debts not joint.

Doug Hoyes: If the debts were joint, then –

Jason Quinney: Then the creditors will go after her, will go after the spouse.

Doug Hoyes: For the full amount.

Jason Quinney: For the full amount.

Doug Hoyes: So, if my spouse, if I’m considering bankruptcy or I guess a consumer proposal would be exactly the same and I’m trying to figure out the impact on my spouse, did they co-sign? We keep coming back to that same point. Because it’s like you said earlier, it’s a very common misconception oh well, we’re married I guess I’m on the hook for it. You know all the money goes into the same bank account, we pay all the debts together, legally that’s not the case. So, okay, legally if I go bankrupt it doesn’t impact my spouse. What about in real life?

Jason Quinney: In real life it’s going to affect. I mean the bankrupt isn’t going to be a very good co-signer. And so if you go and apply for a loan or a line of credit or a mortgage, it may be difficult.

Doug Hoyes: So, my bankruptcy finishes, we go off to the bank to buy a house, the bank’s going to say, oh you were bankrupt last year, much more difficult to get a mortgage, obviously.

Jason Quinney: Exactly, generally they’re going to want you to wait two years after your bankruptcy’s finished.

Doug Hoyes: In order to be able to get a decent rate.

Jason Quinney: Yes.

Doug Hoyes: So, my spouse is disadvantaged in a bankruptcy because I’m a lousy co-signer in the future.

Jason Quinney: Yes.

Doug Hoyes: I guess the flip side of that though is, I got rid of my debt.

Jason Quinney: Yep.

Doug Hoyes: So, there’s pluses and minuses, I guess you got to look at the big picture. Explain to me in a bankruptcy, and again we’re trying to figure out how a bankruptcy impacts on a spouse, how does surplus income factor into this?

Jason Quinney: Well, surplus income in a bankruptcy situation you have to look at both of the spouse’s income. Okay, so in a bankruptcy situation the spouse could be affected.

Doug Hoyes: Okay, so when you go bankrupt, so again let’s take the case of just the husband is going bankrupt, the wife isn’t.

Jason Quinney: Correct.

Doug Hoyes: Every month you have to prove what your family income is.

Jason Quinney: Yes.

Doug Hoyes: How does that work in practice, how do you do that?

Jason Quinney: Well, we would get the bankrupt to fill out a form, an income and expense statement and they would send that in with proof of their income.

Doug Hoyes: So, their pay stubs.

Jason Quinney: Pay stubs or a bank statement.

Doug Hoyes: And so it would be the pay stubs for both the husband and the wife, even though the wife isn’t bankrupt.

Jason Quinney: Yes.

Doug Hoyes: And the more your family makes, the more you have to pay in a bankruptcy.

Jason Quinney: Exactly.

Doug Hoyes: And we won’t go through all the real specific numbers now but in real general terms a family of two, so let’s say it’s just a husband and a wife, they’re allowed to make around –

Jason Quinney: $2,562 I think it is now.

Doug Hoyes: So, and that’s the number for 2015. So, if you’re listening to this in the future, the number might be slightly higher. But they’re allowed to make let’s say around $2,500, if their income is a lot higher than that because the non-bankrupt spouse has income, that potentially means the bankrupt spouse has to pay a little bit more.

Jason Quinney: Yes.

Doug Hoyes: But they don’t have to pay as much as if they were both bankrupt.

Jason Quinney: No.

Doug Hoyes: So, we factor out the non- bankrupt spouses –

Jason Quinney: Exactly, you use the bankrupt’s percentage of the income.

Doug Hoyes: So, if the penalty calculated, let’s say the family is $2,000 over the limit, if the husband earns all the income and the wife earns nothing, then the husband is paying the penalty on the $2,000.

Jason Quinney: Exactly, yeah.

Doug Hoyes: And the penalty is –

Jason Quinney: 50%.

Doug Hoyes: 50% so a $1,000. However, if both spouses have an equal income, then they’re $2,000 over the limit, then how much is the bankrupt husband going to have to pay?

Jason Quinney: Well, we would take out the 50% of the spouse’s income. And then they would have to pay 50% of that. So $500.

Doug Hoyes: So, $500.

Jason Quinney: Yep.

Doug Hoyes: Okay. So, the spouse’s income does matter in a bankruptcy but not as much as the income of the bankrupt.

Jason Quinney: Exactly.

Doug Hoyes: Okay, so I guess the answer to the question then, we’re going to take a quick break here and come back, but in a bankruptcy, the non-bankrupt spouse isn’t directly affected. But they are indirectly affected because the bankrupt might have to pay more, might have to pay less, it all depends. And they won’t be a great co-signer in the future.

Great, thanks Jason. We’re going to take a quick break and we’re going to come back and answer more questions about joint debts and spouses and how that all works when you’re in financial difficulty. You’re listening to Debt Free in 30.

Announcer: You’re listening to Debt Free in 30. Here’s your host Doug Hoyes.

Doug Hoyes: We’re back on Debt Free in 30. I’m Doug Hoyes and I’m joined today by Jason Quinney who is a Hoyes Michalos trustee. He works in our offices in Barrie, Vaughn and at our Jane and Finch office in the north end of Toronto. Today we’re talking about joint debts, spouses, what happens, who’s liable for what. And what we talked about in the first segment, Jason, was what really matters is who signed for it.

Jason Quinney: Correct.

Doug Hoyes: So, if both people signed for it, both people are liable for it.

Jason Quinney: Yes.

Doug Hoyes: And it doesn’t matter if you’re married or not when it comes to deciding who’s liable for something. It’s all who signed for it, that’s what matters. So, we talked about how a bankruptcy impacts a spouse. If I go bankrupt and my spouse doesn’t. And Jason you said legally, it has no impact on them but it could have repercussions down the road if they’re trying to jointly co-sign for a mortgage or something. So, does my bankruptcy appear on my spouse’s credit report?

Jason Quinney: No.

Doug Hoyes: So, there’s no notation whatsoever.

Jason Quinney: No.

Doug Hoyes: And the only impact then on my spouse’s credit would be in the example of a joint debt again.

Jason Quinney: Correct.

Doug Hoyes: So, if we’re both signed on the debt, I don’t pay because I went bankrupt, my spouse now is on the hook.

Jason Quinney: Yes.

Doug Hoyes: So, what happens if I go bankrupt and we’ve got a $5,000 credit card together? And my spouse says well, okay I’m not going to go bankrupt for $5,000. If they continue to pay it will that have any negative impact on their credit report?

Jason Quinney: No, as long as they continue to pay it.

Doug Hoyes: That’s the key.

Jason Quinney: That’s the key, yep.

Doug Hoyes: So as long as – so, even though I’m bankrupt, that non- bankrupt spouse can keep paying. It’s not a big deal.

Jason Quinney: Yes.

Doug Hoyes: So, what about then with – let’s make sure we’ve clarified that then – so, let’s say my parents co-signed a loan I got. I go bankrupt, what happens to my parents?

Jason Quinney: They will go after your parents for the loan.

Doug Hoyes: And so what advice would you give my parents then? What are their choices?

Jason Quinney: Their choices would be to pay it.

Doug Hoyes: And if they’re not able to pay it, then they –

Jason Quinney: Well, it depends. I mean the parents they could be elderly so they could be creditor proof. So, they may not have to pay it, if they don’t have any assets.

Doug Hoyes: So, just explain what you mean by creditor proof? What are you talking about there?

Jason Quinney: If somebody’s not working. So, if somebody’s elderly and they’re on a pension, they don’t have any assets, they could be considered creditor proof or judgment proof where they can’t get – a creditors not going to be able to sue them and get a judgment against them.

Doug Hoyes: So, and the key is being able to get something from them, I guess.

Jason Quinney: Yes.

Doug Hoyes: So, you can sue anybody for anything.

Jason Quinney: Yep.

Doug Hoyes: The sky is blue I’m going to sue you for it.

Jason Quinney: Yep. Typically judges aren’t going to grant a garnishment against somebody’s pension.

Doug Hoyes: Because in Ontario, and the rules maybe slightly different in other parts of the country, but in Ontario, the Ontario Wages Act is pretty clear. You can only garnishee –

Jason Quinney: Income.

Doug Hoyes: Yeah, wages.

Jason Quinney: Wages, yep.

Doug Hoyes: So, if you have a pension then that can’t be garnisheed. The only exception I’ve seen would be if you haven’t paid your taxes, Revenue Canada has the ability to withhold some or all of your CPP payments.

Jason Quinney: Yes.

Doug Hoyes: Cause they’ve already got their finger in that pot. But, if you’ve got a normal company pension, you haven’t paid your credit card bill, they aren’t going to be able to, under normal circumstances, get a judgment, they can get a judgment but they won’t be able to garnishee that.

Jason Quinney: Yeah.

Doug Hoyes: So, is there any way for the bank to collect from my elderly parents who co-signed this loan before I went bankrupt? What other advice would you give them? In terms of, they’re still banking at the same bank, is that potentially a problem?

Jason Quinney: That could be a problem. If they’re still banking at the same bank where the loan is co-signed with, the bank can go into that bank account and take any money that’s in there and put it towards that loan.

Doug Hoyes: Without having to go to court.

Jason Quinney: Without having to go to court.

Doug Hoyes: Because –

Jason Quinney: Because when you open up a bank account it says in the small print that if you owe them money they can technically take the money.

Doug Hoyes: And I guess even if legally they can’t, well it’s their computer system, it’s not too hard. And so have you actually seen that happen?

Jason Quinney: Yes.

Doug Hoyes: So, if someone is listening to us today saying okay I’ve got a bunch of debts, I know that one of my debts is co-signed by my parents, what kind of – what’s the thought process then? What kind of advice do you give someone like that?

Jason Quinney: I would advise them to open up a new bank account with a different bank, with a different institution.

Doug Hoyes: Got you. So, and that way at least they don’t have to worry about something coming out of their bank account that they didn’t know.

Jason Quinney: Exactly.

Doug Hoyes: And I guess when I’m talking to someone like that I say well if your number one worry is I want to make sure that my parents are protected, then what you could do if it’s a relatively small debt, compared to all your other debts, is you could deal with your parent’s debts first.

So, okay fine I’ve got this $5,000 joint credit card that they helped me get 10 years ago and their name’s still on it, so before I go bankrupt, I’m going to help my parents get that paid down or even paid off which of course means all my other debts are going to be really old. But at least then, they are protected. If they’ve co-signed for my $50,000 student line of credit, well, I’m not going to be able to pay that off, and I guess in that case the best advice for the parents, if they actually do have some income, they do have some assets, they should probably go to the bank, get it switched over entirely into their name, set up a new loan, maybe they can get a better interest rate and deal with it that way. Okay, can I go bankrupt on my own or is it a requirement that my spouse has to go bankrupt when I go bankrupt?

Jason Quinney: No, you can go bankrupt on your own.

Doug Hoyes: And how would I decide whether I go bankrupt on my own or whether I go bankrupt with my spouse?

Jason Quinney: Well, the main thing is you got to look at the debt, so are they joint debts? Is your spouse co-signed on them? Does she have supplementary cards on them? Or you could have common creditors. Do you both have the same creditors?

Doug Hoyes: And so, if we’re both on the same debt, that would be more likely that we would both then have to come up with some form of solution.

Jason Quinney: Yes.

Doug Hoyes: And would it be two separate bankruptcies that we’d be doing or would be doing a joint bankruptcy?

Jason Quinney: No, you could do a joint bankruptcy, or a joint consumer proposal.

Doug Hoyes: And that means it’s one process covering both of us.

Jason Quinney: Yes and it would likely be cheaper.

Doug Hoyes: So, when you say cheaper, how would it be cheaper? Let’s take an example then. So, I’ve got – well, let’s take the example of a bankruptcy. I’ve got some debts, my spouse has some debts, some of them are together, some of them are not. If we both went bankrupt separately as opposed to both going with a joint bankruptcy, the cost isn’t going to be hugely different is it?

Jason Quinney: Not hugely different, but there is a difference because I would have to do two separate files. So, the two separate files, there would be cost on those two separate files.

Doug Hoyes: Because typically as a trustee, you’re going to say there’s a minimum cost, a couple of hundred bucks a month or whatever it is, so if you’re doing two files, potentially that minimum cost could double.

Jason Quinney: It’s going to be that cost times two. Exactly.

Doug Hoyes: The surplus income that we talked about earlier wouldn’t make any difference if it’s two separate bankruptcies or one bankruptcy.

Jason Quinney: No, you’re going to end up paying the same amount.

Doug Hoyes: You’re paying the same amount. So, I guess if you have joint debts or if you have some debts together or you both have debts, then you want to sit down with a trustee and crunch the numbers.

Jason Quinney: Correct.

Doug Hoyes: Okay, should we do the bankruptcy together or should we not? I guess one of the problems with doing a joint bankruptcy is, you only get discharged if both of you complete all of your duties.

Jason Quinney: Yes.

Doug Hoyes: And so what would be a common example of a duty that might not get completed if we did a joint bankruptcy. So, I do what I was supposed to do, my joint person doesn’t, what would be an example of something they wouldn’t do? What have you seen in your experience?

Jason Quinney: Sometimes people get divorced during the process. So, one spouse could take off. Maybe one spouse is sending income and expense statements and the other spouse isn’t. Cause if they’re separated then they got to send in two.

Doug Hoyes: Got you.

Jason Quinney: Other things maybe tax information, maybe one spouse provides their tax information and the other spouse doesn’t.

Doug Hoyes: Or attending the counselling.

Jason Quinney: Attending the counselling, exactly.

Doug Hoyes: So, if there’s any risk that your spouse isn’t going to be able to fulfill all their duties, that might be an option to do two separate bankruptcies as opposed to one.

Great, well I appreciate that Jason. We’re going to take a break and come back to wrap it up. Thanks for being here today to talk about joint debts. You’re listening to Debt Free in 30. We’ll be right back.

Let’s Get Started Segment

Doug Hoyes: It’s time for the Let’s Get Started segment here on Debt Free in 30. I’m Doug Hoyes and today I’m joined by Jason Quinney, who’s a Bankruptcy Trustee and Consumer Proposal Administrator. We’ve been talking today about joint debts, co-signers.

So, Jason I want to talk about joint proposals. So we already talked about a joint bankruptcy and you listed a number of potential areas where you can get into trouble with a joint bankruptcy if one of the parties doesn’t fulfill all their duties. They don’t get their tax information in, they don’t prove their income every month, they don’t attend counselling sessions; I assume that most of those same issues could happen in a joint proposal.

Jason Quinney: Yep.

Doug Hoyes: Let’s start with the basics then. What is a joint proposal, what does that mean?

Jason Quinney: A joint proposal is when two people file a consumer proposal together.

Doug Hoyes: Okay, so instead of us filing two separate ones, we do one together. Why would we do a joint proposal?

Jason Quinney: If you have common creditors or joint debts, joint creditors.

Doug Hoyes: So, then it kind of makes sense.

Jason Quinney: Yes.

Doug Hoyes: Now is it going to be more expensive or less expensive if I file a joint proposal?

Jason Quinney: It would be less expensive.

Doug Hoyes: So, let’s take an example, then. Not that I don’t believe you but let’s actually crunch the numbers, then. So, we’ve got, between us we’ve each got let’s say $30,000 worth of debt, and most of that debt is joint. We both co-signed a $25,000 line of credit. So, in order to file a joint proposal you said we have to have commonality of debt. So, obviously if we both have a $25,000 line of credit, that’s – our debts are substantially similar. So, if I file two separate proposals, walk me through the math then.

Jason Quinney: Okay. So, if you file two separate proposals we would have to look at both. The amount of debt would be 100% for both separate files. So, we don’t split the debts, you can’t split the debts in half.

Doug Hoyes: So, I’m going to do a proposal, my debts are $30,000.

Jason Quinney: Yep.

Doug Hoyes: And let’s assume just to keep it simple here I don’t have a whole lot of assets, I don’t have a whole lot of surplus income. What kind of numbers am I going to have to offer to get the creditors to accept that proposal?

Jason Quinney: Probably around 10 to 12 thousand.

Doug Hoyes: So, something around a third, that’s kind of the typical number that most of the big banks are looking for, sometimes it can be less, sometimes it can be more. So, I go and I file a proposal, I got to pay $10,000, $12,000, whatever, my spouse is going to have to do the same.

Jason Quinney: Exactly.

Doug Hoyes: So, the total cost for us to do it individually –

Jason Quinney: It’s going to cost you $20,000.

Doug Hoyes: Whereas if we did one proposal together.

Jason Quinney: It would be $10,000.

Doug Hoyes: Okay, so that’s kind of a no brainer in that case.

Jason Quinney: Exactly.

Doug Hoyes: Now why can’t the banks figure it out when we both file a proposal separately on the same day that it’s both the same debt?

Jason Quinney: I don’t know.

Doug Hoyes: That’s just the way it is.

Jason Quinney: Yep.

Doug Hoyes: Okay, so it doesn’t make sense, but that’s just the way it is.

Jason Quinney: That’s just the way it is, yep.

Doug Hoyes: It all comes back to something we said in the first segment which is you are 100% liable for 100% of the debt. They don’t get split in half. So, if we got separated, but we still had all this debt together, could we still file a joint proposal?

Jason Quinney: Legally yes, you could if you’re separated. I wouldn’t want to do that.

Doug Hoyes: Why not?

Jason Quinney: Because there’s issues, because I mean a lot of the time there could be bantering between the two, the separated couple.

Doug Hoyes: I mean by definition we’re separated, so I guess we’re not getting along.

Jason Quinney: Yep.

Doug Hoyes: And so you’re afraid that if it’s going to be a five year proposal that the chances of us getting along for five years are kind of slim.

Jason Quinney: Exactly, yes.

Doug Hoyes: So, if I said okay we’re separated but I’m going to help my ex out by making all the payments in the proposal, legally that’s fine.

Jason Quinney: Sure, yeah.

Doug Hoyes: Practically though you worry about that.

Jason Quinney: Yes.

Doug Hoyes: Because if I don’t make the payments –

Jason Quinney: Then the other person’s – the proposal’s going to be annulled.

Doug Hoyes: Their pouched. And when you say a proposal’s annulled, what does that mean?

Jason Quinney: Well, if you fall three months in arrears, so if you fall three months behind in payments in a consumer proposal, then the proposal’s automatically annulled. So, it’s automatically cancelled.

Doug Hoyes: Okay, so you can be a little bit behind but if you get too far behind you’re toast.

Jason Quinney: Exactly.

Doug Hoyes: Have you ever done a consumer proposal for people who are separated?

Jason Quinney: No, but I’ve done consumer proposals where people get separated.

Doug Hoyes: In the middle.

Jason Quinney: In the middle.

Doug Hoyes: And some of them work, some of them don’t.

Jason Quinney: Yes. Most of them tend not to work.

Doug Hoyes: Yeah, it’s a bit of a risky situation. And part of it’s just simple math, I mean when we were together we were both earning X number of dollars a month, we had one mortgage payment, one rent payment, one phone bill, one cable bill. Once we get separated, our incomes don’t go up. But now we’ve each got our own rent, our own living expenses, so it’s a lot more difficult than to be making payments. Exactly, that becomes the practical consideration

Jason Quinney: Can they still afford to make the payments?

Doug Hoyes: Yeah and if they can’t – so, at that point what options do you have?

Jason Quinney: Well, you could go bankrupt, you could file a bankruptcy.

Doug Hoyes: And can you just split the proposal in half and I’ll pay half and you pay half?

Jason Quinney: No.

Doug Hoyes: So, that’s not really an option. I mean I guess you could –

Jason Quinney: You could, I mean half the person could be making half the payment, the other half could be making the other half the payment.

Doug Hoyes: So, the proposal is still exactly the same from the creditor’s point of view, it’s just that you’re paying for some of it and I’m paying for some of it.

Jason Quinney: Yep.

Doug Hoyes: But practically speaking a lot more difficult to do.

Jason Quinney: Yeah.

Doug Hoyes: Well, great I appreciate that Jason. Joint proposals they work in some cases, they’re not the perfect option in other cases, that’s a good way to end it. You’re listening to the

Doug Hoyes: Welcome back, it’s time for the 30 second recap of what we discussed today. On today’s show Jason Quinney explained that just because you’re married does not automatically make your spouse liable for your debts. And we discussed the difference between joint and supplementary accounts and what happens to co-signers in a bankruptcy. That’s the 30 second recap of what we discussed today.

I know we emphasised it many times during the show, but it’s a very common misunderstanding so I’ll say it again. You are only liable for debts you signed for. Just because you’re married does not automatically make you liable for your spouse’s debts. However, if your spouse has debts it may indirectly impact you, so it’s important to understand all of the implications of joint debt and debt owed by you and your spouse. So that you can come up with the debt management options.

That’s our show for today. Full show notes are available on our website including details on joint and co-signed debt. So, please go to our website at hoyes.com, that’s h-o-y-e-s-dot-com for more information.

You made the decision to deal with your debts. You met with a trustee, filed bankruptcy and have a plan to get your fresh start. So why are you still receiving calls from collection agents telling you to pay up?

You’re sure you gave all the information to your trustee but you just got a notice in the mail that one of your creditors is going to take you to court if you don’t start paying. Or suddenly, after being quiet for so long, the phone has started ringing.

Don’t panic! It could be that your creditors simply do not know about your bankruptcy and there is an easy solution.

Bankruptcy Is An Automatic Stay of Proceeding

When you file for bankruptcy, the stay in a bankruptcy is the legal process that stops creditor actions. This stay is effective the day you file bankruptcy. This means that creditors do not have the legal right to continue the collection process. So why are they still trying to collect money?

Part of the process of filing for bankruptcy is for your trustee to forward copies of your bankruptcy documents to all creditors listed in your statement of affairs. The process of creditors updating their information however can take time.

Many creditors have large collection centres, or hire someone to collect their debt, or they may have sold your debt to another collector . They are trying to collect on that debt and may not know or have noticed that you have filed bankruptcy. It could be that they may have just received your information (if the debt was sold) and it was not up-to-date. They may even think if they just “bother” you enough you might still pay them.

You may have accidentally missed mentioning a creditor to your trustee during the preparation of your documents so they don’t even know you filed a bankruptcy or proposal. That’s OK, honest omissions can be resolved by contacting your trustee and having them forward your documents to this new creditor.

What To Say To Your Creditors

If a collection agent calls you, don’t be afraid to talk to them. Here is what you should say:

Advise them that you have filed bankruptcy or a consumer proposal.

Notify them of the date that you filed, your estate number if you have it and the name of your Trustee in Bankruptcy.

Ask them to contact that trustee to confirm the information. Sometimes a creditor will ask you to contact the trustee and have the trustee call them. No problem, at Hoyes Michalos we are happy to contact creditors on behalf of our clients if they continue to receive collection calls. Simple ask for their name and phone number and give that information to your trustee.

If you are getting mail regarding your debt, send that to your trustee so that they can contact the company to remind them of your bankruptcy and provide them with any documents that they may need.

The hard part is deciding to file bankruptcy to deal with you debt. Once your bankruptcy is filed, as long as you complete all of your bankruptcy duties, you are on your way to getting your fresh start. Don’t stress if a collector calls. Let them know you’ve filed. Once all your creditors, and their agents, are up to date with the situation that should stop the calls. If it doesn’t contact your trustee for help. It’s that simple.

If you need the benefit of creditor protection provided through the Bankruptcy & Insolvency Act, only a Licensed Insolvency Trustee can help. We can stop wage garnishments and collection calls. Contact Hoyes Michalos today for a free, no-obligation consultation so we can give you a plan to deal with your debts.

On today’s show talk with licensed mortgage agent, Mark Moreau to get his take on loaning against your home. Mark has worked in the financial services industry for 30 years and deals with a number of lenders in Ontario. He talks about the process of refinancing a home through a secured line of credit or second mortgage and explains how to know when it’s right to combine your debt into one monthly payment and when it’s better to seek out other options. We contrast this with Licensed Insolvency Trustee Leigh Taylor’s view on high interest debt consolidation loans if you have poor credit.

How to Refinance if You Have Bad Credit

If you have below average credit, when considering whether to consolidate, you need to look at interest rates because your new consolidation loan may not necessarily be at a lower rate of interest. You may be able to lower your payment by extending the term over a longer period of time, but the interest rate is, generally speaking, going to be higher because you’re a higher risk. This can prove costly and may not help you eliminate your debt.

Instead of treating the problem, a debt consolidation loan does very little except just put the problem off for a couple more years. It’s important to remember that debt consolidation does not reduce your debt, instead, it replaces several debts with one new debt. Your total debt load stays the same, so it is up to you to make sure the finances work so that you are paying down that debt and solving the overall problem.

For “A borrowers” or people with good credit the process of refinancing is fairly straightforward and can be done through a traditional bank or mortgage broker (A lenders).

For those with poor or damaged credit, although still possible, the process will involve more checks and documentation, and may need to be completed through a B lender that is willing to do some out of the box things to get you approved for a debt consolidation loan.

Mark explains that to start the process, the first step is to get your house appraised to know its true value.

Next, he would create a profile for the client, assessing whether they have good or bad credit to determine which type of lender they need to go through to re-finance the home. The difference between what kind of lender you use lies in the urgency for debt consolidation. Mark explains,

…if it’s a self-imposed debt consolidation…if you’ve just decided that you’ve got too many credit cards, you want to address the situation but your credit’s in great shape, then that kind of debt consolidation is really just an equity take-out. And we can get that done at almost any bank.

However, if your thinking about consolidating your debt because of delinquency on your accounts and you’re receiving collection calls, although possible, different strategies are needed.

Secured Lines of Credit

A lot of banks and lenders are pushing home equity secured lines of credit, or HELOCS, right now which can be in the form of a pure line of credit or a blended multi-product. People are using HELOCs for more than just home renovation. Many are using them as a means to buy a car, pay off debt or as a budget balancing emergency fund.

The good news about secured lines of credit are that it’s an easy way for someone to access credit; on the flip side, it’s not a one size fits all approach and depending on the type of purchase you’re making, they could have negative implications for people looking to get a loan.

Mark provides an example asserting,

…buying a car over 30 years because you use your line of credit against your house doesn’t make a lot of sense to me.

Moreover, these new secured lines of credit have a different interest calculation than a conventional mortgage and the rates are often much higher if you have low credit.

The real danger of a HELOC happens if you’re kind of using your house as an ATM. So, instead of retiring with a home and a paid off mortgage, with lines of credit we’re starting to see a trend where the house never really gets paid off.

The real issue facing Canadians is that we are no longer paying down debts; instead, we keep reusing them. The problem with this approach is that it creates a ballooning of balances that can soon lead to having to file a bankruptcy or consumer proposal to get out of the debt trap.

FULL TRANSCRIPT show #37 with Leah Taylor and Mark Moreau

So, you’ve got a bunch of debts. You owe money on three different credit cards, and a payday loan and you still owe some money on an old cell phone bill. You’ve got a job and you’ve got money coming in every month, but it’s hard to juggle five different debt payments every month all on different days in addition to all of your regular bills. Wouldn’t it be great to consolidate all of your debts into one monthly payment? No more juggling your pay cheque to make a bunch of payments every month, you would just have one easy monthly payment. Sounds great, right? Debt consolidation does sound great and in some cases it is a good idea. Other times not so much.

Today on Debt Free in 30 we’re going to talk about debt consolidation; the pros and the cons, the good and the bad and the ugly. A few weeks ago the guest on my show was Leigh Taylor and I asked him if debt consolidation was a good idea. Here’s what he had to say.

Leigh Taylor: People somehow mistakenly think that one payment of a thousand dollars is more manageable then ten payments of a hundred dollars a month. It’s slightly more convenient but that’s about it. You really have to look at things like interest rates.

When people look for consolidation loans it’s usually because they’re having trouble financially and they’re trying to do something to alleviate the situation. If they’ve got a bunch of credit cards they can’t pay off and they go to a financial institution, a high risk lender let’s say and that lender says well I’ll give you a loan and consolidate it, it isn’t necessarily going to be at a lower rate of interest. It may be over a longer period of time, sure, but the interest rate is generally speaking is going to be higher because you’re a higher risk.

Now there are – the other side of the sword as I was saying, is that if you have short-term debt, let’s say a bunch of credit cards and you’re paying somewhere from 18 to 22% interest on it, it might be wise to let’s say roll that debt into let’s say a second mortgage. If you’ve got some equity in your house you could probably roll it into a second mortgage for somewhere around 6 to 8%. You can spread the payment of that mortgage over a number of years, sometimes second mortgages can go for 15 years. And what that does is it reduces the amount of interest that you’re paying on it. It can then be that you pay it off quicker because what you save on interest, you simply put back in to cover the principle again.

By spreading it over a number of years you can create the solution to the cash flow problem. You just don’t have enough money to pay the short-term debt every month and it can spread that out over a period of time. And that can solve a financial problem.

Now, the problem often times related to that is, people don’t change. The lifestyle habits that they created, spending habits etc. that got them into the difficulty and created a whole bunch of credit cards, oftentimes doesn’t change. So, then they end up with a consolidation loan, now they find they have some extra money left over every month because of the cash flow improvement and they don’t change their spending habits. All too often we see people that went through the consolidation route only to end up four or five years later to end up with a bunch of credit cards again, maybe the same ones. And now they’ve got a bunch of credit card debt at 18 to 22% plus a consolidation loan that’s been going on for four or five years and they find themselves pretty well strapped without too much of a solution other than bankruptcy at that point in time.

Doug Hoyes: So, the consolidation loan treated the symptom, it didn’t treat the problem.

Leigh Taylor: Right. So, unless you really get into the good budgeting and good financial management to keep you out of debt and put you back on track, the consolidation loan has done very little except just put the problem off for a couple of years.

Doug Hoyes: So, the key point here is that before you consider signing up for a debt consolidation loan, you have to ask yourself an important question. Why am I in debt? The answer of course is because you spent more than you brought in, that’s the real issue. So, will getting a debt consolidation loan solve your budge problem? No, it won’t.

So, you’ve got to address the cash flow issue first. If you’re in debt because you were out of work but now you’re working and have a good job you may have already solved your cash flow problem so a debt consolidation loan may be a good way for you to lower the interest rate you’re paying and get back on track. But if you’re in debt because you have a fancy house and expensive car and you go out for dinner at expensive restaurants five times a week, a debt consolidation loan will not solve your problem, it might buy you time, but it won’t help you reduce your debt. You have to deal with the underlying cash flow issue first.

So, let’s assume that you dealt with the cash flow problems and your budgets in good shape but you have some high interest rate credit card debt that you’d like to deal with. You want to replace your high interest credit card debt with a lower interest rate debt consolidation loan.

We all know that the lowest possible interest rates are on home mortgages. Banks are willing to give you a good deal on a mortgage because it’s secured by a house. If you don’t pay, they take the house. So, they’re almost always guaranteed to get paid. It’s low risk lending, so you get a better rate. So, is getting a mortgage a good strategy as a debt consolidation loan? How does it work? What kind of deal can you get? To find out I’m joined by a mortgage expert so let’s get started. Who are you and what do you do?

Mark Moreau: Thanks Doug. My name is Mark Moreau. I am licensed mortgage agent for Ontario. I’ve spent the last 30 years in financial services working for many of the major banks, working for some of what we call “B” lenders.

In the past I’ve written policy for the major banks as well as run the sales for nationally at all sorts of things. Right now I’m, as I said I’m a licensed mortgage agent so I deal with a number of lenders in Ontario including banks, all the way through to the private lenders. So, my approach is enter a situation, try to figure out what the customer’s needs are and try to figure out what the best solution for them is. And because I’m a mortgage agent I’ve got lots of flexibility and lots of options available.

Doug Hoyes: So, we’re talking about debt consolidation and re-financing. So, what does it take? Explain to me what does it take to re-finance my house, to borrow some more money so I can pay off some existing debt?

Mark Moreau: Well, the starting point is really around where you are in terms of debt, where your credit history is and all those sorts of things. So, we’ll start with the simplest one. We’ll start with the “A” borrower. And the A borrower is classified basically as a bank borrower, right? So, you’ve got clean credit, you’ve got an income, you’ve got all those wonderful things. Those kinds of restructurings are fairly straightforward and easy in general. The things that you require are pretty much all the same all the way through.

On the other side if you get a customer who’s got some damaged credit or perhaps some fudged credit, then you’ve got a different situation altogether. It’s still possible and a lot of opportunities and a lot of flexibility there but there is a slightly higher need for more documentation and certainly more checks and that sort of thing. The biggest difference between those two though is that, to your point earlier, the banks like to lend to the borrower. So, that’s why they lean towards the low risk customer who’s got great credit history, has got the income and everything else.

The B lenders focus more on real estate. So, they focus first on the security. So, that’s a good news and a bad news story because those lenders will do some things that are outside the box for an A lender which in the case of somebody who is really credit challenged gives them more opportunities and a lot more flexibility then I think people really know about.

Doug Hoyes: So, that’s a key point then. An A lender, which or I guess an A client can go to a bank.

Mark Moreau: Yep.

Doug Hoyes: And the bank says how much income do you have? We’re looking at you specifically whereas if perhaps I’ve had some challenges in the past, I’ve gone through a bankruptcy or proposal, I’ve got a whole lot of debt, then the bank, not so eager to look at you. You’re then going to a different lender who is going to place more emphasis on the value of the real estate their going to be financing. Is that what you’re saying?

Mark Moreau: Yeah in essence that’s it. So, it goes back to what I said my approach was initially. So, what we generally do is we’ll take a look at the client’s situation. And wherever we can get the client the best deal and by best deal I don’t just mean rate, I mean in terms of what actually can be done to help them in their situation? That’s where we’ll go to it. As I said we’ve got lots of flexibility. The banks will stop generally at 80%. CMHC as an example, will not do credit restructuring kind of deals but we got these other B lenders that that’s their playground, that’s where they’re going to like to go.

Doug Hoyes: Well, I’d like to hear how all that stuff works. So, what we’re going to do is take a quick break and then we’re going to come right back here with Mark Moreau on Debt Free in 30. And figure out exactly what does it take to get a re-financing done. We’ll be right back.

Doug Hoyes: We’re back here on Debt Free in 30. I’m Doug Hoyes my guest today is Mark Moreau and we’re talking about debt consolidation and more specifically debt consolidation when you’re using your house as collateral.

So Mark, I want to throw at you a scenario here. So, let’s assume I’m sitting in your office right now and I tell you that I bought my house a few years ago and it’s gone up in value and I just had local real estate agent tell me it’s worth $400,000. My mortgage is $250,000. I’ve got $50,000 in credit card debt I’d like to pay off. So, what’s it going to take for me to borrow $50,000 against my house so that I can use the money to pay off my debt?

Mark Moreau: Well, Doug the starting point for all of this is the house itself, obviously. So, even though a real estate agent might have given you a value, one of the first things I ask to be done is we have to get the house appraised. And just to establish that $400,000 is the appropriate amount or the value of the house at that time. Because all of this lending is really driven off of ratios, the amount of debt to the value of the property.

Doug Hoyes: So, just on the appraisal then. So, how does that work? Who do you use to do that? Do I have to arrange it? What’s that going to cost me? How does that work?

Mark Moreau: Well, appraisers, there’s a number of appraisers in every community as well as some national organizations as well. It’s really determined by the lender that you’re going to use. Some of them are very adamant as to which appraisers get used, that sort of thing. But in general it’s very, very quick and easy. The work is on my side of the fence. I’m the one who orders the appraisal. Once I’ve determined where we’re going to go with the loan, because certain appraisers fit certain lenders and certain ones don’t, as an example. In general you’re looking at a price tag of about $250 to – I’ve seen them as high as $350 for residential mortgage, but when you get up into the higher end that’s usually because they’re rural properties or –

Doug Hoyes: Something more complicated.

Mark Moreau: Yeah investment properties as an example. So, if you’ve got a multi unit, if you’ve got a four plex that sort of thing you got rental income then there’s a little more work required by the appraiser.

Doug Hoyes: And is that something that I would just pay directly for? Is that how that would work then?

Mark Moreau: Yeah. In terms of brokering and in terms of getting that re-finance, whether you’re talking to a bank or whether you’re talking to a broker such as myself is that’s the one piece of work that has to be done upfront before we can actually move forward with anything. Whether you’ve got great credit and you’re moving forward or whether you’ve got fractured credit, we still have to start with the house. Now that’s the only upfront cost that’s involved in general with any of these kinds of transactions.

Doug Hoyes: Okay, so the first step is the appraisal. You’re going to bring someone in, figure out what the house is worth. What happens next then?

Mark Moreau: Well, just working off of the scenario that you gave me in this case if you take the $250 plus the $50,000 in credit card consolidation. Let’s assume that the house is worth $400,000 that $300,000 is 75% of the $400,000. So, the next step is determining what’s the profile of the client? Do they have good credit? Do they have bad credit? If they’ve got good credit this is pretty straightforward and easy. We can go to a regular bank or we can go to really a mortgage bank. So, they operate and have the same rates and similar products as the regular banks do, quite frankly. Those are pretty straightforward.

The advantage to working with somebody like me though is that quite often I can actually get you a better deal and a better rate than you can get through the branches. If you’re – and on the other side of the coin, you’ve got a B client and by B we’ve already determined that’s what we mean, so we’re in damaged credit area (not necessarily damaged credit but we’re in a tougher spot). Then at that point we’ve got the same process basically. So, we’ve got to get the appraisal done and then we’ve got to find the appropriate lender.

Doug Hoyes: And so the appraisal’s done. So, in the scenario I gave you, it’s pretty simple.

Mark Moreau: Yep, pretty straightforward.

Doug Hoyes: Cause you said it was a – it’s going to end up being 75% loan to value. Meaning the mortgage at the end of the day is 75% of what the property’s worth. So, let’s make it more complicated then. Let’s say it’s a higher number than 75%.

Mark Moreau: Yeah, again the first question is, what’s the condition of the customer’s credit? So, A credit you’re pretty good to go 80% or even above that.

Doug Hoyes: So, 80% and what’s the magic about 80%?

Mark Moreau: The magic of 80% really stems from the Bank Act. So, banks under the Bank Act are required to not lend above 80% percent without having a mortgage insurer in place.

Doug Hoyes: So, let’s talk about mortgage insurance then. What are you talking about there?

Mark Moreau: Well mortgage insurance is really insurance protection for the lender. So, it protects them against default on the mortgage. So, many, many years ago, banks, within the Bank Act, determined that banks can lend on their own volition up to 80% of the value of the property. Once they go beyond that they can still lend, but they have to get an insurance policy in place. And those insurance policies are provided by, predominately by CMHC, a company called Gen Worth or Canada Guarantee.

Doug Hoyes: So, there’s three companies, the biggest one being CMHC and if I’m not mistaken CMHC is actually me, right? Cause that’s a government of Canada thing and so it’s really my money that’s supporting that I guess.

Mark Moreau: All of our money, yes.

Doug Hoyes: All of our money. Yeah, I guess I’m not the only tax payer in Canada.

Mark Moreau: If you will take that on I would be happy. [laughter]

Doug Hoyes: No, no I can’t afford this country let me tell you. So, if I’m re-financing my house, if I go over 80% loan to value, the lender has to have insurance either from CMHC or Genworth or whomever.

Mark Moreau: Just let me clarify that a little bit. If they are a bank, an institutional lender that has to abide by those rules, so either the Bank Act or some of the other trust company acts and that sort of thing, a Credit Union is an example, then they’re forced by law to impose that insurance. Private lenders, mix, some of the secondary lenders don’t have to have that insurance in place, but they’ll do their own kind of self insurance. So, when you take a look at the two, it’s really comparing different kinds of apples, but they pretty much operate the same way.

Doug Hoyes: So, if I was a really rich guy and I had millions of dollars and I wanted to start a mortgage company, I could do that.

Mark Moreau: Yep.

Doug Hoyes: I could loan to whoever I wanted, I wouldn’t have to have mortgage insurance. But realistically like you say I’m going to price it accordingly then. And so as a consumer you’ll probably end up paying something similar to it one way or the other, I guess is what it comes down to.

Mark Moreau: Yeah, basically if we can just take a little bit of tangent here, when you have to get mortgage insurance in place, it’s done on a premium basis which is a percentage of the total amount of the mortgage that’s going to go out. That premium gets added to the value of the mortgage.

So, in this case we said $300,000 when you add the fees you’re going to have a mortgage that’s going to be more than $300,000 because the insurance premium is going to be in there. So, when you’re talking about CHMC and – let’s just stick with a purchase for a second cause it’s a little bit cleaner, the rate of fees is between .6% and goes up to roughly 4% right now or 3.5%, somewhere in that range. When you’re in the B market, the fees, or the premiums rather are pretty similar. Now they don’t necessarily call them premiums, they’re going to call them fees, lender fees, that sort of thing. But you’re within a point or two of that so they’re pretty comparable, quite frankly.

Doug Hoyes: Got you. So, 80% is the maximum if I’m re-financing my house. What if I’m buying a house brand new?

Mark Moreau: Well let me just correct something there. 80% isn’t the stopping point. 80% is the stopping point where you need insurance.

Doug Hoyes: Okay.

Mark Moreau: Okay, so if you’ve got really clean credit and you want to re-finance beyond that then we can get it done at a bank and we can get it done with CMHC insurance on it. If you’re doing a debt consolidation though, so you’ve got some fractured credit and it is really, we’re trying to clean up a mess, then CMHC will stop. They don’t do default management situations on their insurance, but all the B lenders do.

Doug Hoyes: Got you. So, what’s the maximum I could go to then in that scenario? So, let’s say fractured credit but I have a house with equity in it. I can go over 80% you’re saying.

Mark Moreau: Yep.

Doug Hoyes: And can I do that with a bank through CMHC or am I pretty much with a B lender at that point?

Mark Moreau: Again, it comes down to what is the – if it’s a self imposed debt consolidation as an example, if you’ve just decided that you’ve got too many credit cards, you want to address the situation but your credit’s in great shape, then that kind of debt consolidation is really just an equity take out. And we can get that done at almost any bank.

If however you’re under pressure, so you’ve got some delinquency on your accounts and those sorts of things and you’re getting calls from creditors and that, people of that elk, then you’re in a different category. So, there are limitations on whether or not we can go over that 80% with CMHC or Genworth or Canada Guarantee in place.

Doug Hoyes: So it is possible, it’s certainly not guaranteed. So really what you’re saying is it’s a lot easier to borrow before things get really serious.

Mark Moreau: Yeah, I mean that’s the end of the equation is that. I mean you sort of led into it before, is the time to get this under control is before it becomes a problem, quite frankly.

Doug Hoyes: And under those scenarios it is possible to get decent rates, decent values but once you’ve got lots of judgments and things on your credit report, it’s going to be a whole lot more difficult.

Mark Moreau: Yeah, it’s well, it’s going to be more difficult, let’s put it that way. So, going back to your original question, if we’re in that category then we slip into what I call the B market, in that case we can go, actually I’ve seen some deals go 100%, but not very many but you can comfortably get to 85, 82, 85 and even up to 90. I just recently did one that was 90%. With capitalized fees takes us slightly over that.

Doug Hoyes: Which I guess is why – that’s why you deal with a mortgage agent, you’re able to shop the market, find the best deal and help people get the deal that they need. So, I appreciate that.

We’re going to take a break and come back to wrap it up here. My guest today was Mark Moreau. You are listening to Debt Free in 30.

Let’s Get Started Segment

Doug Hoyes: It’s time for the Let’s Get Started segment here on Debt Free in 30. I’m Doug Hoyes and today my guest is Mark Moreau. We’re talking about mortgages and debt consolidation. There’s a lot of new things out there, Mark. Why don’t you tell me about some of the new products that you’re seeing in the mortgage market?

Mark Moreau: Well, there’s lots of offer out there, Doug. One of the big pushes by a lot of the banks and a lot of the lenders right now is for secured lines of credit. And they come in a couple of different flavours; either there’s a straight up line or credit or they come as sort of a blended multiple product offering. So, some of those have a mortgage component so the mortgage that you and I would understand and know. So, it’s got a term and a rate and all that kind of good stuff.

But attached to that is a line of credit. What people don’t really understand is that the banks do this for a couple of reasons. First of all it gives customers ready and easy access to the credit, that’s the good news. The bad news is, there’s a whole bunch of other implications that come along with that, that I’m not entirely convinced that people understand. And certainly when I see customers that are trying to get out of – work out situations and trying to correct situations there’s a few gottchas and surprises that can jump up and bite you.

Doug Hoyes: So, let’s think this through then, if I go in and get a conventional mortgage we all pretty much know how that works. There’s, you know, pre-payment penalties but there’s also some good things too. I can take that mortgage potentially with me when I buy another house.

Mark Moreau: Correct.

Doug Hoyes: What are some of the gottchas then when you’re talking about – what amounts to really a secured line of credit instead of a mortgage? And a line of credit sounds good to me, right? Cause that means I can borrow against it, I can pay it down, it can go up and down. With my mortgage, I’m making a set payment every two weeks or every month.

Mark Moreau: Yep.

Doug Hoyes: It’s not changing. And yes, maybe once a year I can pre-pay 10% or whatever I negotiated but it’s basically a loan until it’s paid off. Whereas with a line of credit if I want to borrow some more I can, if I get a tax refund and I want to pay it down I can. That sounds fantastic to me. Why shouldn’t we all just go out and get secured lines of credit instead of conventional mortgages?

Mark Moreau: Well, I’ve always taken the approach that it’s not a one size fits all kind of a product. Certainly with the lines of credit and even these multiple component products are good for certain people, they’ve got great incomes and the ability to repay and that sort of thing. But buying a car over 30 years cause you use your line of credit against your house doesn’t make a lot of sense to me.

Doug Hoyes: I would agree with that.