We receive a lot of comments on our Facebook page from individuals struggling with debt who are afraid to consider something like a bankruptcy or consumer proposal because it will have a negative effect on their credit. Yes, filing bankruptcy or a consumer proposal will appear on your credit report. But so will many other bad credit activities which may be harming your credit score already including:

Maintaining high credit card balances relative to your limit;

Regularly exceeding or maxing out your credit limit;

Applying for multiple credit cards and loans; and

Having mostly credit card debt.

The truth is if you have too much debt, you probably already have poor or bad credit and it’s getting worse every day that you continue to struggle.

Having to rely on loans that carry very high interest rates means that you end up using a larger portion of your income to maintain your debt payments. The result is a cash flow shortage, forcing you to turn to more credit to make ends meet. This kind of bad debt cycle is exactly the type of situation every person we talk to faces each and every day. It usually breaks when they find out they have no more debt options left.

While it may sound good to read a list about how to rebuild your credit, the steps are meaningless if you are caught in a quagmire of debt. Deal with the debt first, then begin the credit repair process.

Still not sure you believe me? OK, let’s run through a case study. Taylor was a 40 year old, single, graphic designer. Work in her field was fun and challenging, but not necessarily steady. A few layoff periods caused her to rely on credit cards to get by and her debt ballooned. After returning to work, she faced almost $33,000 in unsecured debts and a car loan.

Credit card A: $8,500 on $10,000 limit

Credit card B: $2,000 on $2,500 limit

Credit card C: $2,500 on $2,500 limit

Store card (furniture financing): $10,000 on $10,000 limit

Car loan: $23,000 (original $27,000 – 6 year term, 58 payments remaining)

Looking at Taylor’s situation, her credit utilization rate was 88% – way above the recommended 30%. In addition, credit card and high debt financing totaled half of all of her debt. Her credit capacity for new credit was almost nil, unless she wanted to start considering expensive alternatives like payday loans. What’s worse is that her monthly debt payments were $1,190 a month using up 48% of her take home pay. It would be difficult for Taylor to lower her credit utilization rate and build a better credit profile while paying down this existing debt. No way would she be able to apply for better credit. Taylor chose to file a consumer proposal and clear up her debts.

Taylor’s Credit Rebuilding Process

File a consumer proposal for $10,500 based on her income to eliminate her $33,000 in debt. That was a savings of $22,500.

Make her monthly payments of $175 a month for 60 months towards the proposal. Her new payments were now only 7% of her monthly income, a big drop from 48%.

The elimination of her high debt payments increased Taylor’s cash flow sufficiently so that she no longer needed credit to balance her budget.

Set aside $100 a month of the amount she was saving in a TFSA for an emergency fund in the event of another temporary period of unemployment and for future savings.

By the time her proposal was complete Taylor had a TFSA balance of $6,000.

Using a portion of the money she saved during proposal, Taylor applied for a $1,000 secured credit card for personal convenience and to begin the process of rebuilding her credit. She consistently paid off the full credit card balance each month, which provided future lenders a credit history of consistent debt payments and a low utilization rate on her new credit card.

Three years after signing up for her proposal, Taylor also paid off her car loan. Her consistent loan payments during her proposal also helped to rebuild her credit. And with her savings she was a long way towards having a good down payment when she would need to replace her car.

Two years after her proposal was completed, Taylor was able to apply for a small RRSP loan, a further step in showing her ability to manage credit wisely.

Three years after her proposal was completed, the notice of her bankruptcy was removed from her credit report.

So yes, a proposal did appear on her credit report however Taylor learned to live without credit during her proposal (largely because she no longer needed credit to pay for living expenses) and was able to start rebuilding her credit while in the proposal.

This same process works whether you file a bankruptcy or proposal. By the end of your proceeding, you can have savings in your bank account and successfully restore your finances and credit in the event you want to qualify for another car loan or a mortgage in the future. If you have significant debts on your credit report today, it is unlikely you will achieve those objectives any sooner while trying to eliminate high cost credit card debt on your own.

If you’d like to ask more about how a proposal or bankruptcy can eliminate your debt, and what the steps are to rebuild your credit, contact one of our Licensed Insolvency Trustees for a free consultation.

It is possible to rebuild credit after a bankruptcy or proposal. We're here to help with our Free Online Video Course. Get step-by-step instructions on how to repair your credit after filing.

On today’s podcast we talk with Ted Michalos about the Office of the Superintendent of Bankruptcy and how they regulate the bankruptcy process, and trustees, in Canada and why they changed the name from bankruptcy trustee to Licensed Insolvency Trustee (LIT).

A Short History of Bankruptcy in Canada

The first federal bankruptcy legislation was enacted in Canada in 1869 – almost 150 years ago. At the time it was called An Act Respecting Insolvency and only applied to businesses, not consumers. In 1919, the federal government passed the Bankruptcy Act for both individuals and business. Trustees at the time were appointment by the government until, in 1932, the Office of the Superintendent of Bankruptcy was created and given power to grant licenses to bankruptcy trustees.

This short history lesson about bankruptcy and bankruptcy trustees in Canada is interesting because after 84 years, the federal government is officially changing the designation of a person who administers bankruptcies in Canada from ‘bankruptcy trustee’ to ‘Licensed Insolvency Trustee‘.

Given these changes, on today’s show we talk with licensed insolvency trustee Ted Michalos about how bankruptcy law in Canada works, who the players are and why the government may have made this change.

Office of the Superintendent of Bankruptcy Canada

The Office of the Superintendent of Bankruptcy (OSB) is directly responsible for licensing, monitoring and controlling all aspects of insolvency in Canada. This means they supervise the administering of estates and license and oversee the conduct of trustees.

Their role is to ensure that the bankruptcy process is fair and equitable for all stakeholders. As Ted says:

The system is designed to be fair to the individual; it’s designed to be fair to the people that you owe money to.

To maintain this system, the OSB sets standards and policies that all trustees have to follow. This includes releasing directives such as the annual surplus income guidelines and the new directive 33 changing our name to Licensed Insolvency Trustee or LIT for short.

The Bankruptcy & Insolvency Act

The purpose behind the Bankruptcy & insolvency Act (BIA) is to:

provide a sense of structure, framework and legal protection so creditors can’t sue you, garnishee your wages, freeze your bank account or take advantage of you;

debtors get simplification – one monthly payment to one place;

creditors get fairness in terms of their financial recoveries

Ted explains that debtors are:

automatically entitled to this protection as part of the law. And the reason they do that is to make sure that all of the people you owe money to are treated the same way and that you are treated fairly.

Regulating Trustees

It is trustees who are regulated and licensed by the federal government to provide insolvency services through the BIA. Unlicensed debt consultants do not have these powers:

[debt consultants] don’t have the power to stop a wage garnishment [for example] but a licensed insolvency trustee does.

The Office of the Superintendent of Bankruptcy provides a regulatory framework that oversees trustees.

Everyone is subject to the same rules, responsibilities, it’s equitable and it’s supposed to be transparent

For example, an LIT can, but usually does not charge up front fees for a consultation. That is because by law any fees they would charge up front would have to be rolled into the payments you would make if you filed anyway. Not so with unlicensed debt consultants. Consultants charge fees up front then refer you to a trustee to file. You don’t get those fees back or have them applied to the cost of your bankruptcy once you do file.

By including the term licensed in our name, the government is making it clear to the public who can legitimately provide insolvency services under the Bankruptcy & Insolvency Act.

So why did the government remove the term bankruptcy and return to the use of the word insolvency when referring to trustees? As Ted explains bankruptcy often has a bad reputation:

Not everyone knows what bankruptcy is but they’re pretty sure that it’s not a good thing. I don’t believe that statement is correct but it does have the negative connotations.

Insolvency is potentially a better term to explain the fact that trustees can offer more than a bankruptcy as a form of debt relief. An individual looking to eliminate their debt can talk to a licensed insolvency trustee about two insolvency services to eliminate debt:

Ted explains that a trustee is like a referee in a hockey game.

we’re the fellows that make sure both sides, so the individual that’s in trouble, plus the creditors, play by the rules and that everyone works in a fair and equitable manner.

That’s why a Licensed Insolvency Trustee will explain how the bankruptcy process works and what the implications of each option will be for you before you sign any paperwork.

To become a Licensed Insolvency Trustee requires that an individual:

successfully complete a series of courses about the technical aspects of bankruptcy and insolvency;

be employed for a period of time with a practicing Licensed Insolvency Trustee in order to gain practical experience;

pass both a written and oral examination

This process is very rigorous and in fact only one in four candidates succeed.

It may take time before the average consumer understands the term insolvency and the new designation, however regardless of the name, the bankruptcy process is well maintained and the public protected through the licensing and monitoring process of the Office of the Superintendent of Bankruptcy.

You can learn more by listening to the podcast or reading the transcript below.

On April 1st, 2016 the federal government is changing the rules and the term bankruptcy trustee will no longer exist. That’s right, in few short days bankruptcy trustees will no longer exist. So, is this an April Fool’s joke? No, this is the truth.

The first bankruptcy legislation in Canada came into force in 1869 it was called An Act Respecting Insolvency but it only applied to businesses. In 1880 the act was repealed and it was left for the provinces to deal with. Then in 1919 the federal government got back into the bankruptcy legislation business passing the Bankruptcy Act of 1919 and it covered both companies and individuals. The trustee was appointed by the government under that act. The act was amended again in 1932 and the Office of the Superintendent of Bankruptcy was created with the power to grant licenses to bankruptcy trustees. So, the bankruptcy act has existed in Canada for 97 years and the federal government has granted licenses to bankruptcy trustees for 84 years.

So, why now on April Fool’s day, 2016 is the federal government doing away with bankruptcy trustees? To find out please help me in welcoming back to the show my typical guest on the last show of the month Ted Michalos, my Hoyes Michalos co-founder and business partner. Ted, how are you doing today?

Ted Michalos: Not bad. My children will tell you I was around in 1869 when that first legislation was passed and was there voting for it.

Doug Hoyes: There you go, two years after federation is when it all began. Well, I think it’s kind of interesting that we went without federal bankruptcy legislation there for a couple of decades in between the different legislations.

So, let’s go through this step by step then. So, Ted you and I and every trustee in Canada are regulated and licensed by the federal government.

Ted Michalos: That’s correct.

Doug Hoyes: We’ve been known as trustees in bankruptcy or bankruptcy trustees for 85 years when the Office of the Superintendent of Bankruptcy was created. So, first question what is the Office of the Superintendent of Bankruptcy?

Ted Michalos: So, it’s a government agency that licenses, monitors and controls the insolvency community in Canada. So, it’s directly responsible for reviewing the legislation and making recommendations to Parliament for training, well not necessarily training, but definitely licensing and authorizing people to administer bankruptcies on behalf of the Canadian public. That’s a pretty important distinction. Lawyers don’t handle bankruptcy work in Canada, only licensed trustees do. Although on April 1st I guess that’s not the case anymore either.

Doug Hoyes: Well and we’ll talk about the new title. So, give me some examples of policies and procedures that are set by the Office of the Superintendent of Bankruptcy?

Ted Michalos: Well, probably the one that impacts people the most is every year the federal government establishes a threshold for how much income they think families of different sizes need to have a reasonable standard of living in Canada. It’s called the Surplus Income Guideline, it’s directive 12R if there’s anybody out there that really wants to read into this. But that’s the thing that says I think a family of two needs $2,500 a month to live on the entire cost of bankruptcy is based on these government guidelines so it’s a pretty important number.

Doug Hoyes: And that obviously gets updated and there are other directives that get changed as well. And in fact the Office of the Superintendent of Bankruptcy has issued a new directive, directive number 33 for people who are scoring at home. And that’s the one that where this new name comes into effect on April 1st, 2016. It’s changing our name from bankruptcy trustees to licensing insolvency trustees, which I guess in a way is kind of a throwback ’cause like I said in 1869 the first legislation was called an act respecting insolvency. So, we’re kind of going back to the old word as opposed to the bankruptcy word. But Ted, tell me why do think the government has made this change from bankruptcy trustee to licensed insolvency trustee?

Ted Michalos: Well, my suspicion is that the government was rather indifferent, that this is something that members of our industry, members of our profession have petitioned them to do. There’s really two branches of insolvency work in Canada. There’s those of us that deal with individuals, families, households, trying to help people get relief from their debts. And then there’s trustees or licensed insolvency trustees that deal with corporations and businesses. And they’re distinctly different entities, but from a marketing standpoint I think the corporate trustee community was looking for a different name.

Doug Hoyes: And because there is a negative connotation to the word bankruptcy?

Ted Michalos: That’s the reason they got support from some of the fellows who practice with individuals. Not everyone knows what bankruptcy is but they’re pretty sure that it’s not a good thing. I don’t believe that statement is correct but it does have the negative connotations that you were saying. And so, by changing the name to something that sounds much more technical, licensing insolvency trustee, you’ve removed that term that has those negative connotations. Whether or not that’s actually good for the public, I’m not certain.

Doug Hoyes: So, let’s break it down then and see if we can analyze and figure out whether it’s good or not. So, the word licensed is a new thing. It used to be called bankruptcy trustees now it’s licensed insolvency trustees. What does that mean? What does license mean? Who gives a license? What’s the process? Tell me about that.

Ted Michalos: Well, effectively by telling someone that you’re licensed you’re saying that someone has set up a regulatory framework. There’s someone responsible for overseeing the things that you do. And so, I guess the implication is by not telling people we were licensed, so that it was less clear that we’re reporting to a higher authority. So, a bankruptcy trustee by definition had to be licensed by the federal government but the public may not have known that. So, now we’re explicitly saying yes, we are licensed, which differentiates us from the people that are not licensed. And unfortunately there are an awful lot of people praying on the public that aren’t licensed these days.

Doug Hoyes: So, how hard it is to get licensed, what’s the process?

Ted Michalos: Well, if you ask any of our students they’ll tell you it’s near impossible. There’s a series of courses that you have to take. You have to be employed by a trustee, so think of it like articling, the same way that students that want to become lawyers or doctors that want to, what’s the term for doctors that are – residency, right? You have to be practicing with someone that oversees your work to get you to the point where you can sit in an examination and convince the licensing body that you are qualified and competent.

Doug Hoyes: And so, there are two in effect year long courses. We’re kind of over simplifying the process. It finishes with a final written exam where you have to be both examined ons corporate and personal bankruptcy and insolvency technical issues, tax issues and so on. And then the final piece of the puzzle, the final piece of the exam is called the oral exam.

It’s called the oral board and I happen to be quite familiar with it ’cause I’ve been on the board for the last three years as an examiner. It’s a hour and a half long exam where you are given half an hour to read the questions and then you sit in a room with three other people, the trustee, representative of the government and an insolvency lawyer. And you’ve got an hour to answer all the questions. That’s a pretty intimidating process for a lot of people to go through having never done an oral exam before. But that show you how hard it is to become licensed. It’s not a simple thing.

Ted Michalos: And this is not a secret. The failure rate, the number of people that are not successful at this program is pretty significant. There’s a 50% failure rate at the written examination level and a 50% failure rate at that oral board. So, one out of four people that start the program might successfully get a license. It’s much more difficult than anybody realizes.

Doug Hoyes: Yeah and in fact the last two years, 2014 and 2015, the success rate on the final written exam was in the 30 some percent range so it has been considerably less than 50%. So, it’s a very difficult thing to become licensed. So, why should the public care about that? So, great you’ve gone through all this training to become licensed but hey all we’re talking about is debt here, why can’t I just go see anybody else on the street? Why is this license thing so important?

Ted Michalos: Well, there’s more to just dealing with this debt than just saying, you know, I’m just not going to pay people back. The system is designed to be fair to the individual; it’s designed to be fair to the people that you owe money to. And by fair I mean the government sets standards that we all have to follow. It’s not a question of you going to the cleverest guy on the block or a lawyer that knows somebody; he knows a guy and he can get you a deal. Everyone is subject to the same rules, responsibilities, it’s equitable and it’s supposed to be transparent. One of the problems we’ve had in the past is there’s a whole new industry that cropped up about seven or eight years ago they call themselves debt consultants. And I’m not going to get off on this too badly ’cause you know it pushes my buttons.

Doug Hoyes: That’s why I asked.

Ted Michalos: But these people aren’t licensed by anybody, they aren’t regulated. And they’ve been preying on the public. And what they do is they run advertisement saying we can help you reduce your debts, avoid bankruptcy, we’re not a trustee, ’cause they’re not. You go to them, you pay them a fee and then they have to refer you to a trustee to actually deal with the problem.

Doug Hoyes: And so, is that one of the reasons then that the government has changed the name to take the word bankruptcy out of it? You’ve got all these guys out there saying don’t go bankrupt, we’re not bankruptcy, guys, bankruptcy, bankruptcy, bankruptcy, we’re not that, come see us. When really all it is, is a ruse. They’re getting you in the door and they can’t actually solve your problem. They cannot legally do a consumer proposal for example

Ted Michalos: That’s right.

Doug Hoyes: Unless they’re licensed. So, is that what’s really driving this name change to get that bankruptcy out of there that has been scaring people?

Ted Michalos: I think that’s defiantly one of the arguments that was advanced. That you want to get bankruptcy out to try and level the playing field with all these debt consultants.

Doug Hoyes: Well and in fact I guess it’s a negative thing to be called a bankruptcy guy. These guys are able to use it as a marketing advantage to say they weren’t that, when in fact no, it’s actually a positive thing. And I guess that’s where the word licensed comes in now, that you have to have a license to be able to do this. So, what are the services then that a licensed insolvency trustee can provide that one of these unlicensed debt consultants can’t provide?

Ted Michalos: Well, first and foremost the only folks that can perform some sort of legal insolvency service for you are license insolvency trustees. And there really are two big classes of work. There’s something called a proposal to creditors, which is a program where you offer to repay a portion of what you owe or there’s an actual bankruptcy filing. And they’re very complicated rules for both of them but the concept is simple enough. You need relief from your debts. And then depending on your circumstances are you able to repay a portion, which would make the proposal more attractive or do you need complete relief, there is no ability to repay, in which case you’d be looking at bankruptcy.

Doug Hoyes: Well, see I’ve talked to these debt consultant guys and they say look it’s not that complicated. You owe a bunch of money on credit cards, here’s what we’re going to do, we’re going to phone the credit card company up and say we’re offering you 30 cents on the dollar, that’s it, that’s the deal. You don’t need some fancy high falutin guy who’s gone to school and has all these courses and done all this licensing thing, it ain’t that difficult.

Ted Michalos: Unfortunately let’s say you owe five or six different people and so somebody offers to do this for you. That would be a debt settlement company, don’t get me going on them. You call the first fellow and you say I’ll give you 30 cents on the dollar and let’s say he says yes. Call the next guy and he says no. You call the next guy and he says no, I’ll take 50 cents. You call the next guy and he says nah, I’m going to garnishee your wages ’cause I want to get paid ’cause now you told me that you’re broke.

The idea behind a consumer proposal is provide a structure, framework, something that provides the individual with legal protection so people can’t try and garnishee your wages, they can’t freeze your bank account, they can’t take advantage of you when they know you’re in trouble and it provides you with a simplified solution. You’re going to make one monthly payment to one place. There won’t be any interest on your debt. It’s going to deal with the problem to everyone’s advantage. That’s what the real purpose of the act is.

Doug Hoyes: Well, I guess that phrase legal protection is really the whole key to it.

Ted Michalos: That’s right.

Doug Hoyes: You can’t be offering legal protection unless you’ve got some legal background to do that. Does the – so, when I think of the word legal I think of the word court. So, does the court system come into any of this at anytime?

Ted Michalos: It’s interesting, bankruptcy – license insolvency trustees, I’m going to keep using the wrong term for the next three years – are officers of the court. I used to tell people to think of us like junior judges. I mean we don’t have that kind of power but the license means we can administer consumer proposals and bankruptcies as representatives of the court. And the court only comes into play when there’s some complicating issue.

Let me give you an example. Let’s say a young man went out and borrowed $20,000 to buy a pickup truck. And of course he didn’t use the $20,000 to buy a pickup truck; he used it at casinos, which unfortunately is happening more and more often. Well, he files bankruptcy, he wants relief from his debt, he tells the court well, I can’t pay these bills. The creditor says, well I loaned him money for the pickup truck, where’s my pickup truck? Well, that would be a complicating matter that probably a judge would want to look at. And they would have to decide well, was this fellow honest? Did he really do what he said he was going to do when he borrowed money? Or was he less than honest and maybe we have to look at some penalties?

Doug Hoyes: Well, I think an even more common example of a legal issue would be what you said earlier, where you didn’t pay someone, they took you to court and started garnishing your wages.

Ted Michalos: That’s certainly simpler to understand.

Doug Hoyes: So, these guys that are advertising they can settle your debts, just come and see us, they don’t have the power to stop a wage garnishment but a licensed insolvency trustee does. Why? How does that work?

Ted Michalos: Well, so the law specifically says and this is the Bankruptcy and Insolvency Act, that when you file a consumer proposal or you file an assignment and bankruptcy, there’s a provision called an automatic stay of proceedings. So, it’s not that you have to apply to the court for protection; you’re automatically entitled to this protection as part of the law. And the reason they do that is to make sure that all of the people you owe money to are treated the same way and that you are treated fairly. Obviously if somebody’s gone to court and they’re taking 20% of your paycheque, you’re not in a position where you can deal with all the other people that you owe. So, we put a stop to that wage garnishee and everyone gets treated the same way.

Doug Hoyes: And only a licensed trustee can do that. So, a licensed insolvency trustee, there you got me saying the wrong terms too.

Ted Michalos: That’s right; we’re going to change your name later.

Doug Hoyes: That’s right. So, who does a licensed insolvency trustee work for? So, they go to hoyes.com, they hear our ads on the radio or they go to some other licensed insolvency trustee and they say yeah we need to do a proposal can you help me? We say yeah, sure. Are they hiring us?

Ted Michalos: No, so it’s much more complicated than that. The way to think of a licensed insolvency trustee, literally the reason I used that junior judge analogy is it’s a pretty safe one. Think of us as a referee in a hockey game. So, we’re the fellows that make sure both sides, so the individual that’s in trouble, plus the creditors, play by the rules and that everyone works in a fair and equitable manner.

I’m trying to think of a good way to describe this that doesn’t step on toes anywhere, well, maybe there isn’t. So, it’s complicated because you go to the trustee’s office and you’re looking for help. But legally we’re actually appointed by the Office of the Superintendent, their employees which are known as official receivers. And so, our duty is to apply the law fairly and to see that everyone complies with their duties and responsibilities. Most of the people that owe money and more importantly the creditors so they stop lawsuits, they stop wage garnishes, they stop all that sort of stuff.

Doug Hoyes: And that’s why we’re completely up front with people when they come in. We say okay here’s the deal. You eluded to earlier this concept of surplus income in a bankruptcy. Where the more money you make the more you’ve got to pay. Okay, before you sign any paperwork with us, we’re going to explain how that process works. Here’s how all the math works, here’s what the implications of it are. We’re going to go through all the different issues with you.

So, we are certainly doing our best to help you through the process, to explain everything so there are no surprises but what we are doing is explaining the rules so that you can then know what all those rule are that you have to follow.

Now a lot of people say wait a minute, it really sounds like who you’re really working for is the creditors, the people I owe money to because in the proposal or the bankruptcy you’re going to collect money from me and give it to them. If you’re giving money to them you must be working for them not to me. And that’s what these debt consultants are always saying. Oh, you don’t want to go see a licensed insolvency trustee because they work for the creditors, they’re collecting money for the creditors. Is that true? What do you say?

Ted Michalos: Well and so, again you’re right. That’s the argument thatthe other side makes, the people that, sorry the debt consultants. And you can see why they say that but quite frankly, the truth is, we work for ourselves. It’s the trustee’s responsibility, we’re independent businessmen. So, we’ve got to try and secure clients to provide our services to. The same way a lawyer would or a doctor or a dentist. And we’ve got to maintain a reputation in the community, particularly in the insolvency community so that the creditors will allow us to deal with people. Creditors have the right to call a meeting and replace a trustee if they don’t find them trustworthy.

Doug Hoyes: Yeah, so our reputation and any other licensed insolvency trustee’s reputation is very important because we have to – if we’re the referee in the hockey game we’ve got to get both sides on the same page. So, I’ve got to come up with a solution that’s going to work for you but it also has to be acceptable to the creditors. And unfortunately in my experience with the debt consultants they don’t really care about what the bank is going to say because the bank doesn’t even know their name. They’ve sent the person to see a trustee and if it doesn’t work, oh well the trustee looks bad. In our case we want to make sure that everyone’s on the same page with it, that’s pretty key.

Ted Michalos: Well and we kind of missed something here, one of the requirements of the law, so a licensed insolvency trustee is required to review all of your options with you. So, a debt consultant’s trying to sell you something, in nine cases out of 10 they’re trying to sell you a proposal to creditors, they just don’t call it that. Half the people that come and talk to a licensed insolvency trustee don’t actually file an insolvency engagement. So, they don’t follow a proposal or bankruptcy. What they needed was somebody to help them assess their financial situation and give them honest answers about options and alternatives. What can I do to get out of debt? And quite frankly more than half the time the solution isn’t to file bankruptcy or to file a consumer proposal, it’s to take a look at some of the other things that they can do.

Doug Hoyes: Like refinancing their house, getting your taxes filed to get up to date on that, cutting some expenses.

Ted Michalos: Just becoming more disciplined with your finances. I mean no one’s really taught how to balance a cheque book anymore. Nobody’s taught to look at what they’re paying for things. You want to know what your monthly payment is but not everybody takes the time to figure out how much interest are you paying because you’re buying this thing over three or four or five years or worst you’re putting it on your credit card. A trustee’s going to look at all of the things before they suggest to you these are the solutions that would make the most sense to your family and then you make the decision yourself based on good information.

Doug Hoyes: So, final question for you, what is the cost upfront to meet with a licensed insolvency trustee?

Ted Michalos: There shouldn’t be any cost whatsoever. I mean the law allows licensed insolvency trustee to charge a fee for people to come in and have a consultation. But I’m not aware of any licensed insolvency trustee that does it. In fact if you’re sitting down with somebody and the first thing they say after talking to you for 15 minutes is you know what? You need to sign his piece of paper and write a cheque for $250 before we can do anymore work, you’re sitting in the wrong office.

Doug Hoyes: Yes because even though the law allows a licensed trustee to start charging upfront, if they do those fees have to be rolled into the eventual procedure anyway.

Ted Michalos: That’s right so they apply to your bankruptcy or your proposal.

Doug Hoyes: They apply to your bankruptcy or your proposal, which means really there’s not a whole lot of point in a trustee charging you anything up front. It’s all going to get rolled in. So, I think that’s I guess the final key point to remember here. A licensed insolvency trustee is licensed by the federal government and they aren’t charging upfront fees. And those are two things you can look for. If someone’s offering to help you and they aren’t licensed and they’re looking for upfront money they’re probably not the people you want to be dealing with.

Ted Michalos: Yeah the first question you should always ask is are you a licensed insolvency trustee or are you simply going to refer me to one to solve my problems? And if they are, why are you going to pay this person any money at all? But that’s a whole different show.

Doug Hoyes: I totally agree and I will put a link in the show notes to all of this information so if you’re trying to figure out if the person you’re dealing with is a licensed insolvency trustee all the names are listed on the government’s website. So, it’s easy enough to do a search.

Great, thanks very much Ted for that. I’m going to take a quick break and then I will be back with the next segment. You’re listening to Debt Free in 30.

It’s time for the Let’s Get Started segment here on Debt Free in 30. As Ted and I discussed in the first segment on April 1st, 2016 the rules are changing and the term bankruptcy trustee will no longer exist. To understand how long the word bankruptcy has existed let’s review some history.

One of the earliest mentions of a process for settling debts is contained in the code of Hammurabi, which as I’m sure you know is written by King Hammurabi who ruled Babylon from 1792 to 1750 B.C. That’s over 3,700 years ago. In Hammurabi’s code of laws he says if anyone fails to meet a claim for debt and sell himself, his wife, his son and daughter for money or give them away for forced labour, they shall work for three years in the house of the man who bought them or the proprietor and in the fourth year they shall be set free.

In other words if you incurred debt you and your family could become slaves for up to three years to repay the debt. Ancient Greece had a similar approach but by the seventh century B.C the wealthy people in and around Athens had so many poor people in bondage that economic collapse and rebellion appeared likely. So, the lawmakers granted amnesty to many of those in bondage and outlawed using a person’s freedom as collateral for a debt. Julius Caesar a few hundred years later enacted laws against extreme interest rates. And he enacted laws of bankruptcy that are not that different to what we have today.

Many people think bankruptcy is a modern concept but it isn’t. The word bankrupt is taken from the Italian word bankarupta, and my apologies to my Italian friends I’m sure I totally mispronounced that word. It means bench broken. There have always been bankers or what in biblical times were called money changers. If you went to the marketplace in Ancient Athens or the forum in Rome or the temple in old Jerusalem, the money changers would set up a table or a bench to serve their customers. If someone had currency from a foreign country ’cause there was a lot of travelling amongst countries and they all had different currencies, they could see a money changer to change it into the local currency.

Fast forward to the middle ages where the financial centre of the modern world were cities like Florence and Venus and the table or bench was known in Italian as banka, which is the source of our modern world bank. The money changers would exchange your money from one currency to another but these guys would sometimes take money from their wealthier clients and lend it others at a profit. They would charge what even today would be considered a very high rate of interest, think pay day loan interest.

As with all loans there’s a risk. Just like today the borrower might lose his property or even his life and be unable to repay the loan. If the lender has a few bad loans it would cause the failure of the banker, he would be unable to repay the people he borrowed from. And what would the creditors do if a banker couldn’t pay them back? In the middle ages the creditors may break his table or bench to show the world that he was no longer in business. His bench was broken, he was bankarupta. This expression made its way in the 16th and 17th centuries from Italy to England and over time the expression morphed into our current word, bankarupta has become bankrupt.

As I said in the opening the first bankruptcy in Canada came into force in 1869, it was called an act respecting insolvency but it only applied to businesses. In 1880 that act was repealed and it was left to the provinces to deal with. Then in 1919 the federal government got back into the bankruptcy legislation business passing the bankruptcy act of 1919 and it covered both companies and individuals. The trustee at the time was appointed by the government.

The bankruptcy act was amended in 1923 and the estate’s creditors were given the power to select a trustee. The act was amended again in 1932 and the Office of the Superintendent of bankruptcy was created with the power to grant licenses to bankruptcy trustees. A further amendment in 1950 created summary administration bankruptcies, which are the most common form of personal bankruptcies today and a proposal process was also created. In 1992 the name of the legislation was changed to the bankruptcy and insolvency act and consumer proposals were created. So, there’s the background on bankruptcy legislation in Canada.

So, why am I telling you all of this? Well I’m making the point that the word bankruptcy has existed for many hundreds of years and bankrupt trustees have been licensed by the federal government since 1932.

For over 80 years we’ve been called bankruptcy trustees but that’s about to change. On April 1st, 2016 the term bankruptcy trustee will no longer exist in Canada. The federal government is changing our name. And no, this is not an April fool’s joke, although you’ve got to hand it to the federal government for picking April Foot’s day as the day to introduce new rules. Affective April 1st, 2016 bankruptcy trustees in Canada licensed by the Office of the Superintendent of Bankruptcy, a division of the federal government will be known as licensed insolvency trustees.

I guess in a way it’s somewhat fitting because the first bankruptcy legislation in Canada in 1869 was called an act respecting insolvency so in a way we’re going back to our roots. Of course it will take the public a bit of time to get used to the word insolvency and stop thinking about bankruptcy, which is the word we’ve used in Canada for 97 years. Time will tell how long it will take to get used to the new term licensed insolvency trustees.

That’s the Let’s Get Started segment. I’ll be back with some final thoughts right here on Debt Free in 30.

Doug Hoyes: Welcome back, it’s time for the 30 second recap of what we discussed today. On today’s show Ted Michalos and I discussed the new term licensed insolvency trustee, which effective April 1st, 2016 replaces the old term bankruptcy trustee. That’s the 30 second recap of what we discussed today.

So, what’s my take on the new term? Well, I’ve got mixed feelings. On the one hand everyone knows what the term bankruptcy means because we’ve been using that term in Canada for 97 years. The average guy on the street has no idea what the term insolvency means so, it will take a period of time for the public to become familiar with the new designation. I am however pleased that the word licensed is part of the new name because that’s an important distinguishing feature between licensed insolvency trustees and unlicensed debt consultants.

That’s our show for today. Full details on these new rules are available on our website at hoyes.com. Thanks for listening, until next week I’m Doug Hoyes and that was Debt Free in 30.

There are a number of personal finance personalities, especially on American radio and TV, who say that if you have too much debt it’s because you spent too much and you’re the cause. After all, if your actions aren’t to blame, then they can’t sell you their solutions and books.

But is that opinion valid? Are all of our financial problems entirely our fault, or are there other factors that lead to debt problems?

While we should bear some personal responsibility for our actions, there are also circumstances that are beyond our control that lead to debt problems. Yes we should prepare for those circumstances with thing like emergency funds but sometimes, even if you do everything right, stuff happens and you end up deeply in debt. Rather than placing blame it’s better to learn from the situation and take corrective steps to repair your future, rather than focus on the past.

Aggressive and sophisticated marketing ‘sell’ debt as good

Big banks and lending institutions have big marketing budgets. One of the most aggressive, and often effective, market activity is direct solicitation. Financial institutions of all types send preapproved credit applications in the mail. Your current lender may notify you that they have automatically increased your credit limit without you even asking. Walk into almost any major store and there is likely a friendly person at the front asking if you want to apply for their credit card in exchange for a free gift. These are all common tactics, and can be difficult to resist.

Payday loan companies don’t advertise up front that their loan carries an interest rate of 548% – they say it’s $21 per $100 borrowed because that sounds better. Couple this with a convenient and friendly in-store experience and you can see why payday loans are so popular.

All of this means we have easy access to credit. And as Kelley Keehn explained:

not just access, easy access. And cheap money … instead of saying I can’t afford that, they look at well, you know my line of credit, if I just service it with that interest … They’re looking at servicing a line of credit. Not getting out of debt.

Kelley also talks about how peer pressure to spend adds to our tendency to take on this credit and minimum payments make us think we can afford it.

Job loss or underemployment make it hard to pay off debt

More than half of all of the bankruptcies and consumer proposals filed in Canada are caused primarily be a reduction in income, and in many cases that’s caused by job loss. If you lose your job it is often inevitable it’s hard to keep up with existing debt payments and worse, you may use debt to survive until you find another job.

Illness and time off work create more debt

Illness, injury, and health related problems are another primary cause of bankruptcy in Canada despite our public healthcare system. If you have a full health plan at work you may be able to afford your medications, but it is often the time off work, with reduced or no pay, that causes people to resort to debt to survive.

Divorce can lead to problems repaying joint debt

One in five insolvencies in Canada are caused, at least in part, by a relationship breakdown, separation or divorce. More than a quarter of people filing bankruptcy are divorced or separated at the time they file.

We can debate whether or not it’s your fault that you got divorced, but separation definitely comes with financial costs that can lead to more debt:

you are no longer sharing expenses including your home and car;

living costs double on roughly the same combined income;

you incur extra costs to move, perhaps sell a home;

legal costs can add to debt, particularly if children are involved; and

joint debt can create a problem when both spouses no longer live together.

Could you survive a separation tomorrow? Do you have sufficient resources to start a new life? Many people don’t, and it’s not their fault.

Student loans are getting harder to repay

More than one in ten (13%) people who filed insolvency in Canada had student loan debt.

The cost of getting a higher education for most young people today is massive student debt. It’s almost impossible for a student to earn enough money during the summer or with a part time job to cover tuition, residence, books and all the other costs of going to school. Is that student debt your fault?

The takeaway from today’s show is that yes we need to each be responsible for our debt and money choices however sometimes events happen that are on your control and can lead to financial problems. In those situations, rather than laying blame, look for a solution for a future. In other words:

Don’t find faults. Find fixes. If you have a lot of debt, review your options to get out of debt. Look forward to tomorrow, not backwards to yesterday.

FULL TRANSCRIPT show #80 with Robert Brown and Kelly Keehn

Today on Debt Free in 30 I want to discuss a simple question, ‘Whose fault is it?’ That’s the question, whose fault is it if you’re in debt? There are a number of personal finance experts, many of whom are American and have their own radio or televisions shows and they write lots of books that say if you have too much debt it’s because you spent too much. If you can’t find a good job it’s because you aren’t looking hard enough. If you don’t retire by age 50, it’s because you didn’t save enough and invest wisely.

Now I question their opinions because obviously they make their money by selling books and DVDs and webinars and courses to tell you how to get out of debt and manage your money. So, if they can convince you that it’s your fault, they can sell you their solution. If it’s not your fault well then they can’t sell you anything.

In my experience, our Canadian personal finance experts are somewhat more realistic. They understand that into each life some rain must fall and sometimes stuff happens that’s beyond our control. A few weeks ago I had Robert Brown as a guest on this show, he’s the author of Wealthing like Rabbits, which is a great book that is an unconventional look at personal finance. So, I wanted to hear his opinion so I asked him, is it my fault if circumstances come up and bite me?

Robert Brown: Sure, I think it’s largely circumstantial and situational. There may be times when somebody’s taken on a awful lot of debt for irresponsible decisions and if we need to place blame that person needs to look in the mirror and accept some for himself. But it’s also true that sometimes life will come up and bite you in the butt if you will. You could lose your job or you could be faced with a large bill because your car blew up that you weren’t expecting. And personal finance types like me can talk about emergency funds and all those sort of things but life sometimes happens and it’s not always your fault. I think a better lesson is rather than placing blame is looking where responsibility lies and the even larger lesson is learning when these things happen and then taking steps to make sure that they don’t happen again.

Doug Hoyes: ‘Cause I know that in my business we’re very busy in January, February March, April as people get all their Christmas bills, holiday bills start coming in. And there’s a bit of a spike in our business at that time. And I always say to myself well, okay people we always know when Christmas is going to be. You tell me any year a thousand years in the future and I can tell you what date it’s going to be, December 25th. And if you always go out for your birthday well, tell me what your birthday is and I’ll tell you what your birthday’s going to be two years from now, it never changes it. You talked about a car blowing up; okay we’ve all had that happen.

Robert Brown: It probably wasn’t the best example.

Doug Hoyes: Well, but it was a good example because in my business a lot of people get into trouble. They tell me yeah everything was going goo and then the transmission died and I had to get another transmission. Well, you can predict that a car will need repairs. You can’t predict the exact date but if you have a 10 year old car at some point it’s going to need new tires, new breaks, new this, new that.

Robert Brown: You can plan for car maintenance, absolutely you can.

Doug Hoyes: So, is it my fault then when my car eventually does break down? Shouldn’t I have known about that in advance?

Robert Brown: Yeah, you know what? It’s a tough call but people need do I suppose a better job of planning for life, that’s why I come back to personal finance types like me will talk about having emergency funds set aside for when that type of thing happens. And, you know, when we look at all the sorts of stuff that are happening in the economy today, there are some people going through some tough times and there’s some jobs being lost. And I am completely empathetic to those situations.

But in my back of my personal finance mind I’m always asking myself, okay it wasn’t, you know, we don’t have any control over the economy or the price of oil or any of those things, but we do have control to a large degree over our personal economies. And if you were to lose your job, you know, that’s never a good thing but it’s certainly better to lose your job with no debt and, I’m pulling this number out of my head, $10,000 in the bank, then it is to lose your job with $15,000 in credit card debt and no money in the bank. And those are things that we can learn from other people’s experiences or from our own experiences and set ourselves up for the future a little bit better.

Doug Hoyes: So, you’re saying I should control what I can.

Robert Brown: Yes.

Doug Hoyes: And I guess by extension not beat myself up for things I can’t control.

Robert Brown: Perfect.

Doug Hoyes: So, if my company shuts down and moves production overseas, well okay, maybe I should have worked harder but let’s face it there were 4,000 people in the plant, my working harder wouldn’t have changed the outcome, that’s what was going to happen.

Robert Brown: But you do have control over your personal economy for when that happens, whether or not you were in debt, how you managed your money up to that moment.

Doug Hoyes: And so, I guess stress testing your finances is not a bad idea then. So, if I was to lose my job then what would happen, how would that change my behaviour today? And I mean you’ve probably heard the same stories, I’ve heard about people in the oil patch in Alberta in 2013, 14, 15, they were driving big trucks and living in nice houses and that but they all had, well I shouldn’t say all, some of them had debt. And so, when the inevitable happened and the oil price dropped, well if you have no debt okay well I guess it’s going to hurt, I’m going to have to find another job, maybe I’m going to have to move out of Alberta.

Robert Brown: But it won’t hurt as much as for somebody who has a big credit card debt and a big truck loan they need to pay off.

Doug Hoyes: Absolutely. So, you’ve got to look ahead and see what’s coming and control what you can and don’t beat yourself up over the rest, excellent.

Robert Brown: Plan for the worst, and how’s that go? Plan for the worse and expect the best.

Doug Hoyes: Hope for the best, yeah something like that. So, that’s a good way to end the segment, Robert thanks very much for being here.

Robert Brown: Thanks for having me Doug.

Doug Hoyes: So, Robert touched on a number of different concepts. He agrees there are a number of circumstances outside of our control, if you can’t control if you can’t control it, it’s as simple as that. But what Robert also said is that while we can’t control the economy, we have some control over our personal economy. We don’t know when our car will need repairs, but since no car will last forever we can plan for the inevitable repairs. So, what’s the answer to the question, whose fault is it? It would appear that in some cases we have some control over our fate and in other cases circumstances are beyond our control.

So, let’s ask another expert for their opinion.

I’m joined by Kelly Keehn who was on the show awhile back talking about identity theft and fraud. I want to ask you a different question though Kelly, and that is is my financial problems my fault? And I understand that at the basic level, yes I spent the money that’s what created the debt, so yes, on some level it’s my fault. But there are also forces at work here. Is it 100% my fault? Are there other things that factor into it when you think about is it my fault that I’m in the situation I’m in?

Kelly Keehn: Yeah, there’s certainly a number of different factors. But one that I don’t think a lot of us think about is, 20 years ago I used to hear my friends say and peers and co-workers and things of that sort say I can’t afford that. Now they were doing a quick calculation in their head, you know, based on my mortgage payment and put something in RSP and saving for the kids, yeah, no, I can’t afford that right now. So, it wasn’t that they truly couldn’t but their calculation was that they couldn’t afford it.

20 years fast forward, I don’t hear anyone ever, any income level, as a personal finance educator, people will write me for help and then when I offer it or give them a free call, they’re on a vacation in Hawaii or Mexico and they’ll get back to me in a couple of weeks. No, the expectation is you have to have two cars, you have to buy a home, you have to put your kids in this and all of that. And no one stands back and says I can’t afford it. So, when you have that kind of adult peer pressure to be the one to stand back and say to your kids we can’t afford that, to say to your friends, I can’t afford that, it’s just not even in our vernacular. So, I think that’s one of those that have absolutely has influenced us over the last number of decades.

Doug Hoyes: Yeah, I mean if everybody you know in your community wears a blue shirt and you tell your kids no, you have to wear a green shirt, I’m totally different, I’m totally different than anyone else.

Kelly Keehn: Exactly.

Doug Hoyes: And so, it’s a budgetary question then. In the past we would look at our budget in our head if not on a piece paper and say no, I can’t afford that because that will mean I won’t have the money to put in my RSP to save for my kid’s education, whatever. And now we don’t even think of that because we have access to credit?

Kelly Keehn: Well, not just access, easy access. And cheap money as people tell me. So one of the first principles of economics is ‘incentives drives behaviour’. So, I was the host of a show a number of years ago called Burn My Mortgage that’s re-running right now on OWN actually. And I got to tell you I’m 40 right now, I think I was 35 when it ran I had never heard of a mortgage burning party. It was not –

Doug Hoyes: Not even a thing.

Kelly Keehn: Not even a thing. It’s not anything anyone’s talking about. Actually my generation and younger generations are like well just debt is what it is. And people, instead of saying I can’t afford that, they look at well, you know my line of credit, if I just service it with that interest that’s like $75 a month, sure we can do the kitchen renovation with the marble and everything. Yeah, you bet. They’re looking at servicing a line of credit. Not like getting out of debt, paying for your kids education, do, do, do, do. So, it’s like –

Doug Hoyes: So, today afford it means I can make the minimum payments.

Kelly Keehn: I think for a lot of people it does.

Doug Hoyes: So long as interest rates stay close to zero then –

Kelly Keehn: And you have your job and your spouse has his job.

Doug Hoyes: Everything’s perfect.

Kelly Keehn: Right.

Doug Hoyes: So, to a certain extent it’s not our fault because we’ve all got sucked into this mentality that yeah, I can get everything because credit is easy, I can get at it and that’s what outs there. Well, that’s an excellent answer and I think that’s a good thinking point for all of us that when we look at whether I’m responsible or not for something it’s not just the banks that are pushing me that’s how they make money, but also my peers are pushing me. I’ve got to look at both factors.

Kelly Keehn: Exactly. It might not be your fault but with your new awareness it’s within your control to change so be empowered with that.

Doug Hoyes: And make sure you understand it. Excellent, that’s a great answer. Thanks very much Kelley.

Kelly made some great points. She said that incentives drive behaviour so when interest rates are low it drives us to borrow more than we would borrow if interest rates were higher. You can see that quiet clearly in the housing market. When the federal government wants to stimulate the economy they lower interest rates so we can all afford to buy an even bigger house. Low interest rates lead to lower mortgage payments so I can qualify for a higher mortgage so we buy more expensive houses, which just drives house prices up. So, is that my fault?

Kelly also made a great point about our perceptions. 20 years ago if I said I can’t afford it, it meant I don’t want to use up too much of my budget by buying that thing. Today in this era of low interest rates and easy credit, afford it means I can make the minimum payments. That’s a totally different definition of afford it.

We live in a time of historically low interest rates. Government guaranteed mortgages, which encourage us to borrow and easy credit. So, we borrow and that sometimes lead to trouble. Are low interest rates and easy credit our fault? Kelly’s right, it might not be your fault but it’s within your power to decide whether or not you take out that bigger mortgage. But it takes a lot of discipline to not borrow when it seems like everyone else around you is borrowing like crazy.

So, we’ve heard from two experts and they both offered a similar opinion. Sometimes circumstances are beyond our control so it’s not our fault if we get into trouble. But we also should be aware of what can go wrong and we should take steps to prepare for possible problems. So, what can go wrong?

Well, based on a review of all the people I’ve helped with debt problems over the years, I can easily list five common reasons why your debt problems are not entirely your fault. Number one, aggressive and sophisticated marketing. All you got to do is a do a quick review of all the big banks financial statements and you can see that each year they spend many hundreds of millions of dollars on marketing, what they call communications. And that’s television and radio commercials, internet ad advertising but of course that’s not the most difficult advertising to resist. You can always change the channel or hit the mute button.

The most insidious form of advertising is direct solicitation. Have you ever received a pre-approved credit card in the mail? Has your credit card company ever sent you a letter saying congratulations, you didn’t ask for it but we raised your credit limit. Have you ever walked into a store and the friendly person at the front says hey if you apply for our credit card today you get a free gift? These are all common tactics and they’re very difficult to resist.

Payday loan companies, we’ve talked about them many times on this show and they are very sophisticated. They don’t tell you our annual interest is over 500% so you may never be able to pay us off. No, instead they’re only going to tell you things like it only costs $21 to borrow $100. That doesn’t sound like much but if you do the math, borrowing $21 on, oh sorry, paying $21, on a $100 loan every two weeks works out to $548% interest on an annual basis each year. It’s hard to resist these sophisticated marketing tactics and that’s why if you do succumb to the temptation, it’s not entirely your fault.

The second cause of a lot of financial problems is job loss or under employment. More than half of all of the bankruptcies and consumer proposals filed in Canada are caused primarily by a reduction in income and in many cases that’s caused by job loss. Is it your fault that your company moved operations to Mexico or China? Probably not. An equally common scenario is underemployment, many companies offer full-time permanent employees medical benefits and a retirement plan. That’s expensive so companies today may hire a couple of part-time employees instead of one full-time employee.

The savings are significant for the company but of course the cost to the employee is potentially huge. Many employees must have two or more part-time jobs just to make ends meet and they have to juggle their shifts to pick up enough hours just to survive. If they get sick, forget it, there’s no benefits and they incur the costs. Is it their fault that they have to use debt to survive?

Temporary jobs are another big risk factor for employees. To hire a full-time employee, an employer has to interview multiple candidates, pick the best one, set them up on payroll and then if they’re not suitable for the job they terminate them and incur the cost of severance, and incur the cost to hire a replacement employee. That’s why more and more employers today are using temp agencies for clerical or manufacturing or service industry employees. They’ve got an unlimited supply of employees and if they don’t work out they can terminate them with no cost and get another one tomorrow. No severance and no benefits. I know of one large employer where the majority of the work force is temporary employees on short-term contracts. I’ve met with many employees at that company who’ve worked at that company off and on for seven years. But they’re still contract employees with no benefits. They go through periods of unemployment until the next contract starts and they use debt to survive. Is it their fault that they can’t find a full-time permanent job with benefits?

Number three, number three cause of financial problems, illness. What would happen if you were in a car accident or got injured at work or found out you had cancer and required six months off for radiation and chemotherapy? Do you have enough money in the bank that you could pay your rent or mortgage and food and prescriptions and all of your other living costs for the six months that you’ll be off work? Most people don’t have six months of cash just sitting there, so a medical problem can be financially ruinous. So, is it your fault if you get cancer?

Number four, divorce. Based on our statistics one in five insolvencies in Canada are caused, at least in part, by a relationship breakdown or separation or divorce. More than a quarter of people filing bankruptcy are divorced or separated at the time they file. Now we can debate whether or not you get divorced but there is no debate over the financial implications of a relationship breakup. When you’re together you have one expense each month for rent, hydro, gas, cable and home phone. You may even be able to share a car. It’s not quite true that two can live as cheaply as one but it’s pretty close. When you separate you are each now paying rent and all your other living expenses. Your living costs can double but unfortunately you now only have one income and of course that’s a recipe for financial problems. Lower income, higher expenses.

In many cases the actual separation itself is also very expensive. You incur costs to move and you need first and last month’s rent and a security deposit for your utilities. If you don’t have the cash on hand you borrow to start your new life. If a legal separation is required lawyers may be involved, if children are involved the lawyers bills can be significant and that leads to more borrowing. Could you survive a separation tomorrow? Do you have sufficient resources to start a new life? Many people don’t and it’s not their fault.

Reason number five, student loans. More than 13% of all insolvent debtors in Canada had a student loan at the time they filed for bankruptcy or a consumer proposal. And 13% is actually a pretty big number because in Canada a student loan only automatically gets discharged or goes away in a bankruptcy or a consumer proposal if you’ve been out of school for more than seven years. So, it’s not like you can graduate and then go bankrupt the next day and get rid of your student loan. If you’ve got a student loan at the time of your bankruptcy and that’s the reason you’re going bankrupt you’ve been struggling with it for a long, long time.

When I went to university in the 1980s, tuition was low, maybe around $1,000 a year. So, a student like me could get a summer job earning minimum wage and I could earn enough to cover tuition and books. If your parents could cover your living expenses you could complete a four year program without the need to resort to student loans to fund your higher education.

Today, totally different story, a typical undergraduate program at a typical Canadian university will have tuition starting at around $6,000 a year and a more specific program can easily have annual tuition of $10,000 or more. You add in the cost of books and other fees and living expenses and a year of post-secondary education can easily cost $20,000 or more. Well, how many students can earn $20,000 at a summer job? If you can find a job at $10 an hour you can work 40 hours a week for 16 weeks so you could gross $6,400 during the summer, which of course will be less after taxes and other deductions.

So, even if you can work eight hours per week throughout the school year at a part-time job it’s not mathematically possible for a student to earn even half of the cost of a typical university education. If your parents can’t make up the difference your only other option is probably a student loan. Even if you’re covering half your costs you graduate after four years and my example with $40,000 in debt. Is that student loan your fault? Should you have skilled college or university and entered the work force right out of school? Perhaps but without a post-secondary education it might be more difficult to find a well paying job. For young people today there are no easy answers and it’s not their fault.

I’ve got more thought so please stay tuned, I’ll be back after the break; you’re listening to Debt Free in 30.

It’s time for the Let’s Get Started segment here on Debt Free in 30. Today we’re answering the question is it my fault? If you’ve never had financial problems it may be difficult to understand how someone can get into debt. So, let me explain by telling you the story of Sarah.

Sarah is not her real name and I’ve changed some of the facts but here’s her story. Sarah was raised by a single mother so at an early age she learned the value of hard work. She started babysitting the neighbourhood kids when she turned 13 and by age 16 she had two part-time jobs working in a store after school and a restaurant on weekends. She saved enough money that she was able to pay for a good portion of her university education and she was happy to graduate with honours with only $10,000 in student loan debt, which was far less than most of her friends.

The year she graduated from university was a tough year. The economy was in a recession so not being able to find a job in her field she went back to working two jobs in retail and food service but she only earned minimum wage. Two years after graduation Sarah was able to get a job as in intern in her field but it was an unpaid internship so she continued working her weekend job to survive. With the internship experience on her resume, Sarah finally found an entry level position in her field.

Unfortunately the job required a car so with minimal credit history, Sarah’s only option was to finance a used car through a high interest lender. She used her credit card to buy some clothes for work. She did great in her job but now that she was working she was required to start making payments on her student loan and with her car loan and credit card payments Sarah was only able to make minimum payments.

Then one morning on the way to work, Sarah was hit by a drunk driver. Sarah broke her arm and leg, her car was destroyed and she spent six weeks in hospital recovering. Her car insurance paid her the replacement value of her used car, which was barely enough to repay the existing loan. Health insurance covered her stay in the hospital but her sick benefits didn’t start till she was off work for six weeks so she had no choice but to use her credit card to pay her rent and her car insurance.

Sarah was lucky. She made a speedy recovery and was back to work three months after the accident. Unfortunately she now had a student loan and a credit card in arrears so to replace her car with another used car, the interest rate on the car loan was even higher. Sarah calculated that it would be many years before she could pay off her student loan, car loan and credit card and only then would she be able to think about saving.

Well, Sarah was lucky. She was able to return to work in three months, her employer was very accommodating and held her job open and shifted her work responsibilities so she could continue her physiotherapy. Sarah, didn’t have a spouse or child to support and she didn’t have a big mortgage to worry about. Her situation could have been much worse. But even as one of the lucky ones Sarah, who was a hard worker, was still stuck with a lot of debt and no prospects to get out of debt any time soon.

So, now I ask you to consider this question what should Sarah have done differently? What different actions could Sarah have taken to avoid her dire financial circumstances? Well, perhaps instead of going to university she could have continued to work at her minimum wage jobs. She wouldn’t have had a student loan and with hard work maybe she would have advanced to a job making more than minimum wage. Perhaps she should not have been driving to work on a road that a drunk driver was driving on. Or perhaps there wasn’t anything Sarah could have done to avoid her current circumstances. She did everything right and she still ended up in debt. It’s not Sarah’s fault.

At the start of this show I mentioned the financial gurus who tell you that into each life some rain must fall. But with a good work ethic and frugal lifestyle Sarah can get back on track. Well, so let’s test that opinion by doing the math. Let’s assume that Sarah’s take home pay is $2,500 a month and let’s assume that her rent, food, transportation and other basic living expenses are also $2,500 a month. So, here’s the math question. How much can Sarah afford to pay each month to pay down her credit card and student loan debt? I’ll wait while you get out your calculator to perform this complicated calculation.

Well, of course the answer’s obvious. Despite living a prudent and frugal lifestyle, Sarah has no extra money to devote to debt repayment, none. And that’s why for some people, debt problems aren’t their fault. It’s not always possible to work harder to make ends meet. Sometimes the ends don’t meet. So, before you beat yourself up over your debt problems of before you start yelling at your adult children or your friends of family members for having too much debt, remember that sometimes it’s not your fault. Sometimes you do everything right but stuff happens and you end up in debt through no fault of your own.

If that’s you, don’t focus on the past, start looking for solutions for the future and don’t blame yourself. I’ll be back with some final thoughts after the break, that was the Let’s Get Started segment right here on Debt Free in 30.

Doug Hoyes: Welcome back, it’s time for the 30 second recap of what we discussed today. On today’s show Kelley Keehn and Robert Brown both explained that circumstances beyond our control can lead to financial problems but we should also do what we can to prepare for the future. That’s the 30 second recap of what we discussed today.

So, what’s my answer to the question whose fault is it? I’m not a judge, it’s not my job to determine guilt and innocence. If you want a quick answer, the answer is it’s everyone’s fault. It maybe my fault for borrowing too much but lenders must also accept some blame for aggressive lending practices that make it hard not to borrow. Many people today have debt and other financial problems that are not entirely their fault. The sooner we acknowledge that reality, the sooner we can start working on solutions and solutions for the future are a much more productive exercise than paying the blame game for past perceived sins.

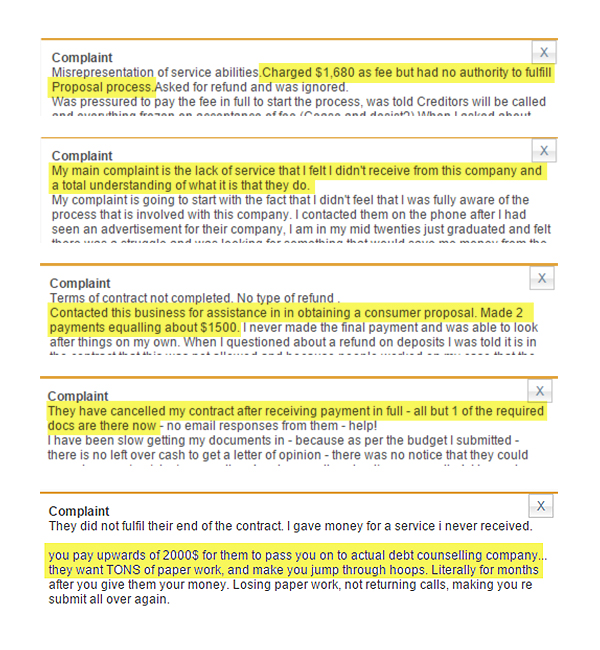

Now that the Ontario government has restricted debt advisors from charging up-front fees before completing a settlement with creditors, many debt relief companies are switching their business tactics. What they now offer is so called consumer debtor protection services, debt assistance or consumer proposal referral programs.

What is consumer debtor protection and what are they selling?

There are varying levels of disclosure about exactly what services are offered by these different debt help companies. What they propose is to help you eliminate your debt through some form of debt repayment program. This however is where things get a little cloudy. In almost all cases what they are selling is a consumer proposal and what they really offer is a consumer proposal referral program.

Some debt assistance companies are a little clearer in what they say they do, some a little less.

The may be up front admitting that they have a consumer proposal representation program.

Others are just advertising ‘government programs’ that can help you reduce your debts by up to 70% without admitting they really mean proposals through the Bankruptcy & Insolvency Act.

The last group advertise consumer proposals, yet they are not licensed to administer such a program and do not make that clear.

What typically happens when you contact one of these debt help companies is you work with a debt manager or debt advisor, often over the phone, who will talk to you about your finances then have you sign a contract for their services. The person you are speaking to is more than likely a salesperson, whose job is to get you to sign on the dotted line and agree to make payments before going further.

What they do:

They will ask you to sign a contract before doing any real work.

They may or may not help you prepare a budget.

They may or may not talk to you about all your debt relief options.

They will ask you to complete various forms which provide the information necessary to complete the consumer proposal documentation required by the federal government to file a consumer proposal.

One you have completed your paperwork AND you have paid all their fees, they will refer you to a licensed insolvency trustee.

In other words they are charging fees to manage the preparing of your debt proposal file, nothing more.

Can debt assistance advisors negotiate a better deal for you?

Here’s the funny part. All of the steps in the previous section (with the exception of the upfront fee contract) from reviewing your budget and financial situation, to helping you review all your options, and preparing the paperwork will be done by a licensed insolvency trustee for free.

So since your trustee will help you prepare the documentation at no charge, that begs the question, can these debtor assistance companies protect you by negotiating lower debt repayments?

First of all let’s start with the idea that the debt counsellor you are dealing with is negotiating with your creditors. In almost all cases they are not. They may look at your situation and help you decide how much you can afford to offer your creditors however that’s not necessarily worth the large fees they charge, especially when a trustee will do this anyway.

But wait, these debt assistance companies often say the trustee won’t negotiate on your behalf and that they are there to protect the debtor’s interests. While it’s true a licensed insolvency trustee represents the interest of all parties in a consumer proposal, including creditors and debtors, a reputable trustee will not negotiate a proposal that won’t work or make you file bankruptcy if that’s not the right solution. If you think they do either of those, get a second opinion – from another licensed insolvency trustee.

There are two criteria that need to be met when you offer your creditors a consumer proposal to reduce your total debt:

You need to offer the people you owe as much money (or more) than they would be entitled to receive if you were to file an assignment in bankruptcy; and

You need to offer the people you owe enough money to agree to the deal.