Family law and bankruptcy law frequently overlap and the effect can be quite complicated. Our Bankruptcy and Divorce Canada fact sheet will answer some key questions you may have however it is always important that you talk to your bankruptcy trustee about your specific situation.

How Does Bankruptcy Affect Alimony & Maintenance or Support

Bankruptcy does not discharge outstanding alimony or child support payments in Canada pursuant to section 178 (1)(b) the Bankruptcy & Insolvency Act.

The spouse owed back support payments can make a claim in the bankruptcy and receive their share of any ‘dividend’ paid from the estate. Any alimony or support arrears for the 12 months prior to the date of bankruptcy are considered a preferred claim and are paid out of the proceeds of the bankrupt estate before any other unsecured claims. The balance left unpaid is still owed by the paying spouse.

Unpaid debts due to equalizaton payments under the terms of a divorce or separation agreement are treated like any other unsecured debt and are eliminated by filing bankruptcy.

Do Support or Alimony Payments Affect Surplus Income?

Support and alimony payments are deductible for purposes of calculating surplus income. This potentially lowers your net income, reducing any surplus income payment you may be required to make in a bankruptcy.

Filing for Bankruptcy During Divorce

Whether you file bankruptcy before or after your divorce is finalized affects whether your creditors will be entitled to any assets that may be part of our divorce agreement.

If you file bankruptcy before your divorce is final, your assets transfer to your bankruptcy estate and are no longer available for distribution in a divorce.

Alternately, if you finalize your divorce before bankruptcy and assets are transferred to an ex-spouse as part of a Family Court Order or legal separation agreement before you file for bankruptcy (assuming not done fraudulently) then these assets are no longer available for your creditors in the bankruptcy.

What Happens To Joint Debts After Bankruptcy?

A joint debt cannot be eliminated by a divorce or separation agreement. That means that, no matter what your divorce or separation agreement says, debts that were owed by both you and your spouse before the divorce, will still be considered joint debts after the divorce. If one spouse files bankruptcy, the creditors can, and will, pursue the ex-spouse for payment of a joint debt regardless of what you agreed to in the divorce.

To eliminate a joint debt, your lender must agree to remove one spouse from any debt they co-signed or guaranteed. This includes joint credit cards.

How To Deal With Debt Problems In A Divorce Situation

A divorced or separated couple can still file a joint bankruptcy or joint consumer proposal to eliminate combined debts. This is not uncommon as a method of dealing with joint debts owed by a couple who can no longer repay these debts due to their divorce and a change in their financial circumstances.

Whether a bankruptcy or consumer proposal makes sense for you, or your ex-spouse requires an assessment of each of your individual financial obligations.

The holidays are known for being a time of happiness and joy. But for those struggling with depression, anxiety or loss, the holidays can be a difficult. I’m joined today by Theresa Karn, Manager of Clinical Services at Carizon Family & Community Services in Kitchener, Ontario.

Attempting to create the perfect holiday experience and living up to expectations set by yourself and others can lead to stress, sadness and even depression. Theresa explains that

we’re saturated with images through televisions and magazines…of perfect couples and perfect families having their perfect holidays. And we all look at that and think, my family isn’t like that. And people who are otherwise fairly satisfied with their lives and content, can end up being really dissatisfied over the holidays measuring themselves against all of these images that are not real to start with.

With the holiday season fast approaching, it’s important to understand what depression is, how to recognize its symptoms and how the holidays can make this struggle even more difficult.

What Is Depression?

To be able to recognize depression and treat it properly, it’s important to understand what the term means. Theresa explains that

depression is not the blues; it’s not feeling down…It’s an extreme and pervasive sadness and a sense of helplessness and hopelessness.

She points out that these feelings will last for some time and that if it lasts for longer than three weeks, it has become pervasive.

The cause for depression is a chemical imbalance and can be triggered by a number of things including:

The loss of a loved one;

Trauma;

Genetics;

Hormones;

Health problems;

Seasonal Affective Disorder (SAD); and

Illness.

Symptoms Of Depression

Recognizing the symptoms of depression is important for seeking help or helping a family member or friend. Symptoms range from emotional to physical and can include:

Long lasting sadness;

Increased anger;

Difficulty focusing and making decisions;

Negative self-image;

Fatigue and low energy;

Lack of enjoyment in activities you used to enjoy;

Change in sleep patterns (insomnia or too much sleep);

Developing a dark and cynical sense of humour

Withdrawing from family and friends;

Physical aches and pains;

Extreme irritability;

Increased substance abuse;

Fixation on the past and on what has gone wrong; and sadly

Thoughts of death and suicide

Similar to the stigma about filing bankruptcy or having debt problems, there is also a stigma associated with depression. But like financial difficulty, Theresa points out that the impact of depression is common and far reaching,

worldwide, 120 million people suffer from depression in any given year. And the stats say 1 in 10 will suffer from depression in their lifetime.

Why Is Depression & Anxiety Common Over The Holidays?

Although the holidays are supposed to be a time of joy, it can also be a constant reminder about their unhappiness for those struggling with depression. Theresa tells me that she works with a lot of clients who are having financial difficulties, single parents and newly divorced couples who feel like they can’t provide for their families and give their children what they want. She explains that

there is a higher level of depression and anxiety in December and around the holiday season because there’s so much pressure, there’s time constraints and financial constraints, there’s lots to do for people trying to prepare for the holidays. The commercialization really has increased that pressure I think, for people to overspend.

The holidays can also act as a reminder about the loss of a loved one when

the holiday comes around and there’s that empty chair at the table. You’re trying to recreate the traditions that you’ve always done with those included and all it does is bring up that pain that that person isn’t there.

If you or someone you know is feeling depressed or anxious, it’s important that you seek help. Reach out to family, friends or a counsellor like Theresa. If the holidays cause anxiety because of financial responsibilities or expectations, talk to a professional, like a bankruptcy trustee or credit counsellor who can help you come up with a plan.

Listen to the full podcast for more about:

Creating new holiday traditions;

How to deal with grief; and

Why you should start planning for the holidays early.

It’s the holiday season, a time of happiness of joy, but it can also be a time of stress, anxiety and even depression. We all know the stress of finding the perfect gift and planning the perfect meal and when you combine that with cold weather and less sunshine our anxiety levels often increase at this time of year.

But when does normal holiday stress turn into serious anxiety and depression? That’s what we’re going to discuss today with my guest. So, let’s get started, who are you? Where do you work and what do you do?

Theresa Karn: Hi Doug, I’m Theresa Karn. I’m from Carizon Family & Community Services in Kitchener. And I’m the Manager of Clinical Services, so I oversee 23 counsellors and all of the counselling programs for the individual couple, family counselling at Carizon.

Doug Hoyes: Great, well thanks for being here today, Theresa. So, our listeners are familiar with Carizon because we’ve had Heather Cudmore, who’s the Manager of the Credit Counselling group on the show and in fact she’s going to be on again this month. Tell us other than the credit counselling piece, which we’re obviously very familiar with, what other services does Carizon offer?

Theresa Karn: So, Carizon has a wide range of services from specialized children’s mental health services, education and school based services and community services. So, we offer services for children, adults, families and groups.

Doug Hoyes: So, it’s a very wide ranging, all encompassing services that you offer. So, today I want to narrow in on the area of depression. So, before we get into it, let’s start with some definitions. What exactly is depression? Cause I think people are listening to this and thinking, oh, well yeah, I’m having a bad day and I’m kind of depressed. Well, we all have bad days when the weather is lousy and it’s snowing and your car won’t start. That’s not depression, I assume. Tell me what is.

Theresa Karn: Yeah, definitely. I think depression is a word that’s become over used. And depression is not the blues, it’s not feeling down. It’s not what you’re talking about; it’s an extreme and pervasive sadness and a sense of helplessness and hopelessness. So, how would you know the difference between the blues and depression? I think it’s a matter of length of time, for one thing. If it lasts for more than three weeks I would say, and as I said it’s persuasive; it doesn’t just happen when you have a disturbing interaction or something happens to disappoint you, but it lasts and it lasts.

Doug Hoyes: It lasts and it lasts with you for an extended period of time.

Theresa Karn: Yes.

Doug Hoyes: So, what causes that? Obviously, it’s not the bad weather, I assume, or is it? What are the cause of depression?

Theresa Karn: Well, you know that’s an interesting point because bad weather can contribute. There is something called SAD, Seasonal Affective Disorder. And for some people the lack of sunshine can cause depression. But that’s not everybody. It is actually a chemical imbalance in the brain. And it could be triggered by a loss or a trauma, it could also be part of our genetic makeup that we are prone to depression, it could be caused by hormones such as postpartum depression or even health problems, some health problems have depression as a kind of a symptom.

Doug Hoyes: So, there are many different causes. What then are the symptoms? So, you kind of hit on some of them, but walk me through, if I sitting here listening to this today going, yeah I wonder if – I’ve always through well maybe I’m just having a bad day. But now that you mention it maybe it’s a little more serious than that, or maybe I know someone, a friend, a family member, a co-worker what are the symptoms that I should be on the lookout for that would alert me to the potential that that person or myself is suffering from depression?

Theresa Karn: Symptoms would be long lasting sadness, increased anger and we find that for men especially, you may see more anger than sadness because I think for men expressing and admitting to sadness is harder just with the way men are raised.

Doug Hoyes: And when you say anger, are you talking about like flying off the handle, that kind of anger?

Theresa Karn: It could be extreme irritability and just a sense of simmering all the time. Maybe you might notice road rage more often and just feeling like there’s no level of just coping with people and with line ups and with just some of the usual irritations that we go through.

Doug Hoyes: Really ticked off, so that’s interesting. So, the long lasting sadness, but what I would consider a completely different thing, anger, those are both potentially symptoms of depression. What other symptoms are there?

Theresa Karn: Also a difficulty focusing and making decisions, negative self image, you know if you’re constantly telling yourself that you’re a loser, you’re not worth anything, you’re not as good as other people, fatigue and low energy is also a symptom. A lack of enjoyment of activities that you would usually enjoy, so if you notice that there are things that you used to love doing, maybe sports or hobbies or different activities or sexual activities and then suddenly you have no interest anymore.

Doug Hoyes: So, a change, something that used to bring you pleasure, now doesn’t. Something has change, what’s the issue there, okay.

Theresa Karn: Yes. There could be a change in sleep patterns. And it could be two extremes, it could be insomnia or it could be wanting to sleep all the time. A change in eating patterns so you may find that you’re gaining weight or losing weight because of that. Developing a dark and cynical sense of humour, so maybe you or people around you have noticed that your sense of humour has really changed; maybe to the point where it’s making people uncomfortable. Withdrawing from family and friends, just wanting to be alone, isolating yourself, maybe it just feels like too much trouble to be around people. And even physical aches and pains, often people aren’t aware that there are physical symptoms to depression.

Doug Hoyes: So, what would be an example of that, like literally, like when you’ve got the flu and you ache all over, that kind of thing? Or would it be something more specific than that?

Theresa Karn: Yeah, kind of like that, but maybe a little more subtle, but you may have more headaches and just feel achy and not well. And obviously when you are distressed other psychosomatic things will be happening like stomach aches and headaches, that sort of thing because our body does react. Increased substance abuse could be happening because I think people will try to self medicate and, you know, maybe I’ll feel better if I have a drink or if I use this drug.

Doug Hoyes: So, you’re trying to mask the symptoms or treat the symptoms. You don’t realize that’s what you’re doing but – so, you’d be talking about, you know, lots of alcohol consumption and lots of other types of drugs to mask it.

Theresa Karn: Yeah and the difficulty with that is you may feel better in the short run, but alcohol is actually a depressant as well. So, it will make things worse in the long run internally but also with relationships. A fixation on the past and what has gone wrong. So, you may find that you’re really thinking a lot about I failed here, I failed there, I messed this up, and really not looking at anything that was positive but really focusing on the negative.

Doug Hoyes: When you go through that list, a lot of things are internal, then.

Theresa Karn: Uh huh.

Doug Hoyes: And that’s really what we’re talking about here. You can be depressed regardless of what’s going on around you.

Theresa Karn: Absolutely. And it’s the opposite of rose coloured glasses. You see the negative, you see what’s wrong, you’re not noticing what’s good anymore. And the last one which is the most serious and concerning is thoughts of death and suicide. Depression can be – can lead to death and that’s the frightening reality of it, that’s it’s not something to ignore.

Doug Hoyes: So, there are many different levels, then. It’s not a one or a zero, an A and a B. There are people with increasing levels of severity of it. So, how common is this? Is depression very rare? Is it very common? Give me a sense of the scope of the problem here.

Theresa Karn: Depression is much more common than people realize. Worldwide, 120 million people suffer from depression in any given year. And the stats say one in 10 still suffer depression at some point in their lifetime. The stats also say that women have roughly twice the rate of depression of men. But I would question if that stat reflects the fact that women feel a little more comfortable to go and ask for help. So, their rates are recorded, whereas for men, it’s tough overall I think to ask for help and say I’m not doing well and to admit or even recognize it as depression if it’s not as much crying as it is anger.

Doug Hoyes: Right, which is what you alluded to earlier when we were talking about the symptoms, so, I assume then that there is still a stigma attached to this.

Theresa Karn: There is, absolutely, and it is decreasing thankfully. But I think over the years historically there’s been a lot of anger and fear about depression and the belief that depression was about weakness and, you know, even in some instances that mental illness was about demon possession and things like that. So, there has been huge stigma and it is coming down, but it holds people back because some of us have absorbed those beliefs about depression, so it’s tough to admit that’s how I’m feeling.

Doug Hoyes: So, it’s unlikely you’re demon possessed is what we’re saying here.

Theresa Karn: Exactly.

Doug Hoyes: When you talk about this, I’m thinking you know, what you’re saying is very similar to what I see in my world, dealing with people with serious debt problems. You said that one in ten people are going to suffer from depression at some point in their lives. Well, that’s very close to the stat of the number of people who end up having to file a bankruptcy or consumer proposal. I don’t think they’re the same people, but it’s obviously the same percentage of the population.

And there is certainly a stigma associated with debt problems as well. And I think the stigma is because it’s one in one people who suffered from these things. If it was nine of ten there would be no stigma ’cause we would all suffer from it. There’s no stigma attached to getting a cold. We all get that, we get one a year, it’s not a big deal. But because this is something that affects a smaller component of the population there’s still a stigma associated with it.

Now we’re in the holiday season, am I correct in assuming as I said in the introduction that depression and anxiety are more pronounced at this time of year?

Theresa Karn: Absolutely. I noticed in your introduction that you talked about the time of joy, and wow, if you’re feeling depressed what a weight that is to feel like you’re expected to be joyful in December. So, there is a higher level of depression and anxiety in December and around the holiday season because there’s so much pressure, there’s time constraints and financial constraints, there’s a lot to do for people trying to prepare for the holidays. And the commercialization really has increased that pressure I think for people to overspend. I have grandchildren and already the ads have started on TV. This is the toy that every kid needs under the tree, right?

Doug Hoyes: Yeah the ads start in September or they start in the summer and they just go continually. I mean when I think of Christmas, the holiday season, I think of the Normal Rockwell paintings of everyone sitting by the Christmas tree and tobogganing the fresh snow covered hills and things like that. But that’s not really an accurate picture for a lot of people.

Theresa Karn: It’s not, and you know, it’s interesting. A couple of years ago I read an article about Normal Rockwell in a magazine and the article said that Normal Rockwell grew up as an only child of a single mom and if you can imagine back in the 40’s and 50’s the stigma even around that, the whole single parent thing was not accepted. The father left the home and abandoned Norman Rockwell.

So, he was a child who grew up with a lot of loneliness, a lot of isolation and probably rejection I would think from other kids. And went on then to be this amazing artist and paint these amazing pictures of the absolute ideal holidays with the big extended family, everybody’s happy and wholesome looking. And I think a lot of us, then, have looked at those pictures and thought that’s what it should look like. That’s what my family should look like at the holidays and that’s the level of joy and connection that we should have. And who measures up to that?

Doug Hoyes: Yeah, nobody. And so what you’re saying then is even those pictures that he’s painting were what he was striving for, but certainly not what he had.

Theresa Karn: Absolutely. And the article went on to say that he suffered depression a lot through his life, he struggled. So, yeah it’s definitely an ideal and we see that all over the place. We’re saturated with images through televisions and magazines and wherever of perfect couples and perfect families having their perfect holidays. And we all look at that and think my family isn’t like that. And people who are otherwise fairly satisfied with their lives, and content, can end up being really dissatisfied over the holidays measuring themselves against all of these images that are not real to start with.

Doug Hoyes: And so what is the implication of that during the holiday season. I mean I assume it’s a big stresser. Are people then reaching out to organizations like yours? Are they going to the emergency room more? What do we see at this time of the year?

Theresa Karn: It’s a really interesting time in the counselling world because as we get towards the holidays we see a lot of distress. I’ve worked with a lot of clients who are poor or single parents, newly divorced, and the distress over I want to be able to give my kids what they want – and what the kids are asking for are more and more expensive all the electronics – and just the distress of feeling a sense of failure that they’re not able to do that.

As we get over the holidays things actually slow down. And that’s something that I saw in the stats as well. There is a belief that suicide rates are high during the holidays and that’s actually not true. Suicide rates actually go down during the holidays. But what they do see in emergency rooms and what we do see more and more is increased anxiety, increased depression and then right after the holidays, suicide rates jump 40%.

Doug Hoyes: Wow, wow. So, that’s when the real danger time is. So, I look forward to the holidays, I get through the holidays and now boom there’s nothing there.

And I mean what you said about the parents, the grandparents trying to give their children the idealized Christmas, that’s often what leads to the debt problems we see in January, February, March, April. And our phones don’t start ringing right away in January, but as the credit card bills come in, you start seeing that February, March and as a result March, April May are very busy months for us. And I think they’re all interrelated; that spending money becomes a supposed cure for depression, but obvious isn’t. Again, it’s like the alcohol and the drugs that you talked about earlier, they’re masking the problem.

So, I would assume the holidays are also a very difficult time if – we alluded to the issue of change. If I’ve lost a spouse during the year, then the holidays become a very difficult time because something significant has changed

Theresa Karn: Holidays are a huge painful trigger when someone is going through grief and loss. And it could be loss of a spouse, a family member, a child or it could be a divorce or separation or a break-up of a relationship. So, then the holiday comes around and there’s that empty chair at the table. You’re trying to recreate the traditions that you’ve always done with those people included and all it does is bring up that pain that that person isn’t there.

Doug Hoyes: We’re going to talk a bit more about what to do, but why don’t we start with that specific example you given, then. So, this person that has been there for my last 20 Christmases, who we used to go tobogganing or watch our favourite movie or whatever is no longer there, what should I be focusing on this holiday season, then?

Theresa Karn: There are things you can do to diminish that, but I think it’s really important to realize you are going to have the highs and the lows during the holidays and to expect that, that the holidays will trigger grief and realize as it comes up, yeah this is normal this is not something to feel ashamed of or disappointed in myself about.

The other things that you can do is you can do something different, come up with new traditions, maybe take a holiday over the holiday season away from home or do something outdoors, do an activity, volunteer. There’s always space for people to volunteer at food banks and places serving people over the holidays who don’t have a home and a holiday meal to go to.

Doug Hoyes: So, by starting some new traditions you lessen the impact of some of the prior ones. We’re going to talk a bit more about the specifics then of what you can do then to help deal with depression in our Let’s Get Started segment, before we do we’re going to take a quick break and we’ll be right back here on Debt Free in 30.

Let’s get Started Segment

Doug Hoyes: It’s time for the Let’s Get Started segment here on Debt Free in 30. My guest today is Theresa Karn, who is the Manager of Clinical Services at Carizon, a large counselling organization in Kitchener, that’s where their head offices is. We’ve been talking about depression, anxiety and in particular how it relates to the holiday season that we’re in now.

I mentioned before the break that financial problems often go hand in hand. And I’ve been to your facility in Kitchener, I know that the credit counselling group, lead by Heather Cudmore and her team, is very close to everybody else in the organization. I assume there are lots of times where you’re each walking someone down the hall because sometimes the debt problems make the depression issues worse and sometimes it’s the other way around. Do you find they do go hand in hand?

Theresa Karn: Absolutely, they do. I’ve dealt with a lot of clients who have been suffering from depression and they’ll talk about their overwhelming debt load and not knowing what to do. Creditors are calling. And it’s great to be able to just walk them down the hall to Heather and to credit counselling and then we can deal with both things at the same time.

Doug Hoyes: Yeah, because you have to treat the cause, not just the symptom.

Theresa Karn: Absolutely.

Doug Hoyes: And so, if as you talked about before the break I’m trying to make Christmas better for my young kids and as a result I rack up a huge amount of debt, Heather can help you deal with the debt, but if you just get back into debt again next holiday season, we kind of haven’t addressed the real problem. So, you’ve got to deal with it.

When someone comes to me with debt problems I always say well the number one thing is you’ve got to get help. I assume the advice is the same when it comes to your field, depression, anxiety and so on?

Theresa Karn: Yeah, it’s really important to get help and not to wait too long. Because when you get to the point of severe depression, you can get to a place where you just can’t make decisions and you can’t take those steps, it feels overwhelming. So, if you are feeling like the symptom list that I mentioned fits you, get help before it gets too deep. It’s easier to treat depression if you start treating it when it’s mild to moderate. If you wait till it’s severe, it’s really hard.

Doug Hoyes: It becomes much more difficult. So, in the show notes I’m going to put a link to your organization, Carizon, you can obviously look it up on the internet, Carizon, sort of like horizon is how I always think about it.

So, in our remaining time let’s talk practically then about what can I do? If I am suffering from depression or if someone I know is, obviously the first step is getting help from a knowledgeable professional. What are some other pieces of advice, practical things you would tell people?

Theresa Karn: Sure. There are lots of things that you can do and I think part of it is planning. As I said, plan that there will be highs and there will be lows in the holiday seasons and have back-up plans so that if you are overwhelmed by grief or depression and you can’t handle something that’s going on, you know what your plan is and how you’re going to make your escape. Don’t let anybody tell you that you shouldn’t feel what you’re feeling. This is the season of joy, what’s wrong with you, any of that kind of thing or you should be over it now. There are no shoulds, feelings are feeling and grief is grief. And it takes as long as it takes. So, don’t feel shame over that.

Doug Hoyes: Everyone’s different.

Theresa Karn: Absolutely, everyone is different. Also be aware that if you are going through grief or you are going through depression, it’s very normal to struggle through the holiday season. So, be aware of it, plan for it and don’t feel ashamed of that.

Doug Hoyes: So it’s almost like I’ve got to have my escape route. If I’m at a holiday event and I’m just not feeling with it, then I shouldn’t feel bad about moving on. Is that what you’re saying?

Theresa Karn: Exactly. It’s not about disappointing the host or disappointing your family, if they’re aware that you are struggling with depression they should understand that maybe you can’t handle a four, five hour party. Maybe being there for half an hour and making an appearance and going is good enough. And it’s okay to say I just can’t handle this right now. Or if it’s a situation like maybe a workplace event and you don’t want to talk about depression there, you could just tell people you’re not feeling well and head out.

Doug Hoyes: Yeah, don’t feel pressure on that. We talked earlier about creating new traditions, particularly when you’re dealing with the loss of a loved one or something. But I assume it’s also important to stick to some kind of routine as well. Sleeping in till 3 o’clock in the afternoon is probably not a good strategy, either. Is there a balancing act there?

Theresa Karn: Absolutely. It’s important to have regular self-care and try to have as much of a normal routine as you can. And that’s an area where I think most people get messed up over the holidays; being up too late, eating the wrong things, not exercising. So, it’s important to try to get to bed at a decent and regular time and have a good night’s sleep, but not sleep hours and hours because you don’t feel like getting up because that just deepens depression as well.

Doug Hoyes: Those are some great pieces of advice and obviously we could talk for a long time about the ways to treat this. Again, I’m going to put lots of notes in the show notes over at hoyes.com with the links to Carizon. Theresa, thanks for being with me.

Theresa Karn: Thank you.

Doug Hoyes: Thank you. We’ll be back to wrap it up. That was the Let’s Get Started segment here on Debt Free in 30.

Doug Hoyes: Welcome back. It’s time for the 30 second recap of what we discussed today. On today’s show Theresa Karn explained that depression is not just the blues or feeling down. Depression is an extreme and pervasive sadness that lasts for more than a few weeks and can be caused by many factors including underlying health problems and illness. She explained the symptoms and gave us many practical strategies for dealing with depression. That’s the 30 recap of what we discussed today.

So, what’s my take on what Theresa had to say? I’m not an expert on depression so I learned a lot from Theresa on today’s show. Depression is a serious problem, affecting one in ten people at some point in their lives, so it’s important that we learn to recognize the symptoms. Long lasting sadness, fatigue and low energy are symptoms but so is increased anger and extreme irritability. Every person is unique, so symptoms can differ. Depression and anxiety increase during the holiday season as we’re saturated with media images of the perfect family.

And I thought it was quite interesting that Theresa said that Norman Rockwell who painted many images of the perfect holiday season was also someone who suffered from depression. So, what can you do? Don’t let anyone tell you how you should or shouldn’t feel. Don’t feel ashamed; it’s normal to struggle with depression and grief. Keep regular eating and sleeping routines, but don’t be afraid to create new traditions. Above all, if you or someone you know is struggling with depression, get help, see your doctor and meet with a trained counsellor. There is hope.

That’s our show for today. Full show notes are available on our website including links to many of the resources provided by Carizon, so please to our website at hoyes.com, that’s h-o-y-e-s.com for more information. Thanks for listening. Until next week I’m Doug Hoyes, that was Debt Free in 30.

Thanks for listening to the radio broadcast segment of Debt Free in 30 where every week your host Doug Hoyes talks to experts about debt, money and personal finance. Please stay tuned for the podcast only bonus content starting now on Debt Free in 30.

Doug Hoyes: It’s time for the podcast only segment here on Debt Free in 30. We ran out of time on our radio only portion of the show talking to Theresa Karn about depression and anxiety and we were talking about specific things you can do. And there’s a few points we didn’t get to, one of them being it’s a good idea to enjoy the outdoors when you’re in a situation like this. Why is that? Why does that help? Is it the change in routine? What’s the rationale there?

Theresa Karn: There are a couple of reasons, Doug. One is to just get out, breathe the fresh air. The outdoors is so beautiful. If you can get out into the woods, you just get a different view point than sitting in a room, looking at the four walls. But also if the sun is shining, the sun is really good for mood as well, so important to get out into the sun.

And, you know being outdoors is something that you can enjoy and it doesn’t cost any money. You can go for a walk with your kids. A new thing that people are doing is geo-cashing;,it’s a great activity, it doesn’t cost any money. Kids really enjoy it. So, there are things you can do outdoors as a family or as an individual that can help with depression.

Doug Hoyes: Yeah and the ones that don’t cost money, that’s the best kind of all. You’re not going to make worse your debt situation. So, what then is your final piece of advice then to people who are suffering through these issues?

Theresa Karn: Studies show that the best way to treat depression is a combination of medication and counselling together. So, I would suggest that you explore both of those things. It’s important to see your family doctor and talk about how you’re feeling and what has changed. Because, as I said at the beginning of the show, there could be medical conditions that are going on that are causing the depression so that needs to be ruled out as well, and then medication can be very helpful.

And then coming for counselling, reach out, reach out to people who care, reach out to people who are supportive. You may have those people in our life, and then get some professional counselling. Because there are a lot of ways that counselling can help to look at negative thought patterns that are deepening the depression and maybe even look at life’s circumstances that are also contributing to the depression.

Doug Hoyes: And I guess the final point that we hit on from before is that you’re not alone in this.

Theresa Karn: No, absolutely.

Doug Hoyes: Depression is something, based on the statistics you quoted, one in ten people will encounter at some point in their life, so sitting there hoping it will go away, it’s exactly again like dealing with debt problems, they don’t go away on their own in most cases. So, reaching out to friends and family but also reaching out to professionals, doctors, counsellors and so on is very important.

Theresa Karn: Absolutely.

Doug Hoyes: Excellent. I think that’s a great way to end it. Thanks for being here, Theresa.

Theresa Karn: Thank you.

Doug Hoyes: That was the podcast only bonus segment here on Debt Free in 30. We’ll be back next week with a new episode. Thanks for listening.

Announcer: Thanks for listening to the podcast only bonus segment of Debt Free in 30. For more information on today’s show please go to hoyes.com, that’s h-o-y-e-s-dot-com and type the word podcast into the search box for more information on every episode of Debt Free in 30. Until next week, this was Debt Free in 30.

Gail Vaz-Oxlade is back on the show to discuss her new book, Money Talks: When To Say Yes And How To Say No. Gail is our most downloaded podcast guest, and this is her FIRST podcast interview for her new book! Gail starts out the episode by exclaiming,

I’m so excited for this new book, I cannot begin to tell you! My toes are curling!”

So you know it’ll be a good one!

Not only does she give away a few secrets about the not yet released book, but she also gives us actionable advice and tips for starting the conversation about money. The topic of the book is one that hasn’t been written about before, “nobody has actually done this before. Nobody has actually talked about how to have these conversations with the people in your life.”

Communication Is Key

Unlike her past books that focused on technical financial processes, Gail’s newest book is all about why and how we should communicate about money. She explains that

how we communicate about our money is what’s at the root of whether the money is working for us in our relationships.

Simply put, we need to start talking about our needs and wants with our friends, family and significant others. If we don’t talk about money – how much we have, where it’s going, how much we owe and how it makes us feel – money will continue to be a problem in our lives.

Gail offered up a quote directly from her new book and it sums up the need for communication perfectly:

We are the problem. How we behave—what we do with our money and how we communicate about that behaviour—is at the root of most of the challenges we face with, and blame on, money.

The Power Struggle

I ask Gail why we’re all so secretive about our money and she quickly identifies power and control as main motivators for avoiding money conversations. When it comes to power struggles a few scenarios make it easier to block others out:

Not including children in our money conversations to maintain a sense of power;

Primary Breadwinner Syndrome or the “I make the money, so I decide how it’s spent” rule;

Keeping your spouse in the dark about your finances;

Financial bullying by one spouse; and

The patriarchal/matriarchal money approach.

What’s more, Gail points out that it’s common to fall victim to the Recency Effect and that we believe that where we are now is where we’re always going to be. Instead of having productive conversations about money and debt, people cast themselves in a certain role, unwilling to change their own behaviour.

Gail uses the example of “The Nagger” where one person is constantly nit picking someone else. In her book, Chapter 11 is titled “I Can’t Hear You” and delves into why it’s important to listen to yourself and put yourself in the other person’s shoes to change your situation. Gail points out that, “if you don’t want that role, I have a way for you to get out of that role”. You just have to be willing to open your lines of communication.

So how do you do that?

Get Rid Of Your Emotional Attachment To Money

Money is a physical entity. Money is not a feeling and it’s certainly not an emotion.

But we attach emotion to our money, making it hard to talk about. Gail got her idea for the book from the hundred of letters she receives from people, and from the numerous television shows that she’s hosted. A common thread between all of those questions and comments was a lack of communication and people’s unwillingness to talk about money because they’d become emotionally attached.

To get past the emotion, Gail’s book includes over 70 scenarios for readers to relate to. Through those scenarios, readers will be able to visualize their own situation and better understand how to deal with conversations about money. To make it even easier, Gail provides you with the type of language that you should be using because as she explains,

I believe with all my heart that until we tell each other the truth about what we’re feeling and how we’re responding, what we’re doing is we are creating a mythology that can’t hold. There is no way we can keep this mythology going forever and what will happen is the whole thing will dissolve and we’ll just get bitten in the butt.

Listen to the full podcast for more information about:

Why parents should teach their children about money early on

This is episode number 66 of Debt Free in 30. And since this is a weekly show that means we’ve been on the air from more than 15 months. And I can tell you based on the download statistics I get for the podcast version of this show, my most popular guest in the last 65 weeks is none other than Gail Vaz-Oxlade host of three television shows, her own radio show and the author of many books including a brand new book that we’re going to talk about today.

Gail was my guest back on show number three and she gave a very interesting explanation for why she has no desire to go back to being a host of a reality T.V show. So, if you haven’t listened to that episode, check it out on our website on hoyes.com or on iTunes or wherever you get your podcasts. So, what’s been Gail up since we last talked? Let’s find out, Gail, welcome to show. How are you doing today?

Gail Vaz-Oxlade: I am great, Doug. How are you?

Doug Hoyes: I am great. It’s fantastic to have you back on. We’re recording this on December the 1st, 2015 (if I’ve got my calendar right) and it will be released as a podcast and on the radio December 5th. And I understand that on Tuesday December 8th, the new book hits the shelves in the bookstores. So, is this the first podcast interview you’ve done about this book, Gail?

Gail Vaz-Oxlade: It absolutely is and I am so excited for this new book like I cannot even begin to tell you. My toes are curling.

Doug Hoyes: Well, so let’s hear about it then. What’s the name of the book?

Gail Vaz-Oxlade: Okay, so the book’s called Money Talks with a subtitle When to Say Yes and How to Say No. And it is – the whole idea behind this book is that how we communicate about our money is what’s at the root of whether the money is working for us in our relationships.

Very often, people will say money is one of the things that causes relationships to fall to rack and ruin. And my premise in writing this book is that, you know what? If we don’t start talking about this, if we don’t start getting better at communicating what our needs and wants are to our family, to our friends, to our mates, then we will just keep on this sort of hamster wheel of making money become a problem in our lives instead of being no more than a means of making a transaction.

Doug Hoyes: So, money is a medium of change is what you’re saying.

Gail Vaz-Oxlade: That’s right. That’s all money is. But how we respond to each other, that has a big influence on what we end up doing with our money.

Doug Hoyes: So, money isn’t the problem, we’re the problem.

Gail Vaz-Oxlade: There’s a line in the book that says “we are the problem. How we behave, what we do with our money and how we communicate about it, that’s at the root of most of the challenges that we face and blame on our money”.

Doug Hoyes: So, we say my problem is I don’t have enough money, I don’t think too many people complain about having too much money.

Gail Vaz-Oxlade: But they’re more things, they’re things about not being able to get our mates to make a budget, not being able to impress upon our sister that our couch is not her ongoing bed. Not being able to communicate with our parents that, listen dudes, don’t think I’m your retirement plan ’cause I got my own crap going on. And if you think that you’re moving into my basement because you made me, then we need to talk about this.

Doug Hoyes: And the same with your kids, I guess.

Gail Vaz-Oxlade: Totally the same with your kids! You know, one of the things that I try and impress upon parents is that if you are enabling your children, if you are constantly bailing out your kids, what are they going to do when you drop dead?

Doug Hoyes: Yeah, they got a big problem. Well, and I’ve always said to my kids I got two teenage boys, I’ve said you know what? When I’m gone, I’m leaving all of my money to a cat charity. And I don’t have any cats, I don’t particularly like cats, but the point is well you’re not going to get any of it. So, you better go out there and earn your own money, make your own way.

Gail Vaz-Oxlade: And I’ve said exactly the same thing to my kids.

Doug Hoyes: Cool.

Gail Vaz-Oxlade: Absolutely. You know, because Doug I have watched people who have sat and waited for their relatives to die to solve their financial issues. Because they think that if they can spend all the money they want right now, they don’t have to save anything for retirement if they rack up debt it’s okay because there’s this trillion dollar inheritance that the media’s been talking about for years. And I’m here to tell you that trillion dollar inheritance is going to go into healthcare and personal care for your folks because they’re going to live a long, long time and all the money’s going to be gone.

Doug Hoyes: Yeah, you’re right. If my parents live to be 90, from 80 to 90 they’re heavy consumers of healthcare services, you’re right, that money ends up getting eaten up. So, you’re saying that we’re unwilling to talk about money, why? Why the big secret? What’s the issue?

Gail Vaz-Oxlade: I scratch my head. Okay, the thing is that what we’ve done is we’ve allowed a lot of emotion to link itself up to our money. So, one of the things that I talk about in the book is the fact that other people are very good at pushing our emotional buttons. And by pushing those emotional buttons they can derive the reaction that they’re looking for. But really it goes even further back then that because parents seem unwilling to talk to their kids about money, how it works, what you can or cannot do with it, even as we are raising children in a world where we know that if we don’t educate our kids about money, what we’re doing is sending them off into the wolves’ hands.

So, I think this whole thing about money and not talking about it is so rooted in us, it doesn’t really matter where it started, the fact is until we cut it out, until we get rid of this monster emotional attachment to our privacy – just think of all those guys that do those articles and they hold up newspapers in front of their faces or they hold up buckets of popcorn in front of their faces. They’re perfectly happy to share their financial deets but only if nobody knows who they are.

Doug Hoyes: So, we have no trouble talking to our kids about you know, you shouldn’t do drugs and you shouldn’t drink and drive, but –

Gail Vaz-Oxlade: But money, which is something everybody has to deal with in their life, and it’s no more emotional than the paper and coin of which it’s made. Paper and coin is not emotional. That’s the thing that we don’t want to have a conversation with our kids. We don’t want to tell them how much we earn. We don’t want to tell them how much we’re spending for rent or what we’re paying for our car payments. I don’t understand it.

Doug Hoyes: Is it a power thing?

Gail Vaz-Oxlade: Sometimes it is. Sometimes it is and that’s one of the things that I talk about in the book, this whole idea of power and control and how we use money to sort of maintain our sense of power and control. It’s lousy, Doug, because let’s face it, the last thing you want to do is teach your children that the person who has more money has power and control over them. You want your children to grow up strong and healthy and knowing the place where money should play in their life. Not believing that he who has the most money has the most power.

Doug Hoyes: And I would assume that can have a pretty detrimental effect on relationships as well.

Gail Vaz-Oxlade: Absolutely. And so the book deals with a whole bunch of power issues that people are sort of still coming to grips with. You know, this whole idea of primary bread winner syndrome; you know the guy who makes all the money gets to make all the decisions. Or we’ll just keep little old sweetheart in the dark about what we’re doing with our money because what she doesn’t know can’t hurt her. Bullying is a big issue in couples where one person ends up being a financial bully in the relationship. Then there’s the person who takes a very patriarchal approach. And this is not just men, the patriarchal or matriarchal approach can be women as well, but this whole idea that I’m in control here and I make the decisions about what’s going to be happening with our money.

Doug Hoyes: Yeah and that has a horrible effect if the – it’s typical now that women outlive men. And so if in a traditional set up, the man is making all the financial decisions or even just he’s the one who writes the cheques, if we still write cheques anymore, and then he passes away five or 10 years before his wife does. And now all of a sudden late in life she’s got to figure out how it all works, that’s got to be pretty damaging as well I would think.

Gail Vaz-Oxlade: And I’ve actually seen role reversal on that. And that’s one of the things I talk about in the book is role reversal because we now have a dynamic where women are making more than their male partners and that’s having some significant impact on how they relate to each other. Again, it should not. I mean if you take the emotion out of it and you deal with the resource this family has, then it’s not about the emotion attached to it. But unfortunately, there is emotion attached to it.And so you have to figure out the words to use in order to take the emotion out and make this be a discussion about resources, not about power and control.

And that’s one of the things that I’ve done in the book that’s a little bit different is that I have created dozens and dozens of scenarios where people will see themselves or see people they know and love, and finally come to some sort of understanding of what the dynamic is that’s going on there.

Doug Hoyes: So, it’s almost a series of 50 different plays or whatever if you want to look at it that way.

Gail Vaz-Oxlade: There are about 70 scenarios in the book. And the idea being that if you can see yourself in this scenario, you’re much more likely to understand why you have to take the steps that you have to take cause every chapter deals with my advice to you in terms of dealing with the denial issue or the entitlement issue or the control issue. But also here are the steps that you’re going to have to take if you want to be the person who fixes this problem. You don’t fix the problem then you can’t whine about the fact that the problem continues to exist.

Doug Hoyes: So, if someone is listening to this today and they’re in a relationship where their spouse is either overly controlling or whatever the opposite of overly controlling is and they realize there’s a problem, what you’re saying is you’ve got a scenario in this book that talks about how to identify that and then what to do about that, how to play it out?

Gail Vaz-Oxlade: Absolutely. And I give the words; I give you words that you can wrap your head and your tongue around. I’m not saying these are the only words you should use, but at least there’s a starting point for the language you can use because I’ve had heaps and heaps of experience with this. I mean, after working with all those people on television, believe you me, I had to come up with some tactful ways of saying some things.

So, some of this is tact and some of this is just straight up telling the truth. Because I believe with all my heart that until we tell each other the truth about what we’re feeling and how we are responding, what we’re doing is we are creating a mythology that can’t hold. There’s no way we can keep this mythology going forever. And so, what will happen is eventually the whole thing will dissolve and we’ll just get bitten in the butt.

Doug Hoyes: So, can you give me an example of the wrong way to do something or the traditional way that gets people into trouble, anyone of these scenarios. I mean, make people buy the book so they can find out how to do it right, but what’s an example of the wrong way to do something? Words we use that are wrong, inflammatory words, how do we make mistakes in these areas?

Gail Vaz-Oxlade: Well, in part two, which is called “changing the game”. The idea is that people really hate change and that as human beings we suffer from something called Recency Effect, meaning that we believe that wherever we are now is where we’re always going to be.

Unfortunately, what happens sometimes is that people cast themselves in the role of The Nagger. And so what we do is we go nah, nah, nah, nah, we jump on every little thing that the person does and we’re not about changing behaviour in a productive way that we’ll be sustainable with such a resort of picking on things that are really less relevant than the thing that’s actually the elephant in the room.

And so, I try to encourage people to not take on the role of The Nagger, understanding that when you nag, what happens is eventually and this is the title of the chapter, “I can’t hear you”. People just plug their ears. And so if you want to bring about real change in a mate, in a sibling, even in your parents you need to walk away from the nagging role and you need to deal with whatever it is you have to deal with in a very straight forward, very truthful, very loving, but very firm way.

Doug Hoyes: Because we’re not in grade two, I guess.

Gail Vaz-Oxlade: Well, it’s not even a matter of not being in grade two. I can’t tell you how many times I’ve seen scenarios play out where people think that the nah, nah, nah is going to work. Like, really? In what world would you want to be nagged like that? So, part of understanding how your mate is responding or how your sister is responding is putting yourself in their shoes and listening to yourself for a minute because if you sound like that horrible harridan then nobody’s going to hear what you have to say.

Doug Hoyes: Well, and this why I’ve always like your approach. What you’re really saying at its very core is we got to think, we go to take responsibility for ourselves. If the people I interact with in my life aren’t behaving the way I want them to behave, it’s really a problem with me not a problem with them.

Gail Vaz-Oxlade: Well, it’s part of a problem with you and a problem with them because let’s take the example of Peter Pan. This is something that psychologists have studied for awhile and so we know it’s a thing, Peter Pan syndrome. And all the people who plunge themselves in the Wendy role they share this dynamic. And so you need to understand what the dynamic is. Sure you can identify, we’ve seen lots of people say it’s a boy/man. But what do you do about it? How do you change the dynamic or how do you change your own life so you’re not having to live in this dynamic anymore? And sometimes that change is really, really hard to make, but if you are not prepared to make the change then at the very least stop whining.

Doug Hoyes: Because the whining isn’t doing anybody any good.

Gail Vaz-Oxlade: No, it’s not. So, if you love this person so much that you’re prepared to put up with his or her crap, then put up with his or her crap. Don’t then turn around and make yourself into the victim because really you have accepted that role. If you don’t want that role, I have a way for you to get out of that role.

Doug Hoyes: And you’re talking about the dynamic in families, relationships, but I guess this extends to just co-workers and friends as well. You got that guy at work who always wants to borrow $20 till payday.

Gail Vaz-Oxlade: Absolutely, and so that’s exactly one of the scenarios that I talk about, the whole idea that there are always people who seem to be willing to tap your wallet, whether it be for a short-term loan or yet one more collection at work for the gift. This thing has always boggled my mind. People come to work with us, we don’t throw them a party. We’re going to spend the next six months, six years, 16 years with this person, but we don’t welcome them. Instead what we do is we wait for them to be leaving and then we throw them a party.

Doug Hoyes: And so the scenarios you talk about in the book are, one of them is how to not be bailing people out all the time.

Gail Vaz-Oxlade: Yep, how to say it with kindness and love, but say it quite explicitly; I’m sorry, I’m not going to let you tap my wallet anymore.

Doug Hoyes: And I think in a lot of cases I’ve dealt with people, I’ve had to do bankruptcies for people and I say what happened? Well, you know, I helped out my kids, I helped out my friend and they weren’t able to pay me back. And I’m going well I’m absolutely a big fan of helping people out, I think that’s fantastic, but I don’t believe in going deep into debt to do it. If you can help someone out with the cash in your pocket that’s your cash, great fantastic, but when you have to go into debt to do it, you’re causing yourself a great deal of difficulty. So, you’ve got scenarios in here to help us understand how far you should go or more the words to not get into that mess in the first place.

Gail Vaz-Oxlade: Well, the recognizing that there are people out there using guilt as an emotional button or using fear, – like “if you can’t keep a way to help your brother then you’re not the child I thought you were”. It’s like a parental bullying. Very often I get letters from people who explain situations to me and what they’re looking for is the way to say no, they don’t have the words to say no. Because every expectation is that they’re going to say yes, which is why the sub-title is when to say yes and how to say no. And so people will write to me and they’ll say how do I say no to this? And so I give them the words and that’s really where this book came from. It came from hundreds and hundreds and hundreds of letters that I get from people asking me, Gail, what do I say?

Doug Hoyes: And so, you’ve been working on this book for awhile, then?

Gail Vaz-Oxlade: I have been working on this book for awhile. I think this is, you know, when I first started, Doug, when I wrote that Debt Free Forever it was a process book. Debt Free Forever is all about how to make a debt repayment plan, how to create a budget, how to set some goals for yourself, how to start saving. It’s the foundation book. When I wrote Never Too Late, it’s how to save for retirement. And so there are process books that I have written. When I got to Money Rules it was my final attempt to get the common sense of money out there. These are all the things that you should have told your children that you didn’t, at least go buy them the book and hand it to them, okay? So, things like renting is not a waste of money.

Doug Hoyes: I agree.

Gail Vaz-Oxlade: Some people have to rent. Home ownership is not for everyone. Things like embrace anticipation. Things like it’s not your money until it’s in the bank ’cause I’ve had people write to me long sad letters about how they were going to get a bonus, went out and spent the money on their credit card and oh woe is me, the bonus never came through and so now they’re in debt, it’s not their fault – hello! It’s not your money until it’s in the bank.

So, that was the common sense of money. What this is, is the last piece is missing. Nobody actually has done this before. Nobody has actually talked about how you have these conversations with the people in your life. How do you say to somebody you love, you know what? You’re an instant gratification junky and we need to talk about that. Or I can’t go on that vacation with you because in good conscience I can’t watch you spend you haven’t saved for something stupid. So, I love you, you are my friend, I would love to go on a vacation with you, but you have to show me you have the money in the bank before I’m prepared to do that because I can’t come back and listen to your whining for the next six months.

Doug Hoyes: That’s a great way to end the segment, so the book is called, Money Talks: When to Say Yes and How to Say No. Gail Vaz-Oxlade’s new book hits the stores December the 8th. Gail, thanks for being here.

Gail Vaz-Oxlade: My pleasure.

Doug Hoyes: It’s time for the Let’s Get Started segment here on Debt Free in 30. I’m joined by Gail Vaz-Oxlade. We’re talking about her new book, Money Talks: When to Say Yes and How to Say No.

So, Gail a real common one that I think parents would get is can you buy me that thing? I need that thing, I need that thing. And so of course as a parent my standard response would be, what do you think, I’m made of money? Money doesn’t grow on trees. And as you said in the first segment probably being a whiny, naggy person is not the correct approach. Is that a common issue you see and if so what mind frame should parents think through to stay out of that?

Gail Vaz-Oxlade: It absolutely is common. I mean that’s why those statements like what, do you think I’m made of money or do you think money grows on trees have just become standard. But they actually don’t teach anything so all you’re doing is losing the opportunity to teach a really important lesson when you let these things go by.

And you know, I am one of the people who believes that teaching about money belongs at home. I know there’s a big push to put it into schools, but really to teach about money it has to be an ongoing thing, it can’t be three classes in the math section and two classes in social studies. It needs to be consistent and it needs to be ongoing.

And you need to give kids some money to deal with it. So, the single best way of eliminating the “buy me this won’t you dad”, is to start giving your kids the money that you would normally spend on them as an allowance and then setting some expectations about what they do with that money. And so, if they want to buy the latest game for their system or they want to buy a new pair of shoes or they want to buy whatever, you simply say, do you have the money for that, ’cause if you have the money for that go nuts babyo. But if you don’t have the money for that I don’t want to hear about it.

Doug Hoyes: So, the answer to the kids is you can buy whatever you want with your money, then.

Gail Vaz-Oxlade: That’s right and we as parents need to stop thinking of an allowance as money we give our kids to throw away because that’s not what an allowance is. Allowance is what we would normally spend on our children put in their hands so they can learn how to manage money.

Doug Hoyes: And I assume that’s something that would vary with the age of the child, obviously.

Gail Vaz-Oxlade: Absolutely. And so I started both my kids on allowances when they were six years old and over time they got more money. By the time my daughter, Alex was 12, she was getting her clothing allowance monthly. And she had to learn to manage that money, make choices about what she was going to do with that money because that money was a finite resource. And so, when the money ran out she had to stop spending.

My son was just home from college. He has a very strict budget that he has to live on while he’s at college. And I said to him, so how are you doing on the money front? And he said well I only got $50 left to last me to the end of the month because he went out and bought a few things at the beginning of the month and so then he had to pull back. He had to reign in what he was spending because he had a limited amount of money that he had to – couldn’t get more before the end of the month.

And you know, Doug, he has all the money in a savings account. He’s only allowed to transfer over $650 a month to cover all his costs while he’s at school. And that’s what the rule is. So, you take more than that and Mommy will slap you silly.

Doug Hoyes: Yeah but when he gets out of university, he will have practiced this for years and years and years.

Gail Vaz-Oxlade: Absolutely. And this is the thing I say to parents, why would you want your children to fail where they’re not safe? Far better they have the opportunity to try and they will bruise their knees from time to time. And that’s okay, then you have a discussion about how they’re going to fix the problem. You don’t rush in with your cheque book.

Doug Hoyes: And do you – I mean obviously you believe in having an allowance for a child and you said an allowance is what I would have been spending on your clothing anyways, I’m going to give you that money give or take. What about actually paying children for chores they do. Do you believe in that or not?

Gail Vaz-Oxlade: Well, I’m of two minds on the chore issue. The first is that the chores that kids normally do around the house they should not be paid for because nobody pays me to cook them dinner.

Doug Hoyes: They’re part of the family, they have to contribute.

Gail Vaz-Oxlade: Absolutely. But if you want to find a way to put more money in their hands so that they can achieve some goals that they’re really working towards, then you can create a honey do list with dollar values attached to the things you want them to do around the house. So, if I had a cat I would be more than happy to pay my kid to clean the cat litter; I’m not going anywhere near that box.

Doug Hoyes: I got you. So, doing the dishes every night, that’s something we’ve all got to do. But cleaning out the gutters or cleaning the cat litter or whatever, well, okay that’s kind of over and above. That’s something you would potentially consider paying them an allowance for.

Gail Vaz-Oxlade: Absolutely. Anything I would be willing to pay someone else to do, I’m happy to pay my kids to do.

Doug Hoyes: Excellent. Well, that’s an excellent perspective on it. You’ve got to start them young and then they learn how to do it.

Gail Vaz-Oxlade: Absolutely, get lots of practice.

Doug Hoyes: Great, thanks very much, Gail. I appreciate you being on the show today. That was Gail Vaz-Oxlade, talking about her new book, Money Talks: When to Say Yes and How to Say No. It’s available at fine book stores everywhere. It’s available at Amazon and other places that you buy books. There is apparently also a Kindle version if that’s how you prefer to consume it.

So, you can go to hoyes.com and the show notes have links to all that information including to Gail’s website. So, check out the new book Money Talks. That was the Let’s Get Started segment; I’ll be right back to wrap it up right here on Debt Free in 30.

Doug Hoyes: Welcome back, it’s time for the 30 second recap of what we discussed today. On today’s show Gail Vaz-Oxlade told us about her new book, Money Talks: When to Say Yes and How to Say No, where she presents dozens of examples of how to talk to friends and family members about money. That’s the 30 second recap of what we discussed today.

As Gail said during the show, she’s written books in the past about the process of budgeting and money management but his book is entirely about helping you see your situation through stories that reflect what you may be experiencing. Her hope is that by recognizing your situation you could learn the actual words to say to negotiate a solution. That’s a subject that I don’t think has been covered in any current book about money so it should be a great help to many people dealing with money problems.

That’s our show for today. Full show notes are available on our website including links to Gail’s website and information on where you can buy her new book. So please go to our website at hoyes.com for more information. Thanks for listening, until next week, I’m Doug Hoyes. That was Debt Free in 30.

Whether you are buying a home or refinancing, in today’s world you have a lot of choice as to who your mortgage lender will be. More and more Canadians are turning to alternatives to the big banks like credit unions, mortgage brokers and large companies that specialize in residential mortgages. This is particularly true for those who are having money problems. If you have a low credit score, getting a mortgage approved by a traditional big bank might be difficult. Self-employed individuals are finding it particularly hard to be approved for a loan through a conventional mortgage after the federal government tightened lending rules.

We wanted to know if there was a trend in the mortgage lending products used by insolvent debtors and if certain mortgage products were more likely to lead to a higher degree of risk for consumers.

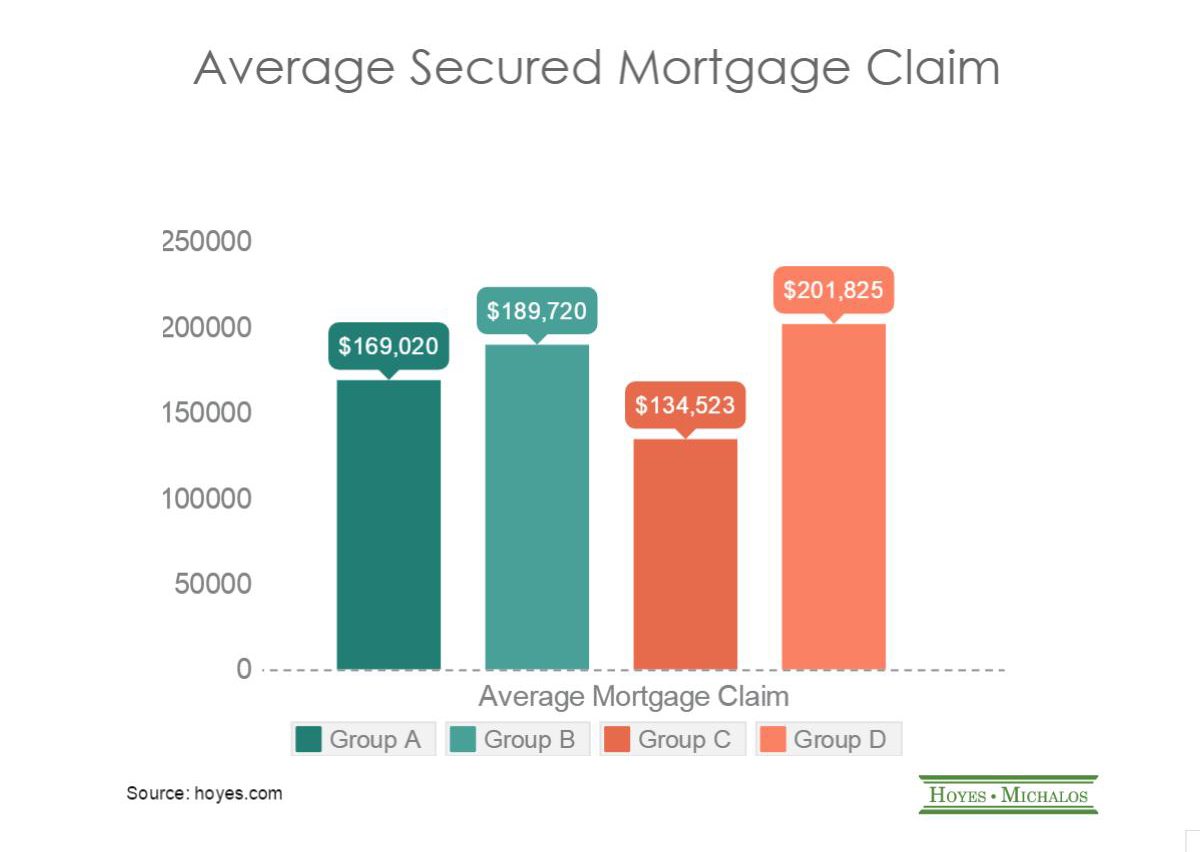

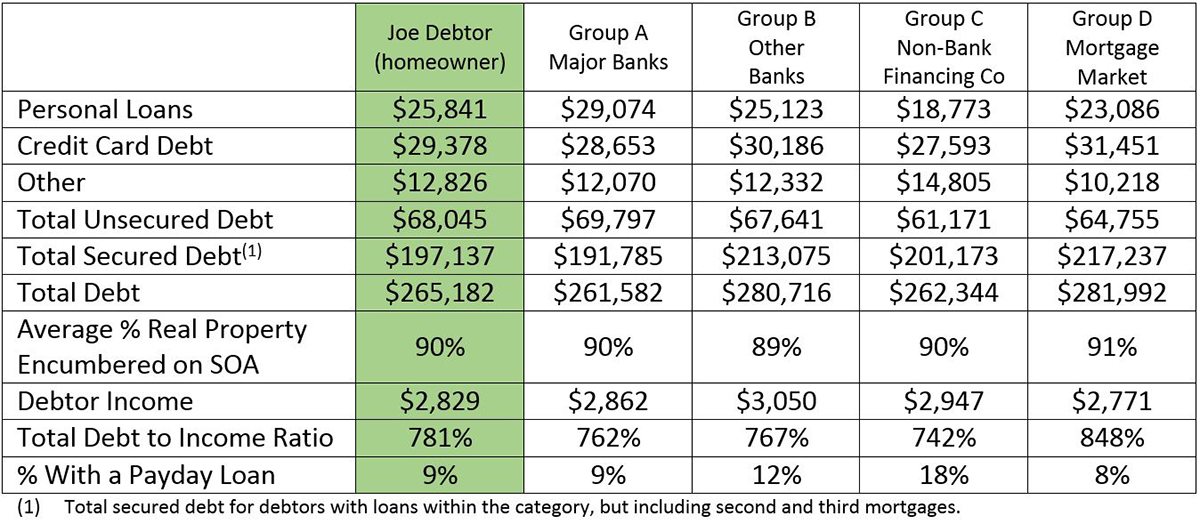

To find out, we turned once again to our Joe Debtor data. We looked at insolvent homeowners and compared their financial statistics based on the type of mortgage lender they used:

Group A: Canada’s 5 largest traditional banks.

Group B: All other banks.

Group C: Traditional non-bank financial institutions that offer broad based lending products – trust companies, credit unions, life insurance and financing companies.

Group D: Brokerage based or mortgage market lenders consisting of mortgage financing companies and large private lending options (mortgage investment corporations).

Alternative lenders have a larger share of claims filed

What we found was that mortgage claims filed by Canada’s 5 major banks declined over a four year period from 55% in 2011-2012 to 52% in 2013-2014. Mortgage claims filed by all other lender groups increased over that period. What’s more, brokerage based mortgage lenders accounted for more than one in four of all insolvency claims (26%).

Effectively, Canada’s traditional large banks appear to be reducing their exposure to high risk consumer mortgages. This leaves consumers increasingly turning to alternative mortgage lenders.

Mortgage market lenders offering larger, and riskier mortgages

Our study showed that, among insolvent homeowners, brokerage based mortgage market lenders have the highest average claims of all lending groups.

In addition to having the largest average mortgage claim, debtors who accessed mortgage market lenders also reported a mortgage encumbrance rate of 91%, higher than all other lender groups. So while all insolvent debtors had high ratio mortgages, those who went through a broker had the highest risk ratio. Combined with a very high credit card debt, these debtors ended with the highest total-debt-to-income ratio of all borrower groups.

Traditional non-bank lenders and smaller banks are choice for debt consolidation

The small average mortgage claim filed by Group C lenders (credit unions, trust companies and traditional non-bank financial institutions) is a bit deceiving. It doesn’t mean that debtors who took out mortgages from these lenders have less debt. What we found was that debtors are more likely to turn to these institutions for second mortgages and debt consolidation loans. Almost one in three (30%) debtors who carried a secured mortgage with a Group D lender also carried another mortgage (or two) with other lending groups. Smaller banks experienced a similar trend.

Interestingly this same group of borrowers, who are more likely to carry more than one mortgage, are heavy users of payday loans. Almost one in five (18%) of debtors who have a mortgage from a traditional non-bank financial institution, and 14% of small bank mortgage borrowers, also have outstanding payday loans compared to only 9% of all homeowners.

This is likely because insolvent debtors often pile debt on top of debt in order to maintain their existing debt payments. This may initially begin with an expensive debt consolidation loan, but eventually ends with multiple payday loans until the pile becomes too crushing to continue. The end result of often insolvency.

What Does It Mean?

The increase in access to alternative lending products for most Canadians is good. Mortgage brokers can often secure favourable terms for lenders in the form of competitive interest rates. However this also means many borrowers can be approved for larger mortgages than they can really afford.

Regardless of who you choose to finance your mortgage, our data clearly shows that any high ratio mortgage, when combined with other unsecured debts, significantly increases an individual’s risk of filing insolvency. So by all means, shop around, just make sure you are looking not just for a better rate, but for something that you can maintain in the long term.