I have received a significant number of calls from existing clients asking for my opinion on a variety of credit repair loan companies that offer loans to “automatically build up your savings” and/or to “improve your credit score”. The number one concern posed by those asking about these types of credit repair or savings loans is “are they worth it?”

What Are These Companies Offering?

One commonality between each of these companies is that the service they are offering is not always easy to understand. Are they a lender, a credit repair agency or a savings company? The truth is the only way to tell is to do a complete and thorough review and ask a lot of questions. We’ve done some of that for you and here are some of our findings.

Savings Loans

Certain companies, like Refresh Financial, offer to provide you with a loan of up to $5,500 so you can begin building your savings. They tell you that you can use this money for an emergency fund or even a vacation. As an upside they tell you that as you progress with your loan you can save money on interest rates, qualifying for better rates on larger loans like car loans or even a mortgage.

What they really do:

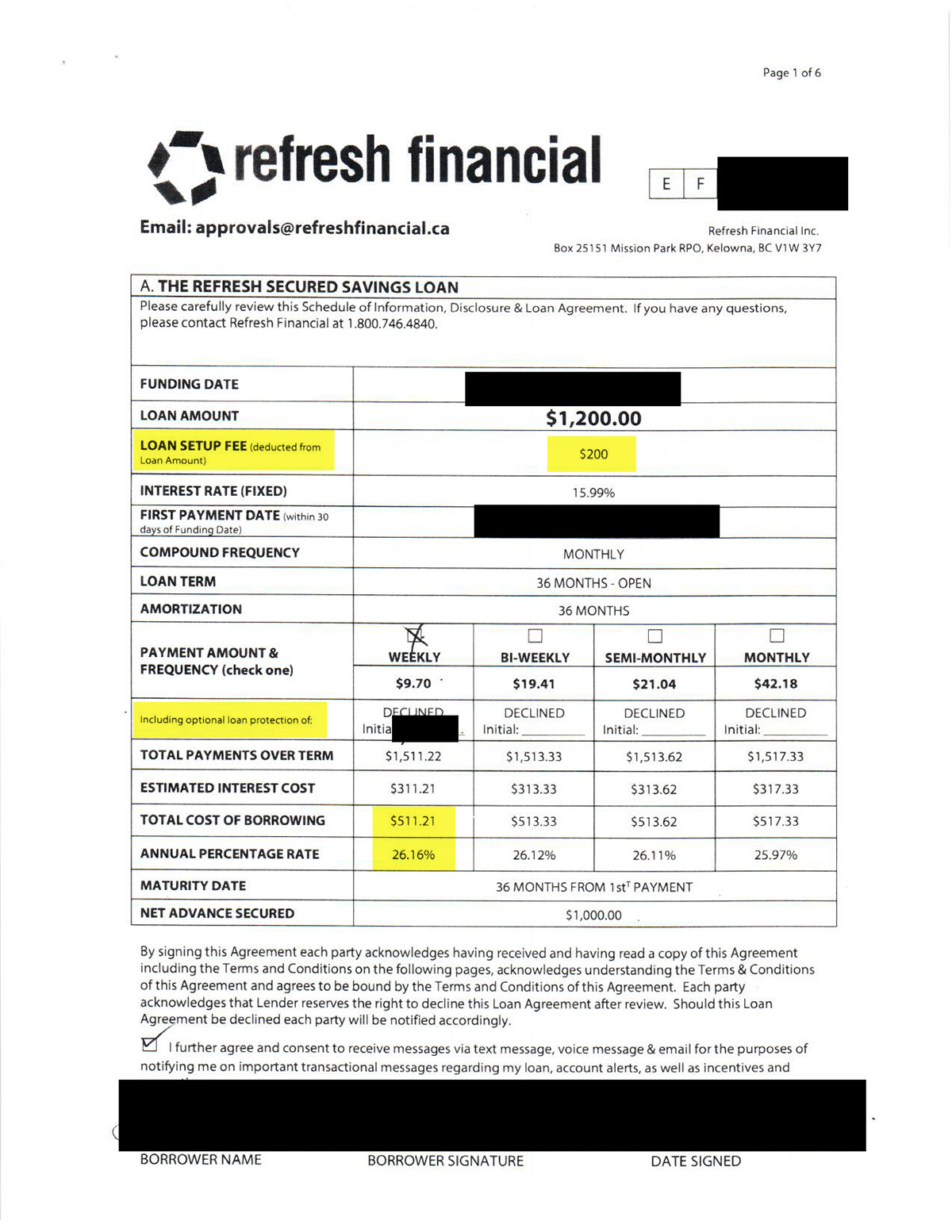

Based on information provided by a client, here’s an example of how these programs work: Our client asked to borrow $1,200. Based on the contract offered (a redacted copy appears below), he will make weekly payments of $9.70 over three years to repay the full $1,200, plus interest, at a quoted rate of 15.99%. However, there is also a loan setup fee of $200. This means that the borrower will pay $511 in interest and fees on a three year loan of $1200, or an equivalent interest of just over 26%.

But what about the savings? Here is how that works: Refresh Financial will put $1,000 (not the full loan amount because they took the $200 setup fee up-front) into a Guaranteed Investment Certificate (GIC). However, this GIC secures the original loan so the borrower does not have access to this money right away. They gain access over time as they make payments. The amount builds slowly, as initially a higher portion of the $9.70 payment goes towards interest. Effectively, the client does not have $1,000 in savings until the end of three years, and those savings cost $1,511 in payments.

We know these numbers from a sample loan sent by a client:

In terms of saving money, the client would be much better off placing $9.70 a week, through automatic payroll deductions, into some form of savings account like a TFSA. If he had, after three years he would have $1,513, plus a little bit of interest, not $1,000.

So if saving money is your objective, you are better off doing so on your own.

But what if you are trying to improve your credit score? These loans are generally reported on your credit report as a term loan, and the loan provider’s position is that a term loan of this type will help you rebuild your credit. While we cannot definitively say how a $1,200 term loan will impact your credit report, the real interest cost is higher than that on a credit card. In the case of a credit card, however, you can use the card for purchases and if you pay the balance in full each month, you can rebuild your credit at a much lower cost ($84 a year).

There are other companies and programs that offer loans that will be reported on your credit report, including some offering credit score improvement programs (some offer you a tablet computer) for a substantial fee or cost.

Ultimately only you can decide if getting a credit repair loan, or getting an unsecured or secured credit card, is right for you. I do, however, have some thoughts on how to rebuild or repair your credit.

How Should You Repair Your Credit?

In general, we advise clients to consider a secured credit card, a small unsecured credit card or a small loan as a way to begin the process of rebuilding credit after filing a bankruptcy or consumer proposal. Used wisely, these forms of new credit after bankruptcy will allow you to rebuild your credit history by keeping your monthly usage well below the actual limit and allow you to show the lender that you can repay your debts each month. I believe the same approach is appropriate for anyone with bad credit today who would like to improve their credit rating (provided they have already dealt with their debts).

You don't need to pay someone to repair credit. Try our free DIY credit repair course. Doug Hoyes gives you a detailed step-by-step plan to rebuild credit on your own.

It is true that from there you will need to show that you can manage larger terms loans such as a small car loan. However, we cannot confirm that borrowing money and paying substantial interest and fees under these forms of credit repair programs will repair your credit score any faster than a less expensive credit card or other alternative.

I recommend you only borrow money if you need to. As the old saying goes, you can’t solve a debt problem with more debt.

Here’s my advice:

First, start with a goal. If you don’t expect to have a need to borrow in the future, don’t waste money on trying to rebuild your credit. If your goal is to finance a car, or even a house, that’s the goal you should work toward.

So, for example, if you want to finance a car, find out what it takes to finance a car at a reasonable interest rate. The car dealer may tell you that you need a $2,000 security deposit and two “trade lines” on your credit report. Now you have a goal. You need to save $2,000 (probably through a savings account or TFSA where you set aside some money every payday) and establish two “trade lines”.

What’s a trade line? It’s anything that shows up on your credit report and could include a credit card or loan. Ask your bank or credit union if they will give you a small loan (perhaps for an RRSP). If they won’t, two small credit cards may be the answer.

Second, crunch the numbers. As shown in the previous example, paying $1,500 to end up with $1,000 in savings may not be your best option. While an unsecured credit card looks more expensive because the interest rate is 29.9% compared to 15% (in our above example), when you compare fees ($200 versus $84) and the fact that you can pay zero in interest if you pay off your credit card balance each month, the unsecured credit card is now clearly much cheaper. Only after looking at all the numbers can you determine how much is a reasonable amount to pay to establish a “trade line”.

It’s up to you, and that’s the most important piece of advice: only you can decide which goal is most important for you, and only you can decide how much you are willing to pay in fees and interest charges to accomplish that goal.

If you are looking a credit repair companies because you have too much other debt to qualify for a loan at a good rate, consider the option of eliminating your old debt first. Eliminating debt is often the first, real step to rebuilding credit. Contact us today for a free consultation. We’ll give you options to be debt free.

As a trustee in bankruptcy, I meet with people every day who are struggling to pay off their debt. In the finance world, it’s not uncommon to hear shocking stories from clients about threatening calls from collection agents or how they got into debt in the first place. On today’s show, I’m joined by Hoyes Michalos Licensed Insolvency Trustee, Howard Hayes, collection agent Blair Demarco-Wettlaufer, credit counsellor, Nicole Olsen from Fitness Financial in Windsor and Licensed Insolvency Trustee at Hoyes Michalos, Rebecca Martyn from our Windsor and Leamington offices to hear some of the scary stories that they’ve heard over the years.

Scary Debt Stories

Each of my guests told me some pretty shocking stories that are unfortunately, all too common. Below are three stories from the episode. Listen to all eight of our guests’ stories in the podcast or read them in the full transcript posted below.

Story #1 – I Was Told I Would Lose My Kids If I Filed Bankruptcy

Howard Hayes tells listeners about a single mother who could not afford to repay her debts and decided to file bankruptcy to get a fresh start. After informing a collection agent that she intended to file bankruptcy, they told her that if she did, child services would be notified and take her children away.

The Moral of this Story: This is absolutely not true. As trustees, we do not report your bankruptcy or consumer proposal with child services and you will not lose your children because you have debt. In this case, the collection agent was willing to say anything to prevent this single mother from filing and to collect on the debt.

Story #3 – My Best Friend Took Out Debt In My Name

Credit Counsellor Nicole Olsen describes one scary story involving two best friends, credit card debt and the sharing of too much information. Jeremy (not his real name), tried to help his best friend who had fallen on hard times. He offered to lend him some money, but instead of cash, gave him access to his bank card and PIN. Rather than taking out a couple of hundred dollars to service his debts, Jeremy’s friend registered his online banking and opened additional overdraft bank accounts in Jeremy’s name, leaving him $4000 in debt.

The Moral of this Story: Don’t share your personal information with anyone (even a best friend). Rather than giving his friend access to his entire account, Jeremy should have taken out the cash so that only that amount could be withdrawn and budgeted for.

Story #6 – Can I Go To Jail For Having Debt?

Licensed Insolvency Trustee, Rebecca Martyn explains a scary story that unfortunately, is not uncommon. One of her clients was receiving collection calls and one day, a collection agent decided to call her 70 year old mom in an attempt to get payment for the debt. The agent told her mom that her daughter would go to jail if the debt was not paid and out of fear, her mother went to the bank, withdrew $5,000, wired it to the credit card company and happily calls her daughter to inform her that she would not be going to jail.

The Moral of this Story: There was no reason for Jane’s mother to pay off this debt and you cannot go to jail for having debt. The collection agent in this scenario used a scary threat to collect on the debt and should not have disclosed information about the debt to her mother in the first place.

Listen to the full episode to hear these scary debt stories:

A man who owed double his original debt due to compound interest.

A single mother who fell behind on payments and received knocks at her door.

A bankruptcy trustee who received collection calls meant for someone else.

A retired man who took on $70,000 in credit card debt, without his wife knowing.

A couple who used payday loans to pay for necessities after losing a job.

Share your scary stories about collection calls and debt in the comments below and what you did to deal with the situation.

FULL TRANSCRIPT show #61

It’s Halloween, so today on Debt Free in 30 we’re going to spend the show telling scary stories. No, we’re not going to talk about ghosts and goblins, but I have invited onto the show a number of guests to tell us scary stories from the world of debt. I’ve got credit councillors and bankruptcy trustees to tell stories of how collection agents try to scare people into paying money. But I’ve also got a collection agent on today’s show to tell a scary story from his point of view. We’ve got a scary story about what happens when you give your best friend your bank card and your pin and what happens when you finance a purchase with a very high interest loan.

So, let’s get to our first scary story about debt. We’re talking about scary stories because today is Halloween and I’m joined now by Howard Hayes who is the trustee with Hoyes Michalos in the Cambridge and Brantford offices. So, Howard give me a story that you heard that you were actually involved in and I want real stories and not something that you just made up. Give me an actual thing, the story that kind of made you say whoa, that’s pretty amazing.

Story #1

Howard Hayes: For sure, Doug. There’s one that always comes to mind immediately that I can think of in my Cambridge office. She was a single mom, had a couple of kids and her situation it was pretty obvious that a bankruptcy was going to be an ideal solution for her. So, we worked on the application form together, I sent her away. There were a couple of bits of information I needed from her before we could file. Everything was great.

The next day I heard a big commotion going on in my office and I could hear someone outside my door using all kinds of expletives, wanting to demand to see me immediately and so I opened my door and there she was, this lady had come back. And the first thing out of her mouth she said, you never told me if I went bankrupt I was going to lose my kids. Never heard anything like that before in my life, I was pretty shocked when she said that. And obviously she was very distraught and upset.

So, first thing I did was asked her to come into my office and sit down. I tried to calm her down a little bit and absolutely reassured her 100% that filing a bankruptcy doesn’t mean you lose her kids. I asked her where she had got the information from. She said it was a collection agent that told her on the phone that morning that if she filed a bankruptcy to avoid repaying her debts, that she was going to lose her kids. I said that was absolutely ludicrous of course. The collection agent apparently had told her that because she was filing a bankruptcy, that apparently the trustee reports the situation to child services, child services automatically assumes she must be a bad parent because she’s not paying her debts, and therefore, she came to the conclusion that that meant that she would lose her kids.

Doug Hoyes: And just so we’re clear on this here, have you ever reported anyone to child services?

Howard Hayes: Absolutely not. It’s nothing to do with child services.

Doug Hoyes: Yeah, we have no dealings with them, whatsoever. So, it’s kind of a ludicrous thing to say.

Howard Hayes: I think the collection agent was just trying to make their commission on collecting the debt and was just trying to think of anything they could to tell the lady to try and discourage her from filing the bankruptcy, which of course it’s an absolute shame that they have to resort to that level. It’s deplorable behaviour really from the collection agencies. But it just goes to show sometimes they’ll tell you anything they can think of telling you to try and persuade you to pay the debt.

Doug Hoyes: And that’s why when you hear a story like that, talk to someone who actually knows.

Howard Hayes: Absolutely.

Doug Hoyes: It is ridiculous and we’re going to hear other stories like that today. Thanks for telling us that one, Howard.

Howard Hayes: You’re welcome, thank you.

Story #2

Doug Hoyes: So, we heard the story from Howard about a collection agent who was lying and basically being quite deceitful to the person who owed the money.

Well, does it ever happen the other way around? Do collection agents hear stories from people they’re trying to collect from who aren’t perhaps dealt with the proper way? So, I’ve asked Blair Demarco-Wettlaufer to come here. He’s been on a couple of shows with us already talking about an insider’s view from the collection agent. So, Blair thank you for coming back. Have you ever had – well, tell me a scary story from your perspective? What do you hear?

Blair Demarco-Wettlaufer: We hear – unfortunately we hear a lot of hard cases from people and we hear some pretty horrible things. Obviously, we can be calm and reasonable. We’re yelled at, we’re sworn at, you know, because we’re not delivering exactly good news.

Doug Hoyes: You’re the bad guy.

Blair Demarco-Wettlaufer: Yeah. I’ve had people use their eight year olds to screen their phone calls. We’ve seen some pretty horrible stuff. But here’s a good example of a scary story. At one point I called a consumer, they owed $850 for a lease on some furniture. And we called them and said this is a curtsey call and you owe $850 and what would you like to do before we put this on your credit rating? And we got called every name in the book and he hung up on us and he called back to swear at us because he was clearly emotional about it. And, you know, obviously we couldn’t work with him so we put it on his credit bureau.

And two, two and a half years later, wouldn’t you know it, he gives us a call. Hi, it’s me, I can’t get a car. And we pulled up the account and I got the inbound call, two and a half years later. Oh, Bob, yes you and I talked two and a half years ago, you said some hurtful, rude things. And he said well can I work out a deal? And I went sure, here’s your balance with compound interest because the leasing company’s been charging you 24% per annum. And it’s almost doubled. The fellow owed $1,500. And really the scary part about this is compound interest. Now that’s the real scary thing, not me. And he asked can we make a deal? And unfortunately, this leasing company gave us no wiggle room, no co-operation and of course he’s calling two and a half years later. The creditor isn’t going to be reasonable or forgive interest when he’s told us to go to heck in a hand basket. And we shared all that information with the creditor and the poor fellow had to pay $1,500, two and a half years later.

Doug Hoyes: And I guess there’s a few pieces to that puzzle there. In some cases, the creditor’s going to say yeah fine we’ll wave the interest, it’s been a certain amount of time. You, as the collection agent, are acting on instructions from them.

Blair Demarco-Wettlaufer: Yes.

Doug Hoyes: So, if they say nope, the interest clock keeps ticking then that’s the way it is. It’s not for you to decide.

Blair Demarco-Wettlaufer: Exactly. And a lot of times if the consumer can get on side with the collector, they can avoid the nastiness. I had one lady, sweet lady, she must have been 80. She came into our office every month in her walker and paid $20 a month because that’s what she could afford. And when she finally came in with a box of 20’s to pay her $6,000 account saying her older sister had died, we were able to work with the creditor and get $2,000 forgiven. Because she had proven to be reliable and taking an attempt to take care of that. And that isn’t as common in this modern age of databases, but it’s still there. So, the really scary thing is interest and consequences.

Doug Hoyes: So, the moral of the story is if you’re straight up and you work with someone, then you’re likely to have a better outcome than if you swear a lot.

Blair Demarco-Wettlaufer: Keep your cool.

Doug Hoyes: Keep your cool.

Blair Demarco-Wettlaufer: It’s just business, keep your cool.

Doug Hoyes: It’s a simple as that. Great, thanks for telling us that story, Blair.

Blair Demarco-Wettlaufer: Thank you.

Story #3

Doug Hoyes: So, there you’ve got two stories about debt collectors, but it’s not just collection agents who can tell scary stories. Credit counsellors also have lots of stories to tell. So, let’s let my next guest introduce herself.

Nicole Olsen: So, my name’s Nicole Olsen and I’m a credit counsellor from Financial Fitness, which is a non-profit credit counselling agency here in Windsor, Ontario as well we have an office in Sarnia-Lambton.

Doug Hoyes: Great, well thanks for being here, Nicole. And when I put out the word for scary Halloween stories, or scary stories that relate to debt, you said hey I got all sorts of them. So, let’s see how many we can get to. So, what I’m going to ask you to do, I’d like you to tell me the stories. I’d like you to change the names of people that you’re telling us. We don’t want to be disclosing any confidential information or anything here. But give me a story, tell me what you got.

Nicole Olsen: Sure. I guess one of the most interesting stories that I’ve had recently is of a client named Jeremy, his name’s been changed, but he’s in his 20’s. His best friend was falling on hard times so Jeremy thought well, I’m going to help my friend out and I’ll lend him some money. So, instead of giving him the cash, he gave him his bank card and his pin number thinking that his best friend would only have access to the couple of hundred dollars that he had in his bank account.

But lo and behold, a month later, Jeremy finds out that what his best friend actually did was he registered his online banking for him and then started opening up bank accounts in Jeremy’s name. And all of these bank accounts he added the overdraft so there were eight accounts that were added in total. And essentially, it put Jeremy in debt over $4,000 to have to pay this back.

Doug Hoyes: Wow, wow. And so, I’m just trying to figure out how this actually happened. So, he gave him his bank card and said here’s the pin. So, I understand that. If I’ve got your bank card and your pin I can go to the machine and take out money. But then he took it a step further and went online and because I have the card number, he could register for online banking. And apparently you can do that just online I guess. You don’t need to provide any further information is that how it worked?

Nicole Olsen: Well, since they were best friends, he had a lot of information about Jeremy. He knew his birthday; he might have even known his social insurance number. Considering Jeremy was willing to give him his bank card and pin number, he might not have been so protective of all his personal information. So, I think that’s where the best friend got most of the information from, was from their relationship.

Doug Hoyes: And because he was registering, he was setting up accounts, which is pretty easy to do online. Would you like to open a new account? Here you go. It wasn’t the same as trying to apply for a car loan or a mortgage or even a credit card where there’s a greater standard of review that the bank would do. It’s only a small account. And you said how many accounts did he open up?

Nicole Olsen: Between six and eight.

Doug Hoyes: Wow, so each account maybe only had a $500 overdraft on it. So, the bank doesn’t look too closely at a $500 overdraft. It’s not like getting like I say a loan or a credit card or something. But when I add up a bunch of them, it ends up being a big number.

So, based on that story, what is the advice you would give people in that situation? If you could turn back the clock and see Jeremy six months ago, before all this happened, what advice would you be giving him?

Nicole Olsen: First and foremost always never, ever give out any personal information, even friends and family. If they need to borrow money then give them the cash. Don’t give them your pin number, that’s something that you really need to keep to yourself. And change it frequently, every six months or so you should be considering changing your pin number so that if it is compromised you’re kind of mitigating all these damages.

Doug Hoyes: And so, what do you do? You just go into the bank and change your pin number there? Is that how it works?

Nicole Olsen: Yep, you can go into the bank and they’ll put your card into a reader and they’ll just ask for your old pin number and then you put in a new pin number and you’re good to go.

Doug Hoyes: Great. So, that’s good advice, keep your confidential information confidential and if you do want to help somebody out, then fine, give them cash because that way you’re only giving them the cash that you can afford to give them. You don’t have to worry about it being any greater of a number than that. So, that’s very good advice. So, tell me another story, what other scary stories have you got?

Story #4

Nicole Olsen: Well, I did have a client, Rebecca, she was a single mother of three and she was collecting Ontario Works, so she’s on a very limited income. And she needed a new bed for her oldest son ’cause he was outgrowing his. So, she went to one of those easy furniture loan stores and signed up to get the furniture delivered and she got into a payment plan. What she didn’t realize was that the interest rate was around 46% interest, plus administrative fees; her payments were really, really high.

So, she made the first maybe three or four payments and then after a while she just couldn’t keep up with having to buy groceries and pay the rent so she fell behind on the payments. And now what’s happening is the store is actually coming to knock on her door, like on her front porch, knocking on her door looking for payment.

Doug Hoyes: Wow and that’s something we used to hear about all the time in the past. And you don’t hear it so much anymore ’cause everything’s done by computer, all the lending’s done by a computer, the collection person might be miles away from you. But when you’re dealing with a local business like that, they’ve advanced the money so they’re more likely to be coming after you and actually knocking on your door. So, what in hindsight would your advice have been to Rebecca? And again, that’s not her real name, but what would your advice have been to Rebecca if you could have spoken to her before she had gone out and financed this mattress?

Nicole Olsen: Yeah, if she would have come into our office, we would have sat down and did a budget with her. We would have talked about if she need anything in the future, thinking about those periodic expenses that come up within a year. We all have them, they all happen throughout the year. And what we need to do is start setting up a plan for them. So, kids, if you have children, they have a lot of periodic expenses, shoes, furniture, clothing, setting that money aside on a monthly basis so you can pay cash for those items. ‘Cause a lot of times if you pay cash, the item is a lot cheaper than if you were to finance it.

So, what happens is Rebecca’s now financing it at almost double or triple the cost of the item, where if she would have saved for maybe six months, $50 over six months she would have had $300 that she could have purchased the bed with.

Doug Hoyes: Yeah because that’s what we’re talking about. If it’s a $300 purchase you’re right. I mean $50 a month is more than what she’s paying on the loan payment now.

Nicole Olsen: Uh huh.

Doug Hoyes: And so, we understand that okay, I mean I’ve got kids too, I understand they grow out of things but they probably didn’t grow out of their bed instantly. And even though you wanted that new bed, well they probably could have survived for a few more months in the old one. Or, you know, done a camp out on the floor in their sleeping bag or something, or whatever. They’d probably like that better than sleeping in a bed I guess.

Nicole Olsen: Sometimes they do. [laughter]

Doug Hoyes: But you’re right, you are much better off putting aside the $50 a month, you know, $10, $12, $15 a week for a period of a few months, rather than being faced with having to make a loan payment of $50 or $100 a month for a much longer period of time. So, you really have to be proactive and look at it in advance.

Story #5

So, there was some great stories from Nicole Olsen who is a credit counsellor based in Windsor. I am going back to Windsor again for our next story. I have on the line Rebecca Martyn, who is our Hoyes Michalos trustee covering our Windsor and Leamington offices. Rebecca, how are you doing today?

Rebecca Martyn: I’m good, thanks for having me Doug.

Doug Hoyes: Thanks for being here. So, we’re talking scary stories that have to do with money and debt. Why don’t you start me off, tell me a story.

Rebecca Martyn: Well, the first thing I want to tell you is actually something that happened to me. Now this was several years ago but I was continually getting phone calls with someone with the same last name as mine. I would have collection agency’s calling me up, they were threatening me, they were telling me that I was harbouring this person, that I was doing everything I could to avoid it. They were assuming that I was this man. I don’t think I have a masculine voice but they were saying I was really this man in a disguised voice, trying to hide from them.

And at the time I was working for a bankruptcy trustee in London. So, I knew a little about collection agencies and what they were doing. So, eventually I just started marking all these phone calls down and I just basically told them, you call me again I’m going to file a complaint against you. And the next time the collection agency would call me I would tell them I’m filing a complaint and at that point the phone calls just stopped. But it’s just to kind of show you that some of these collection agencies, they use means to try to intimidate people. And in the case with me it didn’t work because one, I wasn’t the person they were looking for and two, I didn’t owe the money so I wasn’t going to pay something that wasn’t mine.

Doug Hoyes: And so, what’s the takeaway message there? If people are getting phone calls for a debt that they don’t owe, I mean obviously if you’re getting a phone call for a debt that you do owe you need to deal with it. That’s – the collection agency is just doing their job. But if you suspect that either they’ve made a mistake or they’re doing it deliberately and they’re calling you for a debt that you don’t owe, what’s your advice?

Rebecca Martyn: Well, my advice is just to realize that people do have rights. If someone is harassing you for a debt that doesn’t belong to you, find out who’s calling, get their name, get their phone number, get their contact information. If they still call you after you tell them it’s not your debt, then just file a complaint with the Ministry of Consumer & Commercial Relations against this company.

Story #6

Doug Hoyes: Obviously, the answer is no, don’t go and pay them. Even if it’s not your debt, that’s obviously counterproductive. So, that’s obviously a scary story when people are calling you for debts that don’t even belong to you. So, tell me another story perhaps that had to do with one of the clients or one of the people you’ve helped over the years.

Rebecca Martyn: Well, this one was actually a client of mine who came to see me awhile ago in the Leamington office. She had lost her job, living on her credit cards. So, it’s a story that unfortunately we’ve heard a lot. Got behind on her credit card bills and they went to collection agencies. A collection agency called up her mother, who was a senior citizen in her 70’s, and basically said that your daughter owes this money and she needs to pay it. And let’s just call the daughter Jane, that wasn’t her name, but I’m just going to make up a name so I can talk about a person.

So, the collection agency said that if Jane doesn’t pay this money there’s going to be a police officer at your door and we’re going to take Jane to jail. Mom was really scared. She doesn’t want her daughter going to jail, goes down to the bank, withdraws $5,000, wires it to the credit card company. And she’s probably happy, great now I’ve avoided my daughter going to jail, this is fantastic. I’ve really helped her out. Jane comes home, sees mom all happy. She says oh you’re going to be so happy Jane. You were about to go to jail, but I stopped it. She goes what did you do mom? Well, XYZ collection agency called, they said you had to pay this money or you’re going to jail, so I paid it.

Of course Jane is furious ’cause there was no reason for mom to do that. She doesn’t understand why someone at the bank didn’t stop mom from taking out so much money. Nevertheless, the debts now been paid, it’s gone and then a few months later Jane couldn’t deal with the rest of her debt, she came to see us and she filed for bankruptcy.

Doug Hoyes: And so, the sad part of this story obviously is that someone who was unsophisticated in the manners of money, the senior citizen mother in this case, kind of got scammed into making this payment that she legally didn’t have to make, obviously it wasn’t her debt and didn’t have to make. So, have you heard this story about, you’re going to go to jail if you don’t pay? Have you heard that one before?

Rebecca Martyn: Unfortunately, yeah I have. I have heard the comment that if you don’t pay you’re debt you’re going to jail. And even when clients come to see us, if a collection agency hasn’t specifically implied that or said that, they just have this fear that if I don’t pay my debt, I’m going to go to jail.

Doug Hoyes: And so, do people go to jail if they don’t pay their debts?

Rebecca Martyn: No, they don’t go to jail. Imagine if people didn’t pay their debt and they go to jail; imagine how overcrowded our jail would be from people who didn’t pay their debt.

Doug Hoyes: Yeah because pretty much everybody gets behind at some point. And the way I always explain that to people is there are two different kinds of courts in Canada, there’s criminal court and civil court. Criminal court is if you commit a crime, you kill somebody, you steal well that’s a criminal offence and yes, you can go to jail if you’re convicted of a serious criminal offence.

But not paying your debts is a civil offence, that goes to civil court. And the penalty isn’t going to jail, the penalty would be you have your wages garnisheed, you have a lien put on your house, something like that. So, you’re not going to jail for not paying your debts. If you kill someone, yes you’re going to go to jail but it’s not paying your debts isn’t something that lands you in jail. You know, it’s a great line for a collection agent to use because it’s scary, it just simply isn’t true. So, what’s the –

Rebecca Martyn: That’s exactly right, it scares people, right?

Doug Hoyes: Yeah and that’s why they’re doing it. So, what’s the takeaway message here then for dealing with this kind of situation if somebody is faced with it?

Rebecca Martyn: So, I think the takeaway situation is so if you’re getting calls for a family member or a friend about the debt, just be polite on the phone say thank you for the information, I’ll pass it along. But don’t let the collector intimidate you into thinking that something else is going to happen that can’t happen. And it’s the same thing that we mentioned with the other scary story is that if you owe the debt, work out a payment plan and then just again, realize that you’re right. Like you mentioned, you’re not going to go to jail just because you have an outstanding balance on your Visa, that’s not what jail is there for.

Doug Hoyes: And even if you were going to go to jail I don’t think they’d be putting you in jail in ten seconds. It’s not like it’s going to happen by the end of the day. It’s just ridiculous. So, yes if you want to help somebody out, that’s great if you have the money to do so, fine, give that money to the person and let them deal with it then. But to be wiring money to somebody you don’t even know, who you just heard of, is obviously the wrong approach.

So, those are two very good and scary stories thanks very much for joining me today, Rebecca. We’ll take a quick break and I’ll be back with the next segment right here on Debt Free in 30.

Doug Hoyes: It’s time for the Let’s Get Started segment here on Debt Free in 30. It’s our special Halloween edition and I’ve asked my guests to tell me scary stories about debt. In this segment we’ve got two scary stories, but the main point of the Let’s Get Started segment is to give practical advice as well, so that’s what we’re going to do.

In the first segment Nicole Olsen, a credit counsellor with Financial Fitness in Windsor told us two stories. One was about Jeremy, a young man who made the mistake of giving his bank card and pin to his best friend with scary results. The other story was about a young woman who got caught up with a very high interest finance loan. Those were both stories about younger people.

So, I asked Nicole if she had any stories she could tell me about seniors. Frequent listeners to this show will know that seniors are the fastest growing segment of the population that we help. With low interest rates and fixed incomes, it’s growing ever more common for seniors to get into debt. So, I asked Nicole whether or not she’s also seeing a lot of seniors with debt problems and here’s what she said.

Story #7

Nicole Olsen: Yeah I think that would be our largest growing demographic right now that we’re seeing a lot of seniors coming in with debt. A very familiar story would be the story of Jackie and Frank. They’ve been retired for quite a few years, about 10 years. And they’re in their 70’s, they’re enjoying their retirement. Both Frank and Jackie worked during their careers so they have good pensions.

But Frank had a really hard time adjusting to his new retirement income ’cause we all know, when you’re working, it’s maybe weekly or maybe bi-weekly pay, but when you retire it’s once a month and that seems to be the hardest one to budget for. So, he’s used his credit cards to kind of pay for the extras in his retirement. So, his golfing and all of the outings that he wants to do, going out for lunch with his friends. So, eventually what happened is ’cause he had such a good credit rating throughout his working career, he was able to accumulate over $70,000 worth of credit debt, within a 10 year period of time.

So, they came into see me, we looked at their options. But because Jackie and Frank own their home outright, they really don’t have a lot of options. Because for the most part the creditors are going to say sell your house and pay your debts. So, we had to really work with Jackie and Frank to see what we could do because they really didn’t want to sell their dream home. They had worked their whole lives to pay off this house and now they just had to deal with this debt.

Doug Hoyes: Wow, yeah and you’re right, when you’re retired, your life changes; getting a paycheque every two weeks is a bit different than getting a pension cheque every month. And if you get a little bit behind when you’re working you can work some overtime, maybe pick up a part-time job. Once you’re retired, well there’s no such thing as overtime. So, you’ve really got to go into retirement with no debt.

But then I guess the other piece of advice you’d be giving is yeah you’ve also got to make sure your expenses shrink to whatever your new reduced income is if your pension income is lower than what you were making. That’s really the mistake they made I guess.

Nicole Olsen: Uh huh and having to finance all that debt as well was costing a significant amount of money, for the minimum payments that they were having to make. And Jackie didn’t know about Frank’s debt. So, that was another part of it that caused a lot of problems. There has to be open lines of communication between two people in a marriage.

Story #8

Doug Hoyes: And that certainly becomes a scary story that’s for sure. So, tell me one more. Have you got any stories about a typical couple then? We’ve looked at the younger people, the older people, have you got any stories about someone right in the middle?

Nicole Olsen: Yeah Mike and Kelly would be our typical clients that we would see that are in their 30’s and 40’s. Mike would be working full-time and maybe Kelly is staying home with the kids. And Mike, like many Windsorites that we see, is getting laid off and he’s jumping from job to job. So, what’s happening is they’re getting behind. They’re getting behind on a lot of their utilities, sometimes they get behind on their property taxes and the city or town is starting to talk about foreclosure on the home. So, they’ve eaten up all of their savings if they had any. They’re behind on all of their bills and now they’re having to take out payday loans just to buy groceries and take care of their basic necessities. And so, at this point they’re in crisis mode.

Doug Hoyes: And once you’re in crisis mode, your options are really limited.

Nicole Olsen: Yeah it can be very challenging to figure out what we can do ’cause we just need to stop the bleeding. So, sometimes it could be looking at re-evaluating the budget, sometimes it could be leaving the home, finding a new rental that’s more in their price range. First and foremost, it’s finding steady income, which sometimes can be challenging.

Doug Hoyes: So, I guess your advice in really all these situations we talk about is you’ve got to be proactive. If you’re in an industry or in an economy where you know there’s a good chance you’re going to be laid off in the future, you’ve really got to be planning for that. And I guess the best way to do that is to stay out of debt, but also to have some savings as well.

Nicole Olsen: Having savings yep and looking for skills that are transferable. So, really in the employment market you want to be in a career or in a job that you can take those skills and easily convert it to another position so that you’re not out of work for a longer period of time. Being really on top of the E.I process, so the unemployment insurance process, making sure that you have your Service Canada account open, so, that every single time that you go on lay off you can reactivate that claim and you’re not having to wait so long to receive your first cheque from unemployment.

Doug Hoyes: That’s good advice. So, being proactive and making sure that the government programs that are available to you are easily accessible. You don’t want to be having a time lag on that. Well, that’s great. Those are some excellent scary stories and some great advice to back them up. Thanks very much, Nicole.

Nicole Olsen: Oh thank you.

Doug Hoyes: That’s the Let’s Get Started segment here on this special Halloween edition. I’ll be right back to wrap it up right here on Debt Free in 30.

Doug Hoyes: Welcome back, it’s time for the 30 second recap of what we discussed today. On today’s show we heard many scary stories about debt from trustees, a credit counsellor and even a collection agent. That’s the 30 second recap of what we discussed today.

Of course debt doesn’t have to be scary. There are options for eliminating debt, so, for full details please go to our website at hoyes.com, that’s ho-y-e-s-dot-com, for all the options to make your debt a lot less scary. Thanks for listening, until next week I’m Doug Hoyes, that was Debt Free in 30.

Canadians are receiving threatening and fraudulent phone calls from individuals claiming they work for the Canada Revenue Agency (CRA). They are being told they must act fast to deal with an outstanding tax debt owed to CRA and if they do not pay something right away their assets will be seized or they may go to jail. To facilitate making a payment, the caller will request credit card information. The immediate damage is the charge to be paid on the credit card, but there is also a high risk of identity theft.

In light of COVID-19, fake CRA callers have also been demanding repayment for the Canada Emergency Response Benefit (CERB) and Canada Emergency Student Benefit (CESB). There are official ways to repay the CERB or CESB income supports, but the CRA will never demand immediate payment by Interac e-transfer, bitcoin, prepaid cards, credit cards, or gift cards from retailers such as iTunes, Amazon, or others.

How to identify fraudulent calls

Canada Revenue Agency has a webpage telling consumers to be aware of fraudulent calls. Their advice, if you get such a call, is to hang up and report it to the Canadian Anti-Fraud Centre. CRA has even gone so far as to post a sample phone call so you can more easily recognize these types of phone scams and avoid being trapped by their threats and false information.

Here are some tips on how to identify and handle calls from possible scammers:

Don’t assume because they know your name that the caller is legitimate. It’s easy to find names and phone numbers in many online resources.

Don’t be alarmed by threats of a tax audit, a visit from the police, deportation or other scare tactics. This is what fake callers do to get you to react to them.

Never wire money or send prepaid credit cards or gift certificates to a request over the phone. The CRA themselves say they never ask for prepaid credit cards or payments like that.

Don’t offer personal information. The CRA does not ask for personal information such as your passport, health card or driver’s license.

Be on alert if they suggest you should keep the call confidential. You are always able to contact a lawyer, a licensed insolvency trustee or talk to a family member about your tax problems.

Rather than talking to the caller, tell them you are going to call CRA to verify then hang up. Call the CRA directly at 1-800-959-8281 to see if you owe them money.

If you hear a message on your answering machine, be alert. The CRA does not leave personal information about you or your tax situation on an answering machine. The CRA also will not leave threatening voicemail messages.

Ignore text and social media instant messages claiming to be from the CRA. The CRA has stated that they never use text or instant messaging to communicate with taxpayers under any circumstance.

Always check the CRA website for the newest scam approach. These scammers change their stories frequently.

Always be suspicious when someone calls you at home, threatens you and asks for money.

If you are scared because you do owe money for back taxes you can contact the CRA directly to discuss a repayment arrangement or talk to a bankruptcy trustee. Tax arrears can be dealt with by filing bankruptcy or a consumer proposal if you cannot work out a payment plan with CRA.

If you have already filed a bankruptcy or consumer proposal with Hoyes Michalos and are concerned about any call regarding old debts included in your bankruptcy or proposal, including tax debts, please contact our office. Our team is happy to help you understand how your tax debts will be treated as part of your insolvency filing.

Just like no two individuals’ debt problems are the same, no two consumer proposals will ever be exactly the same either. However the driving forces behind how a consumer proposal is negotiated do follow a similar pattern.

Debt Is Different For Everyone

The size of debts, types of creditors and other factors, like how and when the debt was incurred, will be different in every single consumer proposal ever filed. Debt is incurred in different ways, by different people, for different reasons. The reasons for wanting to file a consumer proposal may be different too; some people file because they face the threat of legal action, some because the size of the debt is too overwhelming to maintain and some because they have recently suffered an unexpected event like a drop in income, marital breakdown or medical problem.

Common Requirements of All Proposals

What all consumer proposals have in common is that they are filed by individuals who find themselves unable to repay their debts. Only if you’re insolvent, do you qualify to be eligible to file a consumer proposal. All consumer proposals filed in Canada must be done so by a licensed trustee and must comply with the rules and regulations outlined in the Bankruptcy & Insolvency Act.

What all consumer proposals must provide for is a greater benefit to creditors than they’d receive in a possible bankruptcy scenario. There’d be no sense in a creditors accepting a consumer proposal if they’d likely see a higher repayment from a bankruptcy.

A trustee experienced in filing consumer proposals with many different creditors get’s to know what individual creditors are looking for and what will work. It’s for this reason that almost every consumer proposal filed at Hoyes Michalos is accepted by creditors.

What this means is that the factors in determining what a consumer proposal will cost are the same for everyone however the end result of the calculation may be different. All negotiations are based on what you own and how much you make. How much you choose to offer however can depend on how fast you want to pay off your proposal and what your budget looks like.

Our video on what a consumer proposal costs explains more:

A consumer proposal allows you to settle your debts for less then you owe. What you pay in a consumer proposal is based on what you and your Trustee can negotiate with your creditors. The golden rule of a successful proposal is that it must work for both you and your creditors. You have to be able to afford the payments and your creditors have to feel they are getting enough to vote yes. Typically, this means your creditors want a little more than they would receive in a bankruptcy. This would include any payments you have to make based on your income, any equity in your home, any other assets you might lose in a bankruptcy. Once all this is added up you will talk to the trustee about how much you can afford to pay each month. A proposal can last up to 5 years, so you can spread out your payments over a maximum of 60 months. Let’s look at an example. Mark meets his Trustee and finds a bankruptcy would cost him $475 a month for 21 months, or almost $10,000. He decides to offer his creditors, $200 a month for 60 months, or $12,000 in a consumer proposal. Mark is happy because he pays less each month then in a bankruptcy and can keep his assets. His creditors vote yes because they earn a little more over time, and Mark pays only what he agrees to in his proposal. He doesn’t pay extra Trustee fees, they come out of his negotiated payments. In effect, Mark’s creditors are paying to administer the proposal. Each situation is different, at Hoyes Michalos we provide you with all of the necessary information to help you calculate the potential cost of a consumer proposal given your specific circumstances. Call us today and we’ll calculate a payment plan for you.

A consumer proposal may be offered over a period of up to five years. Many people take advantage of this to stretch their monthly payments over as long a term as possible to reduce the burden on their monthly budget. However, there’s nothing to say a consumer proposal cannot be offered over a shorter term, as some people prefer to pay off their consumer proposal early, to put it behind them.

You may hear claims that a consumer proposal can reduce your debt by 80%. That may be true in some cases, but not all. Someone who has no assets and low income may benefit by such a sizable reduction, however, someone who has a moderate or high income, or assets to their name, may be expected to offer to repay a larger portion of their debt.

The amount to be repaid in a consumer proposal will also be determined by the wishes of the creditors involved. Some creditors may not be too concerned with how much of the debt is being repaid, so long as the offer is better than what might be expected in a possible bankruptcy. However, some creditors may only accept a consumer proposal if they are receiving at least one third, half or two thirds of the debt regardless of how little may or may not be available through bankruptcy.

Because each person’s situation is unique, the benefit of a consumer proposal is that it can be tailored specifically to meet your needs. If you are dealing with debt, contact us today for a free consultation.

Bankruptcy happens to almost 120,000 Canadians every year. In bad times the number of bankruptcies and consumer filings increase. When the economy recovers they decline. But they never go away because bankruptcy is a viable solution when people find themselves in too much debt.

Our infographic, below, looks further at the most common fears of bankruptcy often expressed by individuals who come in to see us for a consultation:

My own carelessness caused my bankruptcy. In fact less than 4 in ten bankruptcies are caused solely due to poor financial management. Illness, job loss and relationship breakdown are much more likely to be a determining factor in filing personal bankruptcy.

Everyone will know if I file bankruptcy. Your trustee will only inform those who need to know about your bankruptcy which in most cases means only your creditors. You do not need to worry about your friends and family finding out unless you choose to tell them.

I’ll lose everything. Both Canadian and Ontario provincial law have legislated exemptions listing what you keep if you file bankruptcy and the vast majority of people do not lose anything.

Bankruptcy doesn’t get rid of all my debts. Bankruptcy does not deal with secured debts and it’s true some debts, like alimony and recent student loans are excluded, however bankruptcy does deal with most unsecured debts including credit cards, payday loans, bank loans, lines of credit and even tax debts.

Bankruptcy will ruin my credit forever. This is probably the number one fear for most people. While bankruptcy will remain on your credit report for 6-7 years, you can begin the process of rebuilding right away and the fact that you have no debts allows you to gain the fresh start you are looking for.

Find out the truth behind bankruptcy and why it helps so many people find a fresh financial start.

The reason you file a bankruptcy or consumer proposal is to eliminate your debts. While there are some exceptions (like special rules for student loans), bankruptcy eliminates most unsecured debts. After several court cases, it is now clear that 407 ETR debts are dischargeable in bankruptcy. They are a debt, just like any other debt.

But what if you haven’t declared bankruptcy or made a proposal to creditors and have unpaid bills to the 407 ETR? What collection rights does the 407 ETR have?

In order to collect on an account, the 407 has several collection remedies including:

Issuing internal notices of default and demand for payment

Engaging outside collection agencies to make phone calls and otherwise attempt to collect on an overdue 407 bill

Suing in court to obtain judgement in order to pursue a wage garnishment

Most importantly, under Section 22 of the Highway 407 Act the 407 can notify the Registrar of Motor Vehicles of the failure to pay, and the Ministry of Transportation will refuse to issue a new vehicle permit when the license plate comes up for renewal.

This “blacklisting” or “plate denial” is usually the first step that the 407 ETR will take before they serve a statement of claim and commence legal action to, for example, garnish wages. The courts have decided that since 407 ETR has this extraordinary power, they should use this power as a first step to attempt to secure payment.

This same power of plate denial also makes it impossible to ignore a 407 ETR debt and hope that it will go away over time. Let me explain.

..shall not be commenced in respect of a claim after the second anniversary of the day on which the claim was discovered.

In other words, you have two years to start legal action and then it’s too late. You can’t wait forever to sue someone. So how do you calculate two years?

For most debts, the two year limitation period clock starts on the date of the last payment, also known as the “last activity” on the account. However, in the case of the 407 ETR, there was a court case (407 ETR Concession Company v. Ira J. Day) that ruled that the two years starts on the date that the 407 ETR sends a plate denial notice. And to complicate matters even more, if you have a transponder, you signed a Transponder Lease Agreement, and the standard agreement used by the 407 ETR attempts to lengthen the applicable limitations period to 15 years. While I’m not a lawyer, I’m of the opinion this extension isn’t valid since you can’t contract out of provincial laws, so I question how much the ETR company can rely on this extension.

But the real answer is, the Limitations Act isn’t really going to help you avoid paying an overdue 407 ETR account if you want to get your plates back.

So while the Limitations Act might stop further collection actions like a wage garnishment, the debt itself isn’t going to go away.

If you only owe money to the ETR, you can work out a payment plan with them. If, however you have other debts, contact us to book a free consultation with a Licensed Insolvency Trustee to talk about your options.

It might surprise you to know just how many tools collection agents have to be able to locate you when you owe money. Today I talk with Blair Demarco-Wettlaufer, Managing Partner of Kingston Data & Credit, a collection agency servicing Canada and parts of the United States. Blair is a past guest from show #20 where we discussed how to stop collection calls.

He’s back to give me an insider’s perspective about ways that collection agents find debtors, including the use of social media to do it, and what you should do once they’ve successfully contacted you.

Collection agents use “ridiculous amounts of data”

Gone are the days when collection agents sat smoking at their desks, flipping through index cards and telephone books to find ways to contact debtors. Blair explains that today, there is no shortage of information available to the general public and debt collectors because:

there are ridiculous amounts of data available now through the internet, through databases, through information technology, and a lot of people aren’t aware of what can and can’t be used.

Now, a collection agent can search databases like the Canada Post National Change of Address Database or Canada 411; they can also pull a full credit bureau on an individual over the computer. In an age of technology where our information gets logged every time we sign up for something online, whether we provide information to create a new login, apply for a new credit card or purchase items that require our personal information to be divulged, anonymity has become a thing of the past. We make it easy for people to find us.

But what if an agent has the wrong information?

Not all data is current or accurate. However, collection agents can only go by the information that they have been given. A collection agency’s data is gathered from the original creditor’s logs, and agents will assume that the information is correct, until proven otherwise. This is why many people receive collection calls intended for someone else. If the wrong person has been reached, agents will then proceed to search for new data by following leads provided by the original creditor such as your birth date, social insurance number, drivers license number and an employer in an attempt to reach you. Once the correct information has been found, they’ll update your file with the “best known data”.

Your social media accounts are making you easy to find

There are laws that protect our privacy and they include social media. For example, collection agents are not allowed to use data that they found on a social media account because the information was not intended for collection agencies.

But that doesn’t mean that all agencies follow this rule.

If your social media accounts include contact information like a phone number or address, or if you’re uploading pictures that include your house number in the background, that information is out there for all to see.

What’s more is that databases exist that are able to pull information from social media accounts and other online sources to compile reports that provide a detailed list about you, at the click of a button. Blair points out that

not only can we go to a website like Pipl.com and pull up your Facebook, your Twitter account, your local bowling league stats, we do a search through a database called Teranet and see if you’re on the title of your house, who owns your mortgage, how much equity is in your house; there isn’t a lot of secret data anymore.

Social media is constantly changing, and so is the way that people can access your information. Although hypothetical, Blair explains that some people have suggested that a person’s credit score be determined by the longevity of their Facebook account because “it’s really hard to invent a social media identity and keep it going over years and years and years”. Although it may seem extreme, these ideas are coming ever closer to reality with things like Facebook’s recently publicized patent that would allow lenders to assess an individual’s friends on Facebook to determine their credit worthiness.

“Triggers”: your information sent straight to an agent’s inbox

I ask Blair what he means by the word “trigger” and how it can be used to find debtors. He explains that agencies can go in and pull a credit bureau scrub to receive contact information including addresses and phone numbers for thousands of files at once, within 15 minutes.

For those individuals lacking data, agencies can pay a monthly cost to activate a “trigger” function that alerts them to new data. Blair explains that

…if they suddenly surface, or they get a new address or a new phone number, we get an email alert.

What’s more is that it’s not uncommon for an account to be managed by different individuals at the agency over time. In fact an account can change hands “two to eight times over five to six years”. The trigger function allows whomever is assigned to the account at that time to locate you. So what could set off a trigger alert? Blair’s example is that of a person applying for a new credit card. On the application form, it is necessary to fill out your address and phone number, and as soon as you do, an email will be sent to your collectors who have signed up for this trigger function. So if you owe money on an old debt, then apply for new credit, chances are the collection agent will find you again and start calling.

So what can you do to reduce your data footprint?

Be mindful of the information that you’re putting out for the public to see on all of your social media accounts. This includes reviewing your privacy settings, not using your full name and not accepting friend requests from people that you don’t know. Be proactive and Google your own name to see what a basic search will provide to those looking to locate you. Check your online footprint through tools the collections agencies use like Pipl.com. Consider who might see your information when filling out applications or creating new accounts.

And last but not least, if you’re tired of trying to hide from collection calls, it might be time to consider filing a consumer proposal or personal bankruptcy to receive creditor protection. Once you file, a “stay of proceedings” is put in place that stops collection calls, reducing your stress so that you can focus on becoming debt free.

Listen to the full show or read the transcript below for more information about:

FULL TRANSCRIPT show #57 with Blair Demarco-Wettlaufer

Have you ever wondered how a bill collector was able to find you? I’ve had hundreds of people over the years come into my office and say yeah I had this cell phone bill from five years ago, and I hadn’t heard from the in five years and then all of a sudden they started calling me. I moved, so I live in a different town and I’m at a new job and I have a new phone number so I have no idea how they tracked me down. Well, that is an interesting question. How does a collection agent find you? That’s the question we’re going to answer today on Debt Free in 30 and I know just the guy who has the answer. So, let’s get started. Who are you and what do you do?

Blair Demarco-Wettlaufer: My name is Blair Demarco-Wettlaufer, I’m the managing partner of Kingston Data and Credit, which is a collection agency across Canada and parts of the U.S.

Doug Hoyes: Well, great thanks for being here today Blair. In fact thanks for being back on the show. You were my guest all the way back on show number 20 and this is show number 57. So, that was about nine months ago that you were on the show. You gave us some great advice on that show on how to deal with collection calls. So, I’ll put a link in the show notes at hoyes.com to that show.

So, let’s get back to the question. How did they find me? So, what’s the answer? You run a collection agency so you’re the guy who is out there tracking people down, that’s your job. How do you do it? How do collection agents do it?

Blair Demarco-Wettlaufer: Well, I guess a lot of people wouldn’t see what happens internally. But one thing to understand is collection agencies aren’t what they used to be. When I first got into the business there were a bunch of people smoking at their desks working off index cards. Obviously, there is ridiculous amount of data available now through the internet, through data bases, through information technology and a lot of people aren’t aware of what can and can’t be used. I just received a batch of 15,000 collection accounts. And we were able to contact one of the credit bureaus and say give us their up to date address and phone number and within 15 minutes we had 6,000 phone numbers returned to us.

Doug Hoyes: So, let me just stop you there. So, 15,000 – a list of 15,000 people to collect from, and in a very short period of time you had updated phone numbers for a big chunk of them.

Blair Demarco-Wettlaufer: That’s right.

Doug Hoyes: And in the old days, you would have literally gone to your old stack of phone books from across the country and tried to look them up. And of course you couldn’t find them cause they’re all old phone books.

Blair Demarco-Wettlaufer: We actually had a guy drive across Canada picking up phone books at Bell Centres, you’re not wrong and going to the library to use the Vernon’s Directory to reverse look up phone numbers.

Doug Hoyes: So, is this 1920? How old are you?

Blair Demarco-Wettlaufer: [laughter] That was in the 90’s.

Doug Hoyes: In the 90’s, wow.

Blair Demarco-Wettlaufer: And now I can do a search through the Canada Post National Change of Address Database from my office. Or I can pull a full credit bureau on somebody over a computer rather than a fax request. Things have changed so much in the last 20 years and also people aren’t – often people aren’t aware of what kind of a data trail they’re leaving. I’d advise all your readers, Google yourself, see what’s out there, see what’s on the internet. Cause there’s a ridiculous amount of data.

Doug Hoyes: So, let’s talk about that, a ridiculous amount of data. So, if we were to do a search for me or you or somebody else you’re collecting from – let’s go through the process with this 15,000 list of names then.

Blair Demarco-Wettlaufer: Okay, so we receive accounts in collections. And those accounts could be 30 days old; they could be five years old. So, the data could be good or it could be bad. So, it’s really based on what the original creditor did and we – we’re not psychic – we only know what we know. So, we’re going to assume a phone number on file is good until proven otherwise. That’s why I’m sure you get a lot of your listeners calling in going, this agency’s calling the wrong number. Well, we don’t know it’s the wrong number.

Doug Hoyes: Cause that was the phone number of the guy five years ago. You’ve now got the phone number, they don’t know any better.

Blair Demarco-Wettlaufer: Exactly. And, you know, obviously if we’re calling there might be five or six other collection agencies calling that same number for a debtor who no longer has that phone. But let’s assume we have data and it’s good. Obviously, picking up the phone or calling or emailing or texting is right available. Let’s assume the data’s bad. We’ll go to whatever data the creditor had. For example, some creditors ask you for personal references; we may have that. They’ll ask for an address, they’ll ask for a social insurance number, a date of birth, a driver’s license number, an employer. We’ll have a certain amount of data that we start with and it’s our responsibility to reach the right person if possible.

Doug Hoyes: Well, cause if you reach the wrong person you’re not going to collect money, you’re not going to collect any money on it. So, you’ve got this list of 15,000 names. So, the first thing you did was run it through the credit bureau?

Blair Demarco-Wettlaufer: Yes, we ran it through Equifax.

Doug Hoyes: And you can do that very quickly.

Blair Demarco-Wettlaufer: Yeah.

Doug Hoyes: And because you’re linked in with Equifax this is not a huge expense to you I assume. It didn’t cost you a million dollars to do all these searches.

Blair Demarco-Wettlaufer: Certainly less than paying somebody to look through the phone book one at a time.

Doug Hoyes: Got you, and it all comes back to you electronically.

Blair Demarco-Wettlaufer: That’s right.

Doug Hoyes: And it’s all in your computer now.

Blair Demarco-Wettlaufer: And we update the consumer’s file with the best known data. And so, a collector sitting in our office will see Bob Smith owes $800. And it’ll say we pulled the person’s Equifax and here’s their phone number, it was good as of February 2015, here’s the last known address, it was good as of April 2015. And the credit bureau gets their data from the other creditors.

So, if you have a cell phone and you make your payment once a month, every month not only is your cell phone company reporting to the credit bureau Bob made his payment on time, they’re also saying and he still lives at this address and this is still his phone number, and so on. So, the credit bureau is this huge flux of data coming from creditors, likewise, when I take my 15,000 consumer’s list in our office and I ask the credit bureau for data, they take my data, my last known address and phone number and append it into their database and they try to determine whether my number is better than the one they have on file, if my address is better than the one they have on file. If a consumer goes to Trans Union or Equifax, they can actually request a list of who’s reporting and who’s inquiring. And for the most part, they can see all that data.

Doug Hoyes: So, if you’re collecting from Bob Smith, and Bob if you’re listening sorry that we’re using you as an example here, but you’re collecting from Bob Smith and let’s say the address and the phone number that was in Equifax was old, but you were able to do a Google search, find the guy, so you put that information into your system, is that then also going back to Equifax at some point?

Blair Demarco-Wettlaufer: Maybe.

Doug Hoyes: Maybe.

Blair Demarco-Wettlaufer: If we’re trying to reach Bob, poor Bob. And Bob takes care of his account and we’ve had his account 30, 60, 90 days, he’s co-operated with us, there’s been no issue, we have no need to report his debt to his bureau. That’s the bad news, that’s the consequence. If we reach Bob and say, Bob, would you like to pay this or would you like us to list it on your credit bureau and Bob pays it, we don’t want to affect him negatively.

But let’s say we can’t find Bob, or Bob tell us, go to hell in a hand basket. Yes. We’re going to report that debt to the bureau and yes his updated information that we’ve accumulated will be reported to the bureau. And it’s not that we’re trying to do something to Bob individually. For example, our agency updates the credit bureaus in Canada and the U.S twice a month and we’re uploading hundreds of thousands of people at a push of a button.

Doug Hoyes: And that’s what big data is, it’s very quick and very fast.

Blair Demarco-Wettlaufer: Yeah.

Doug Hoyes: So, I want to get back to this whole idea of what gets on the credit bureau. But before we do that then, you’ve got this new list of creditors, you go through Equifax and dump out the most recent information.

Blair Demarco-Wettlaufer: Exactly

Doug Hoyes: And then I would assume if I was doing this I would have a list now and I would on my computer sort it for all the people that have the most current information and those are the people I would start calling.

Blair Demarco-Wettlaufer: Exactly.

Doug Hoyes: And the people I don’t have any information for are at the bottom of my list and I’ll get to them when I get to them, or never.

Blair Demarco-Wettlaufer: Well, it depends on the agency. Like some agencies use predictive diallers. So, they’ll take all 6,000 and call them in the first hour and just hammer them and call them three or four times a day. Not necessarily the best approach in my opinion, but that’s how a lot of old school, hardnosed collection agencies work. I would rather have someone manually call and verify it’s correct and speak to them person-to-person but I’m crazy according to the competitors.

Doug Hoyes: Yeah, that’s not the way a lot of them do it. So, okay so you’ve picked the low hanging fruit, you’ve got the obvious data from Equifax, but there’s still a bunch of people that didn’t show up there.

Blair Demarco-Wettlaufer: Sure.

Doug Hoyes: What other things are you going to do then?

Blair Demarco-Wettlaufer: Well, depending what province they’re in, like in Ontario it’s required that we mail a letter. We say we got a new address, but not a new phone number; we’ll mail a letter to reach them. If we can’t find them through Equifax we’ll try through Trans Union. If we don’t find them through Trans Union, we’ll look on the Canada Post Change of Address Database. If that doesn’t work, yeah we’ll literally roll up our sleeves and log into Canada 411 and see if the person shows up. Or we’ll do a Google search and see what’s there, cautiously.

There’s a lot of hullabaloo right now about social media and what data’s allowed to be used and what’s not allowed to be used. I was at a conference last year and one of the people from the office of the Privacy Commissioner came and told all the collection agencies in the room, if you look at Bob’s Facebook and Bob has his phone number on there, technically Bob did not intend that for you, you’re not allowed to use it. But certainly there are agencies out there that might.

Doug Hoyes: So and that obviously raises an interesting question about social media. You said earlier that we all leave quite a footprint.

Blair Demarco-Wettlaufer: Absolutely, some more than others.

Doug Hoyes: And so if I’m on Facebook, and I’m actually not on Facebook, I have an account but I don’t know how to log into it and every time I log into I’ve got 9,000 friend requests. So, I don’t know what I’m supposed to do with that, so I’m not the expert on that. So, I’m on Facebook and I have a picture of me playing baseball, throwing the ball with my son on my front yard. And so if you could look at that picture you can see where I live cause there’s the number on the side of my house.

Blair Demarco-Wettlaufer: Absolutely.

Doug Hoyes: And so whether that’s legal or not for a collection agent or anyone else to use that information, cause what you just said was I didn’t intend for that information to be used for collections, the fact of the matter is, it’s there.

Blair Demarco-Wettlaufer: Exactly. And some agencies would use that data. It’s not just that. Let’s say, Doug, you have an account in my office and we’re trying to locate you and you’ve been less than co-operative. And you owe $12,000 for a car lease. Not only can we go to a website like pipl.com and pull up your Facebook, your twitter account, your local bowling league stats, we can do a search through a database called Teranet and see if you’re own title on your house, who owns your mortgage, how much equity’s in your house there isn’t a lot of secret data anymore.

Back in the old days you’d have unpublished phone numbers and obviously cell phone numbers are not tracked by traditional phone directories, that data’s available through the credit bureau; that data’s available through social medial; that data’s available through a number of internal databases. And the thing that I think people don’t realize is that when a collection agency is making an attempt to call, they’re not trying to do so maliciously, they’re just trying to reach a person to make them aware, should you pay the debt or should it be listed on the bureau or in certain cases should it go legal. And we’re entirely pointed towards reaching people, that’s our job. We’re outward facing, trying to reach thousands of people a day and sometimes we’ll get answering machines, sometimes we’ll reach people, sometimes we’ll exchange emails with a consumer, but we’re geared towards doing that on a massive scale. It would be in our best interest to reach people efficiently, politely, professionally and within the law, that’s ultimately our goal.

Doug Hoyes: And deal with it.

Blair Demarco-Wettlaufer: Yeah.

Doug Hoyes: Now you mentioned pipl.com and I’ll put a link to this in the show notes, but pipl is pipl.com.

Blair Demarco-Wettlaufer: Yeah.

Doug Hoyes: And from what I understand it is really a database of databases.

Blair Demarco-Wettlaufer: Exactly, and it’s publically available. So, it’s not going to have necessarily the highest quality of data. One of the things you and I talked about earlier, there’s a website in the U.S called Spokeo. And Spokeo.com is a paid database. You can’t access a lot of it for free. But if you go into that, you can look up people in the U.S and it gathers census data, social media data, Google street view data and literally you can type in John Harrison. John Harrison lives in Michigan, you pull up all the John Harrison’s in Michigan, you pick the one in Dearborn, you click on it, and it shows you a Google street view of his house, the average market value of the houses in that area. Is he a democrat or a republican, the names of his relatives, a link to this Facebook account, his email address, his phone number, his date of birth, his spouse’s name, that’s the kind of data that’s available.

And people aren’t realizing when they answer a census or they buy something on Amazon.com they may be releasing that data for the purposes of – they may have agreed – when they buy something on amazon.com in the fine print it might say they have the right to resell your data. And amazon.com might, hypothetically, I don’t know if they do or not, may have a revenue stream from selling that data to another database and that’s how this data gets around.

Doug Hoyes: And you’re just using them as an example, but literally you do anything with, potentially can be forwarding that data somewhere else.

Blair Demarco-Wettlaufer: Absolutely. So, if you get a cell phone with Virgin mobile, I guarantee you, you have signed off giving them the authorization to pull your credit data and to report to the credit bureau. And that’s all entitled under the Consumer Reporting Act of Ontario, in Ontario for example.