It’s easy to get dejected if your credit score isn’t where you want it to be. But just because you have a low score today, it certainly doesn’t mean that you’re stuck with it for life. Even if you have faced a bankruptcy or consumer proposal, or have accounts in collections, there are measures you can take to improve your score. In this guide, I explain what you need to know about rebuilding your credit after you have filed bankruptcy or a consumer proposal or if you have bad credit due to past mistakes in handling your credit history.

How much credit do you need?

I don’t advise that anyone, after completing a consumer proposal or bankruptcy, jump right in and start borrowing again. If you can live without debt, that’s great. However, in today’s modern economy you might need or want access to credit.

The first thing you should do is figure out why you want to improve your credit score. Begin by writing down your expected credit and financial goals.

Credit goals to consider:

Qualifying for a car loan

Getting a mortgage

Getting a credit card

Qualifying for a line of credit

Getting a student loan to go back to school

In addition to determining your future credit needs, it’s important to consider what financial or savings goals will help you qualify for new credit.

Savings goals relating to access to credit might include:

Setting aside money for a secured credit card

Saving a deposit for a car loan

Saving for a down payment to purchase a home

These savings goals need to be balanced with other financial goals like saving money for your child’s education or your retirement, so you don’t need to rely on credit in the future.

A credit score is simply a three-digit number between 300 and 900. The higher your score, the more credit options you will have and at lower interest rates. With Equifax:

729 to 759 is very good

660 to 724 is good

560 to 659 is fair

Anything below 560 is poor

If all you need is a credit card for bill payments or emergencies, you can generally qualify for a secured credit card with a credit score around 650. Even someone in an active consumer proposal or bankruptcy can get an unsecured credit card from certain credit card issuers as long as they don’t have a history of bankruptcy with that provider.

However, if your goal is to take out an auto loan or apply for a mortgage, you will need better credit.

But you need more than just a good score if you are thinking of getting a mortgage or low-interest car loan. To qualify for a larger loan from a regular lender, like a mortgage, your credit will be considered re-established when:

Two years have passed since you finished your bankruptcy or proposal

You have two accounts active or established after your completion date, and

Each account has a credit limit of $3,000 or higher.

One final word on credit scores. Your credit score is for the bank’s benefit, not for your benefit. Credit scores are designed to help the bank decide if they should lend to you. They are there for the bank’s benefit, not yours. Your credit score is only important if you want to borrow in the future. Never chase a credit score for vanity’s sake.

DIY Credit Repair

Repairing credit on your own is possible; it’s not complicated and it is often the fastest and cheapest way to rebuilding your credit. To rebuild credit you need to create a reputation as someone who can handle credit wisely.

Try our Free Online Video Course on Rebuilding Credit. Get a step-by-step plan on how to manage your credit score, how to review your credit report and fix errors and discover what types of credit you need to rebuild credit.

Here are the five steps to take to repair credit on your own.

Step 1 – Get a copy of your credit report

Your credit score is only as good as the information that is on your credit report. Credit bureaus get their information from your creditors, and mistakes happen. It’s up to you to ensure that the information on your report is accurate and presents a good image of how you manage credit.

The first step in rebuilding credit is to get a copy of your credit report. The best source is directly from TransUnion, Equifax or your bank if they offer you that service for free in their app or online banking platform. You can request a free copy of your credit report online, by mail or by phone. We’ve provided links and instructions in our article on how to get a copy of your credit report for free.

If you are rebuilding credit after filing a bankruptcy or proposal, we recommend waiting at least two weeks after your discharge or completion before requesting a copy of your report. You want to wait long enough for the government to report your completion date to the credit bureaus, and this is done weekly.

Step 2 – Fix all errors on your report

Now that you are armed with a copy of your credit report, the next step is to look at all the information and see what needs fixing.

There are several areas on your credit report to review.

Personal information

Be sure that your name, mailing address, social insurance number, birth date, and employment information are correct.

List of accounts

Review the accounts or creditors listed on your report. Regularly checking that these are companies you owe money to is a good way to monitor for fraud and identity theft.

Balances and credit limits

This information is used to calculate your utilization rate, which has a big impact on your credit score, so you want to be sure it’s correct. Accounts included in your bankruptcy or proposal should show a zero balance upon completion of your program.

Narrative

Next to each account will be a comment or narrative. If you filed a proposal, any debts included should be marked as ‘included in proposal’. Debts included in your bankruptcy will be marked ‘included in bankruptcy”. If this description is wrong, highlight it as something to be fixed.

Each account will also have a two-part code next to it – a letter and a number.

The letter shows the type of account – R for revolving like a credit card or line of credit, I for installment loan like a car loan, O for open accounts such as an internet or cell phone bill, and M for mortgage are the most common.

After the letter is a payment code.

0 means the account is new or approved, but you haven’t used it yet.

1 means it was paid on time. That’s what you are aiming for.

2 to 5 means there was a late payment on the account. The higher the number, the longer you were late. 2 means you were a month late, 3 means two months late, and so on.

A repossessed vehicle is coded as an 8.

An account included in a consumer proposal should appear as a 7. If your account is in collection or you filed bankruptcy, you will see the code 9. It is not uncommon for creditors to report an account included in a consumer proposal as a 9 until it is completed. Credit bureaus may not update this to a 7 until your proposal is finished. What you do want to be sure though, is that the narrative is correct, as this is what lenders look at.

If you decided to keep a financed vehicle when you filed and are maintaining your payments, make sure there is no narrative beside this debt. Secured debts are not included in your bankruptcy or proposal unless you gave the vehicle back. And as I mentioned before, make sure to make payments on time on accounts that remain after you filed, as this will help you improve your credit score.

Payment activity

Check the date of last payment or activity and the number of late payments reported. If you have filed a bankruptcy or consumer proposal, the date of last payment should be frozen at the date you filed insolvency. Creditors, in particular Canada Student Loans, may continue to report late payments during your bankruptcy or proposal. Again, make a note of this but know that credit bureaus likely won’t correct this until after you have been discharged or your proposal is finished. When they do, they should backdate the correction and remove any late payments to the date you filed.

Public records section

If you have filed a bankruptcy or consumer proposal, review the Public Records Section of your credit report. This is where information about the type of proceeding, the date you filed, and the date of discharge or completion will appear.

Other items

Check for any closed accounts still marked as open.

Look for duplicate records – the same debt reported twice under different names, or a bankruptcy or proposal reported twice.

Watch for old accounts being re-reported by collection agencies with updated payment dates or the reinsertion of information you previously had corrected.

Once you have identified everything that needs correcting, visit our article on how to correct errors on your credit report to get the necessary links to the dispute resolution form and information on how to dispute errors with both Equifax and TransUnion.

Step 3 – Pay your bills on time

Your payment history has the largest impact and makes up about 35% of your credit score. Late payments are the worst thing you can do for your credit score. If you have a credit score over 800, one late payment could make your credit score fall 30 points. To rebuild your credit, you must always pay your bills on time.

During your bankruptcy or proposal, make sure you keep up with your internet, cell phone bill, car loan payment, or any other active account that remains after you file. Missed payments will affect your chances to rebuild.

Most major cell phone providers report to the credit bureaus today. Paying your cell phone bill on time during your bankruptcy or proposal is very important. While it does not help your score increase because the payment is small, paying late will hurt your score a lot.

Step 4 – Establish new trade lines

The most important type of credit for credit rebuilding is credit cards. Mortgages and car loans and other forms of credit help, but credit cards have the most dramatic impact on your credit score. A credit card is revolving credit, meaning you control how much you use and repay each month. That makes a credit card the best tool to show you know how to manage credit wisely. And that is the goal of building a good credit history. Credit cards do not have a defined term like a car loan and as we know, the longer you have credit the better your score. Closing an old credit card account can lower your score drastically.

The downside is that high credit card limits can tempt you into borrowing. Only charge what you can pay in full each month.

If you really need a credit card during your bankruptcy or proposal, you can try getting a secured credit card. A secured credit card is backed by a deposit you leave with the credit card company. They will use this deposit if you stop making payments which is why they are willing to lend to more risky borrowers, like someone in a consumer proposal. Getting a secured credit card can help you jump-start your credit rebuilding enough to help you qualify for a regular card after your bankruptcy or proposal is finished. Be prepared though, not everyone who filed a bankruptcy will be approved while still in an active bankruptcy. Talk to your trustee or credit counsellor to see if applying for a secured card while bankrupt is a good idea in your situation.

Start by requesting a small credit limit, say $300 to $1000, depending on how much you can save for the deposit. Our experience shows that Capital One is best for active bankrupts, while Capital One or Home Trust Visa may approve your application during a proposal. The Capital One card comes with an annual fee. Both charge high interest rates, so be sure to pay your balance in full each month.

After your bankruptcy or proposal is complete, and you have corrected items on your credit report, apply for a regular credit card. Certain lenders are more willing to lend to someone with low credit, like Capital One or Canadian Tire (or what’s called Triangle now). If you don’t have good enough credit to qualify for an unsecured card, try a secured card if you haven’t already done so.

After six months of making payments on time on your first new card, you have an increased likelihood of being approved for a second credit card. Credit card providers like MBNA, TD, CIBC, and PC Financial, in that order, are good options assuming these creditors were not included in your bankruptcy or proposal.

If you already have a car loan, you may already have a decent credit score, so you may not need a second regular credit card. As long as you are making your car payments on time, this loan already shows you can manage a healthy mix of credit.

Increase your limits slowly. Asking for a higher limit is asking for more credit, which may mean a hit on your credit report. If your credit card provider offers you a limit increase without you asking, then take it if it brings your unsecured limit up to $3,000 or higher.

Always wait a few weeks, or a few months, between credit applications. New credit may temporarily lower your credit score, so you don’t want to apply for a second credit card right after you got your first.

As a reminder, the goal if you want good credit so you can qualify for a low-interest car loan or mortgage is to have two active established accounts, with authorized credit limits of $3,000 on each card, and maintain a good payment history for two years after your bankruptcy or proposal is complete. You might get credit faster, but it may not be prime credit. It will likely carry a high interest rate and may not look good on your credit report to future lenders.

Step 5 – Keep your utilization rate low

Managing your credit score is more than just paying your bills on time. You must also manage your balances.

Filing your consumer proposal or bankruptcy allowed you to start your credit repair process with no more debt. That’s good.

However, as you rebuild your credit, you will need to carefully manage your future credit balances. Carrying high balances on your new credit cards will hurt your credit score.

Wait, so I can charge one thousand dollars on my new secured or unsecured credit card, but if I wait to pay off that balance until it’s due, my credit score could drop?

Yes, it’s called credit utilization, and it accounts for 30% of your credit score. Credit utilization is simply the amount of money you borrow divided by your total credit limit. Credit bureaus assume that if you need to use most of your credit limit, you aren’t managing your credit well and so lending you more money might be risky for the next lender.

To have a good credit score, you want a low utilization rate on revolving credit like credit cards or a line of credit.

And here’s the key point: you want to keep this balance low throughout the month. You don’t know when your balance will be reported to the credit bureau. Your creditor might report your balance two days before your payment is due. If you have a high balance, it looks like you are carrying a lot of debt, even though you make all of your payments on time.

You want to prove to the credit bureau that you are responsibly using your credit card, and that you don’t need it, which is why you keep your utilization rate low.

So, what’s the right utilization rate?

If you are rebuilding, our experience shows that zero is better than 30%, and you should never go over 50%.

So, if you have a limit of $500, how are you supposed to keep your utilization rate at or close to zero?

Simple, pay your credit cards early. You don’t have to wait until the bill is due to make a payment. I recommend you choose a fixed cost bill, like your cell phone or internet. Set this account to be paid off automatically each month with your new credit card. Next, pay off this balance the same day. After you set this up, hide your card so you won’t be tempted to spend more than you should. Check your credit card statements every month to make sure this is working and that your balance is zero on the due date.

This will do two good things for your credit. You will have a history of payments, and your balances will be low. You are proving that you don’t need the money.

It’s possible to lower your utilization rate by getting another credit card or raising your limit. However, having a lot of credit is risky. You might be tempted to run up your balances, leaving you in trouble with debt again.

Also, if you have a lot of credit cards with high limits, even if your score is good, future lenders may not be willing to loan you more money because they think you have too much credit already.

You only need to worry about managing your credit utilization on revolving credit like credit cards and lines of credit. You can’t manage your utilization rate on your mortgage or car loan. These types of loans start with a 100% utilization when new, and you make fixed monthly payments. Over time the balance you owe falls until it reaches zero.

Build good financial habits, not your credit score

After your bankruptcy or proposal, while you may want to rebuild your credit, my last word of advice is don’t obsess over your credit score.

If all you need is a credit card for everyday use, a credit score in the mid- 600s is likely good enough.

If you take the steps I outlined to re-establish your credit, including two active trade lines with authorized limits of $3,000 each, you should be able to get a mortgage or car loan at a reasonable rate two years after your bankruptcy or proposal is finished.

But getting a loan, and affording a loan, are two different things. The larger your down payment, the better chance of approval since the amount of loan you are asking for will be lower.

Also, remember that more debt benefits the bank. The more you owe, the more interest you pay.

What you don’t want to do is go back to using credit to make ends meet.

That’s why I recommend you focus on building some savings while in your bankruptcy or proposal as you prepare to rebuild your credit.

Remember, credit is not your money. The trick while taking on new credit to rebuild is to find the right balance. You need to show you can use credit but do so responsibly and not get overextended. You want to take on the right amount of credit at the right time for the right reasons.

My normal advice is not to use credit cards to pay for everyday living expenses like groceries or gas. Yes, you can earn some points, but the balances can quickly grow past what you can pay. If you do use your card more often, make multiple payments throughout the month – for example, with each paycheque. It will reduce the risk that you will end up with a balance you can’t pay off at the end of the month.

And if you do apply for a larger loan, apply for only as much credit as you need, whether it’s a car or a house or anything else you might finance. Don’t take on more credit than you can afford to repay. Focus on building savings, not debt.

Your end goal is to be better off financially, not to have a better credit score and lots of credit.

Today I ask a question that generates a lot of debate on our Facebook page: what happens if you stop paying your debts? More specifically, what happens if you stop paying your debts and you are not in a consumer proposal or bankruptcy?

To help me delve deeper into this topic, Ted Michalos, my partner and co-founder of Hoyes, Michalos & Associates, joins me to discuss the various outcomes of not paying your debts.

What happens if you stop paying your credit cards?

Defaulting on payments or being in arrears has consequences. The severity depends on just how far you are behind on your payments:

If you miss one payment, the bank or credit granter will send you a friendly reminder. Generally, it will say ‘we noticed you didn’t pay last month. If you’ve paid by now, ignore this message”.

If you do not pay for two months, you may receive a phone call or a letter saying ‘you are two months in arrears, please contact us’.

If you do not pay for three months, this is when the bank has to decide whether or not they are going to send your debt to a collection agency.

If they do send it to collection agency, you’re supposed to receive a letter or notification from the credit card company saying that they have done so. However, more often than not, most people do not receive a notice, or they receive it after the collection agency has called. If you receive a call but you have not received a written notification, you have the right when dealing with a collection agency to ask for a letter outlining what you owe and to who you owe the money.

If you’re getting a call from a collection agency that you’ve never gotten a call from before, the first question should be, who are you collecting for? Send me a letter explaining who you’re collecting for, what I owe, what the story is. Because … that’s the law here in Ontario. They have to send you written notice before they do that.

If you have not paid the collection agency, they will try to pursue you for a couple months before threatening legal action. If you still haven’t paid, the collection agency will have to decide whether they will sue you or send your debt back to the credit card lender.

If they choose to sue you and it’s under $2,500 in Ontario, they can file a statement of claim in Small Claims Court. The courthouse will then send you a notice, and you will have 21 days to respond. If you do not respond, the people who are suing get a default judgement, which allows them to apply for a writ of seizure or execution, giving them the right to garnish your wages, seize your bank account, or employ other intense measures.

If you can’t afford to repay your credit card debt, then you may need to look at other options to get out of credit card debt.

What happens if you stop paying your payday loan?

When you take out a payday loan, we strongly recommend against giving a void cheque or access to your bank account. If you can’t pay, they just take the money out anyway. If you don’t have enough money to cover the payment, they’ll try again tomorrow. And every time they try to take a payment, you get hit for a service fee.

You could put a stop to the payment on the account or close the account or if you have a lot of payday loans, you may need to consider options to eliminate payday loan debt.

What happens if you stop paying your income taxes?

The federal government doesn’t have to take you to court to garnish your wages or seize your bank account. They can even send a demand to pay or a notice to pay without telling you. It will go straight to your employer or bank, and you won’t find out until the money is gone or seized. Or, they can put a lien on your house, which serves like a mortgage, meaning they can take your house if you do not pay them.

CRA has many collection tools at its fingertips to ensure they receive their money. There are also no limitations on money owed to the Canada Revenue Agency. Walking away from income tax is never a good idea. You need a formal plan to deal with tax debt.

What happens if you stop paying for your car or mortgage?

Car loans, leases and mortgages are secured debts, meaning that you’ve made a pledge with your lender that if you stop making your mortgage payments, they have the right to take your car or house.

For cars, the financing company will repossess your car if you default on your payments. For houses, banks will initiate a power of sale, which is a legal procedure where they give you 35 days to bring your mortgage current. If you do not bring your payments current in that time, they can show up with a sheriff and ask you to leave in 24 hours. If banks have gone to a power of sale, you should be looking at the likelihood you will have to move.

A consumer proposal provides meaningful debt relief.

If you live on very modest means and own very little, its unlikely your creditors will take action against you. However, if you have a good income, savings, or assets, your creditors are likely to purse some form of legal action to collect on your unpaid debt. Therefore, if you do have assets or a good income, it makes more sense to speak with a licensed insolvency trustee about your options than it is does to stop paying your debts and hope for the best.

One option for dealing with debt is a consumer proposal. It is a legal arrangement where you repay a portion of what you owe to your creditors. Every dollar you owe is a vote and you need 50% of the votes to be in favour of your proposal. So if you owe six creditors but one has more than half the debt, it only matters what that one creditor decides. In addition, there are other factors that could have affect the likelihood of your proposal being accepted:

How much the creditors are getting in comparison to what they would get if you were to file bankruptcy. This takes into account any assets you own and if you would have to make surplus payments.

Some creditors have a standard amount on the dollar they would like to receive. Generally it’s 30% of the debt.

They will look at your activity prior to filing a consumer proposal. If you ran up the debts 3-4 months before filing, it might suggest to them that you were planning on filing a consumer proposal versus if the debt slowly accumulated through normal use.

They will also look at your expenses to see if nothing is out of the ordinary or if you could cut back to pay a little more. Special allowances are made for certain circumstances. For example, special dietary needs may require an unusually high grocery budget.

The last thing they consider is the overall viability of the proposal. Or in other words, do you have a steady job that you can make the payments? Are the payments reasonable and affordable while satisfying the creditors?

If you can satisfy the above requirements, there is a strong chance that your creditors will accept your proposal, providing debt relief that will give you a fresh financial start. It’s a better solution for dealing with debt problems than not paying and just hoping that they go away.

It’s the last show of the month, and as we do at the end of most months it’s time for our frequently asked questions show here on Debt Free in 30. On most frequently asked questions shows we’ve got a list of five or 10 questions. Today the list is much shorter. We’ll probably only get to two questions but they are two important questions.

The first question is one that’s been the subject of lots of discussion over on the Hoyes Michalos Facebook page. And as a reminder if you’re on Facebook you can find our page at faceboook.com/310PLAN, which also happens to be our phone number. Or you can go to Facebook and search for Hoyes Michalos or 310PLAN. So, the first question we’re going to answer today is can I just walk away from my debts? What would happen if you owned money on a credit card or bank loan and you just stopped paying it? In many cases if you are deep in debt, a consumer proposal or a bankruptcy is the necessary solution, but what would happen if you just stopped paying? You didn’t file a bankruptcy or consumer proposal, you just stopped paying.

That’s today’s first question so to answer it I’m joined by my Hoyes Michalos partner and co-founder Ted Michalos. So, Ted can I just stop paying? What would happen if I just walked away from my debts? What’s the process?

Ted Michalos: Well, let’s break this down and talk about different types of debt. So, one of the things you mentioned was credit cards. That’s a pretty common problem for people to have, so can you walk away from your credit card debt? Maybe. The bank has got to decide is it worth pursuing you so what do they know about you? Have you got employment, have you got money on deposit with them? Are you a good candidate for them to sue? So, if they decide that they really want their money back and you’re not co-operating, they could take you to court. Well, the bank could decide that you know what, you’re a bad candidate for a lawsuit, you haven’t got enough that it’s worth pursuing you and I’ll just let you get away with it. The problem is you just don’t know which one of those you’re going to be.

Doug Hoyes: So if I’m a bank, I got three choices then. I can just say forget it, which of course banks don’t like to do ’cause they don’t make a lot of money if they just stop collecting debts. They could continue pursuing you through a collection agency or they could take you to court. So, tell me about the whole collection agency process. If I have always paid my credit card and now I miss one payment, they’re not taking me to court, what’s the process when I miss that first payment?

Ted Michalos: Well, so when you miss one payment or you’re late with a payment, you’re probably still dealing with the bank or whatever the credit granter is themselves. And you’ll get a polite reminder next month saying, you know, we noticed you didn’t pay last month, if you’ve paid by now ignore this notice otherwise you owe double this month. That’s not too pushy, it’s just their way of saying you got to catch up what you owe us. If you’ve made a habit of this, then instead of getting that polite reminder you might get a phone call or a letter that specifically says, you know what, you’re behind. American credit cards are much more aggressive about that than Canadian ones by the way.

So, let’s say you missed a month’s payment, you got this friendly reminder and the second month comes around and you still don’t pay them. So, the bank will probably still deal with you themselves for that second month. So, again now it’s as if you didn’t get a phone call before you’ll probably get one now, you get a less friendly reminder or you get a letter that says you’re two months in arrears and we need you to deal with this, contact our offices.

It’s the third month when things get interesting. The third month is when the bank has to decide are we going to send this out to a collection agency? And this all about psychology, it’s bad for business for the bank to be yelling at you themselves, they want their money but they don’t want to have a bad public impression. A big bad bank is beating up on Jane Doe, the single mom who can’t pay their credit card bill. So, they send it out to a third party, the third party’s job is to collect and they get paid a commission.

Now the law says you’re supposed to receive a letter or notification from the credit card company telling you they’ve assigned it before you have any obligation to talk to a collection agency. So, in nine times out of 10 nobody ever receives that notice or they receive it after the collection agency called. So, if it were me, I tend to ignore those. If you haven’t gotten a notice telling you who it is that’s calling you, why would you talk to somebody on the phone, particularly about your debts.

Doug Hoyes: So and then that’s a practical tip then obviously. If you’re getting a call from a collection agency that you’ve never gotten a call from before. The first question should be who are you collecting for? Send me a letter explaining who you’re collecting for, what I owe, what the story is. Because you’re right, that’s the law certainly here in Ontario. They have to send you written notice before they do that.

Ted Michalos: Particularly in this day and age with identity theft. I live in Guelph and lately we’ve had a scam on our phone systems. Once or twice a day there’s a message on my machine saying you owe the federal government agent money, your taxes are in arrears, we’re going to initiate legal action, you got to call this number now. Well, the federal government doesn’t leave messages like that.

Doug Hoyes: No and you’re right. They’re getting very creative because with all the fancy phone systems now, they can mask their phone number, they can make it look like it’s coming from a 613 exchange, which is Ottawa and that’s where the federal government is. And so, it looks legit, so, as a starting point yes, get them to send you a letter so that you know.

Ted Michalos: So, now we’re back to the collection agency.

Doug Hoyes: So, we’re back to the collection agency then.

Ted Michalos: Alright. So, the collection agency is going to try and pursue you for a couple of months. Then they have to decide do they threaten legal action? And if they threaten do they actually go through with it or do they just send the credit card debt back to whoever your lender is and let them try to deal with you again?

Let’s say that they’ve decided that you’re a good candidate for a lawsuit. And we can talk about what makes you a good candidate to be sued. And they decide they’re going to do something. If the debt’s under $2,500 in Ontario, they can take you to Small Claims Court. Small Claims Court is a pretty simple system. The person wanting to sue you, goes to the courthouse, fills out a statement of claim, the courthouse mails you the notice and you’ve got 21 days to respond to it by saying whether or not you want to argue or dispute the fact, the amount that’s being claimed.

If you don’t respond, the person suing you gets what’s known as a default judgment. A judge basically says okay the debt must be real ’cause you didn’t argue about it. Then the next thing they’re going to do is apply for a writ of seizure or execution. This lets them garnish your wages, freeze your bank account. In some cases I supposed they can register something with the sheriff, which effectively puts a lien on your house and your other possessions, and it’s complicated stuff and it’s pretty intense.

Doug Hoyes: And it doesn’t happen a whole lot in the overall grand scheme of things. And there are relatively few people who actually get sued out of the total number of people who owe money. And the vast majority of those lawsuits would result in like you said a default judgment. I don’t show up in court ’cause what am I going to say? The purpose of court is not to figure out how much you should pay, it’s to figure out do you owe the money or not. It’s really that simple isn’t it?

Ted Michalos: That’s right. I mean the first responsibility of the court is that the person who’s trying to sue you has to establish that you actually owe the money. Now what you said it correct, most people don’t respond to these notices and so a default judgment kicks in. But if you were to ask a lawyer or anyone associated with the court just how many cases they actually see relative to how much credit card debt is out there, it’s an infinitesimally small number. It’s one of those things that it’s used as a threat to scare the bejeezus out of you but it isn’t often followed through on.

Doug Hoyes: And that’s a key point. It’s very rare, comparatively speaking, that someone actually gets sued. So, we’re answering the question can I just walk away from my debts? And you’re saying well, you know what? It’s relatively rare that someone is actually going to sue you for those debts. So, under what circumstances is a bank not going to bother suing you? That’s obviously the common response, when does that happen?

Ted Michalos: Well, so the most obvious instance is when they can’t find you. So, if you’ve got a relatively small debt on a credit card, and you’re difficult to get a hold of, so, you’ve moved once or twice because your circumstances aren’t great, so you’re not getting these notices anyway. The bank, you don’t bank with the bank anymore so your paycheque doesn’t go there. They don’t know if you’ve got any money. They know in the past that your income wasn’t great. I mean these are all things that it’s not worth spending money on a lawyer to try and sue you. It’s just good money after bad.

Doug Hoyes: And as a result they won’t do it. So, obviously not having wages is going to make a big difference. What’s the point in suing someone if you can’t garnishee their wages?

Ted Michalos: Right.

Doug Hoyes: So, let’s go through the different types of debt. So, you addressed credit cards right off the bat. That’s a fairly simple one to understand. And the process you described is one as going to happen with credit cards. What about payday loans?

Ted Michalos: I knew you were going to bring this up.

Doug Hoyes: I’ve always got to needle you there with the whole payday loan thing.

Ted Michalos: You push my buttons. Okay, so payday loans are a funny animal onto themselves because usually when you go and take a payday loan out, you give them a void cheque or access to your bank account. So, if you don’t go in and make your payday loan payment, they just take it. Now of course you could stop that by putting a stop payment on the account or closing the account. And quite frankly once you start dealing with a payday loan company, if you’re able to break the cycle that’s great, but don’t ever give them one of your void cheques. Don’t ever give them access to a bank account where your pay actually goes into. These guys are notorious for trying to take your payment today, well if it doesn’t go they’ll try again tomorrow. And every time they try to take a payment, you get hit for a service fee.

Doug Hoyes: Well and we’ve talked a lot about payday loans this month. I’ve had a couple of different guests to talk about them. So, you can go to our website at hoyes.com and search for payday loans and you can see entire episodes. And we’ve got more coming up in the future. So, that’s certainly a big topic. But the point is you can’t just say to your payday – when you get the payday loan, if you give them a void cheque or access to your bank account and they say well if you don’t come in Friday to pay it off we’re taking the money out of your account, you can’t just walk away from it if you haven’t already put a stop payment on it or –

Ted Michalos: You have to do something or you’re going to lose your money.

Doug Hoyes: You’ve got to do something, some action is required. So, what about income taxes that I owe? Can I just forget about that?

Ted Michalos: So a lot of people think they can forget about income taxes but you’ve got to remember that the federal government has a very long reach. They’re not required to take you to court in order to seize a bank account or garnishee your wages, they simply send out something called a demand to pay or notice to pay. And they won’t tell you that they’re doing it, it’ll go straight to your employer or straight to your bank. And after the money’s taken you’ll find out who did it.

So, if you’ve got a debt with the federal government, I wouldn’t play around with that one. It’s not the same as a credit card where they got to decide whether or not they’re going to sue you. It’s not the same as a payday loan. The federal government has the tools to take their money. And you know what I found in the past, they’re more likely to be aggressive with small debts, people that owe them a few thousand dollars than the people that owe them hundreds of thousands of dollars. Makes no sense to me but I guess it’s cause it’s easier to pick on somebody getting a paycheque than it is somebody running their own business and hiding money from them.

Doug Hoyes: Yeah and I guess the guy who’s the average working guy doesn’t have access to the fancy lawyers and accountants, and whatever to protect themselves.

Ted Michalos: That’s true too.

Doug Hoyes: Now the other element we haven’t touched on is The Limitations Act of Ontario, which says in laymen’s terms, what does it say?

Ted Michalos: So, the limitation’s act says if you haven’t affirmed, confirmed the existence of a debt in two years and legal action hasn’t been commenced in that two years, you now have a defence in court to say that effectively you don’t believe the debt is real anymore.

Doug Hoyes: And in real simple terms. If I haven’t made a payment in two years on that debt, then if they were to take me to court and sue me, and try to garnishee my wages, I could go to court and say hey judge, it’s been more than two years and they wouldn’t be able to get their judgment all else being equal. Now does that apply to income taxes?

Ted Michalos: It does not apply to income taxes.

Doug Hoyes: It does not. So, you can walk away from some debts. And if it’s been more than two years, it’s highly unlikely that they’re going to be able to take you to court and sue you. But income taxes are not subject to those rules. So even if you owe taxes from 10 years ago and you start working and you start generating tax refunds, they’re going to keep them and obviously Revenue Canada, Canada Revenue Agency has the power to freeze bank accounts and do other nasty things, so, walking away from taxes generally not a good idea.

Ted Michalos: Right.

Doug Hoyes: We’ve been talking up to this point about unsecured debt, tell me about secured debt. So, first of all what does secured debt mean?

Ted Michalos: Okay, so secured loan or secured debt is one that you’ve pledged, you said that if I don’t pay you, you have the right to come and take something from me, the most common examples, car loan, car lease or a mortgage on your house. So, with a car loan you basically say if I don’t make my loan payments, they’ve got the right to come and take your car.

Doug Hoyes: So, that’s pretty cut and dry.

Ted Michalos: It is and they’re more likely to do that than they are – than so the credit card where you don’t pay it. ‘Cause the credit card, their only choice is hound you or take you to court. With a car loan, okay well I can come take your car. And for most people the car has enough value that I mean you need it to get to work, you need it to get the kids to soccer, you’ve got to have a car. So, you find a way to make the payments, so it’s a much bigger threat they’ve got over you.

Doug Hoyes: And so walking away from a car loan debt means your car is going to be gone. It’s pretty much that simple. Unless of course it’s a car with no value and it’s not worth it for them to repossess. But in most cases that’s an obvious answer. So, a secured debt is a debt that is attached to something. A credit card isn’t secured, it’s not attached to anything. Income taxes in most cases aren’t attached to anything. Payday loans I guess are attached to your wages.

Ted Michalos: We should be careful with the tax ’cause it’s a little – they’ve got some special rights ’cause again we’re talking about the federal government. So, when a credit card sues you, they get a writ of seizure, write of execution and lets them garnishee your wages. The court’s given them some rights. They still can’t come and take your stuff from you. The tax department, if you owe income tax and the tax department puts a lien on your house, it serves like a mortgage on your house. So, it’s not like a judgment that there are ways to get around. That’s a secured debt just like your mortgage to the bank. It’s got to be paid or the government has the right to take your house.

Doug Hoyes: And they don’t have to go to court to do that.

Ted Michalos: Well, they go to internal tax court. But as far as the average person is concerned, they don’t have to, they just send a demand.

Doug Hoyes: They push some buttons on the computer. So, the final category then is mortgages. And again, I think the answer on this one’s pretty obvious. So, can I just stop paying my mortgage and everything will be great?

Ted Michalos: Only if you want to leave your house. Effectively what they’re going to do is decide do they initiate power of sale, which is just a legal procedure where they give you 35 days to bring your mortgage current. If you don’t bring it current in that time, they’ve got the right to show up with a sheriff, knock on your door and say you’ve got to be out in 24 hours. And as unpleasant as all this sounds, they don’t actually want to throw you out of your house, ’cause that’s not how they make any money. But if they go to a point of power of sale, you should be looking at moving.

Doug Hoyes: Yeah because the bank, the mortgage company isn’t going to just walk away from hundreds of thousands of dollars. They obviously want their money. So, let’s wrap this up then with an overall comment, then. So, what’s your advice? How do you know if you should just walk away from your debts or try to pay them or should you take some more tangible action like filing a consumer proposal or a bankruptcy?

Ted Michalos: Well, so as coarse as this may sound, the less you have, the less likely you are to be subject to some sort of legal action. So, if you’re a person that’s living on very modest means, maybe you’re on government assistance or a pension now, you’re not a good candidate to be sued, there’s not a lot of practical reason to do so. If you’ve got a good paying job, regular income, money in a savings account or assets that are worth a fair bit, then you are a much better candidate and more likely that someone’s going to take action against you. So, the more you have, the less likely you can just walk away from something.

Doug Hoyes: Excellent. We’ll expand on that in the Let’s Get Started segment but I said I wanted to get to two questions, so we’re kind of burning through the clock here on the first one but I think that was good stuff. So, the second question I want to answer today in the last sort of four or five minutes of this segment is what are the chances my consumer proposal will be accepted?

So, we just talked about one of the solutions when you are being pursued, your wages are about to be garnisheed, you can file a consumer proposal. So, give us the 20 second overview, what is a consumer proposal?

Ted Michalos: Alright so, a consumer proposal is an arrangement to repay a portion of what you owe. So, as an example let’s say you owe $30,000 to all your unsecured creditors, you can’t afford to pay that back. But maybe you can afford to pay back $10,000. And so you make a payment plan to pay that amount of money over a period of time, one, two, three, four, maybe five years. You’re automatically thinking well, why would anybody agree to accept less money? Well, a proposal is designed to be an alternative to bankruptcy. So, often in a bankruptcy the creditors get very little money, in a proposal you’re voluntarily saying I`m going to pay you some of what I owe, something is always better than nothing, which is why they make sense.

Doug Hoyes: And so, the creditors, which is the people I owe money to, have to vote on this. How does the voting work?

Ted Michalos: So, it`s a pretty simple. Every dollar you owe is a vote and we need half the dollars to actually accept the deal. So again let’s use that $30,000 example. If $15,001 or $15,000 and one cent were to agree to terms of the deal would be approved.

Doug Hoyes: So more than half have to say yes.

Ted Michalos: That’s right, a simple majority of dollars, not creditors. And that’s important because if you owe to six different people but one company has more than half the debt, then it really only matters what the one company says.

Doug Hoyes: In that case one person out of six is going to decide. So, okay you go through the analysis and decide yes, I should file a consumer proposal. So, the person is sitting in front of you and says okay Ted so what do you recommend and you say well I think, you know, $300 a month for five years is a good thing. And what are the chances then that the creditors are going to accept my proposal? So, you already hit on the first thing that they look at, which is comparing it to bankruptcy.

Ted Michalos: Yeah, it’s got to be a better deal than a bankruptcy. Why would anyone agree to take less money than they’re going to get if you were bankrupt, which is a very rules oriented project. You know exactly what you got to pay in a bankruptcy.

Doug Hoyes: But aren’t they going to get nothing in a bankruptcy?

Ted Michalos: It depends on your situation. So, there are cases where you actually have to pay money into a bankruptcy. If you have equity in your home, if you have savings, if you make more than the government guidelines for families of your size. It gets complicated and I don’t think we can get into it here. But bankruptcy does cost you something.

Doug Hoyes: Yeah, it’s based on your income and the assets you have. And I’ll put some links in the show notes to the concept of surplus income, which is what you’re talking about. Based on your income you have to pay more so if in a bankruptcy it’s likely I’m going to have to pay $3,000 because of my assets, my income whatever, the proposal is going to have to be more than $3,000 or else why would the creditors accept it?

Ted Michalos: That’s right. And there’s a second complicating factor. Most of the Canadian credit granters, so the banks, the credit card companies, the loan companies have all said that they want a minimum return to accept a proposal. So, they won’t just – it doesn’t just have to be better than a bankruptcy, it needs to be about a third of what you owe. It’s possible to get deals accepted for less than that but the standard response or the standard request that all of these lenders have told us they want, is about a third of the debt. So again, you owe $30,000 then probably they’re going to ask you to pay back 10.

Doug Hoyes: Yeah and when you come into see us obviously we can look at the specific creditors you’ve got. There are some that are more likely to accept 20 cents on the dollar, so each case is different. But you’re right, if a bankruptcy is going to generate one cent on the dollar for them, it’s unlikely that they’re going to accept two cents a dollar in the proposal. Even though it’s twice as much it’s just administratively –

Ted Michalos: It’s not worth the trouble.

Doug Hoyes: It’s not worth the trouble. So, one of the other things they look at is prior activity. What does that mean?

Ted Michalos: Yeah so what they want to know is how have you been using your credit? So, did you deliberately run the balances up in the three of four months before you came in to file? That suggests that maybe this was a planned activity and they might ask for more money to be returned. Or were you using it in an unusual way? So, traditionally you use it to buy gas and groceries and small expenses, but two months ago you took a trip overseas and you put $10,000 on your credit card that you wouldn’t normally do. Or you repaired the engine in your car, something unusual or out of the way. Anything like that causes them to take a look and say well was there something deliberate done here? Do we need to ask for a little bit more?

Doug Hoyes: And again, that’s something that we could advise you on. They also look at your expenses every month.

Ted Michalos: Yeah, this is – it’s kind of a grey area. So, the government has established guidelines for how much they think a family of different sizes they think need to live on. And so, within that number this is what they expect you to pay on rent. This is what they expect you to pay on groceries. This is what they expect you to pay on gas and insurance. And they see enough of these things that if something in unusually high, they’ll notice it.

So, for instance a family of three might spend anywhere between $700 or $1,000 a month on groceries. Well, if your family of three is spending $2,000 a month on groceries, they might wonder why. And there could be very valid reasons for it. Nobody’s saying you can’t spend your money the way you want to, but they’re going to look to see are you doing something out of the norm or something that perhaps they could say well if you cut back on that, you could afford to pay us a little more?

Doug Hoyes: Yeah, if you’ve got special diet requirements or something that maybe a reason and which case that would be explained to the creditors. I guess the final criteria they look at is the overall viability of the proposal. Do you have a job that’s going to allow you to continue making the payments, that sort of thing?

So, there’s a number of different factors that go into it. I guess the closing comment is well when you come in and see us we’ll look at your situation and figure out what it’s going to take to make it work in your situation. That’s really the key. We’re going to get into a little bit more detail in the Let’s Get Started segment and all of that. But for now we’re going to take a quick break and we’ll be back with the next segment. You’re listening to Debt Free in 30.

It’s time for the Let’s Get Started segment here on Debt Free in 30 where we emphasize practical advice for dealing with debt problems. Before the break Ted Michalos answered the question how do I know if my consumer proposal will be accepted?

So, Ted let’s get practical with this, what advice would you give someone to increase the chances of their proposal being accepted. When someone comes in to see you and you review their situation and it looks like a consumer proposal is the best option, what practical things can that person do to increase the chances of their proposal being accepted?

Ted Michalos: Well, we touched a little bit on this before. So, when you’re looking at your household budget, which is money coming in and going out every month, we have to disclose that to the creditors, they get to consider your proposal. You want it to appear reasonable. So, you don’t want to have $500 a month for red licorice, which would seem like a luxury to most people. You want to be in line with what the average Canadian household spends on their groceries and their living expenses, and all the other places that their money goes. You don’t want to have unusual transactions, particularly large dollar amounts, going through your credit cards, lines of credit loans, in the two or three months before you file a proposal.

So, they’re looking for how you continue to act in your normal manner, so this really is a solution that you’ve come upon? Or did you plan the solution so you ran your debts up a little higher? Most importantly it’s are you making an offer that makes sense? Are you going to be able to afford the payments? Are you offering them as much of a payment as you can afford? So, you’re looking at your budget and it turns out that, you know, you should be offering $250 a month. Well, if your budget only supports a payment of $150, then the proposal’s not likely to get approved. If your budget shows that you can afford $350, well then $250 might get bumped up. So, all of this is deal with someone who’s got enough experience in the industry that files enough of these that they can guide you properly through this minefield.

Doug Hoyes: Yeah and the first thing we’re going to do when we sit down with you is look at your budget. And a lot of people don’t have a budget so that’s not problem, let’s piece it together. How much do you spend on rent? What’s an average grocery bill and so on? And it may be that there are some things that you’ve got to cut out before the proposal gets filed. So, your example of $500 a month on red licorice, I mean I guess black licorice should be okay.

Ted Michalos: Somebody had that on their budget once; I’m not making this stuff up.

Doug Hoyes: There you go. And well, we’ve seen it. I’ve seen people who have, you know, I spend $300 a month buying magazines. Okay, well maybe what you need to do then is go to the library and buy them because the creditors aren’t going to accept a proposal where you pay $200 a month if you spend $300 a month on magazines. Unless I guess that’s part of your job that you have to read them. So, what’s reasonable? It’s actually modifying the budget, modifying your actual expenses, it’s not the budget, it’s what you’re really spending that needs to get reduced. Now I would assume that the more you offer the better because the creditors are more likely to say yes to it.

Ted Michalos: And that’s a reasonable assumption. Keep in mind here that the creditors understand that you’re offering a proposal because you cannot afford to pay them in full. If they ask you to pay the debt in full, so they turn down your proposal for anything less than that, you might just file bankruptcy where again they’re going to receive less money. This has got to be a win/win for everybody. So, the proposal’s going to be structured so that you give them more than a bankruptcy, at least a third of it is that you owe. But they’re not going to force you to pay so much that the bankruptcy becomes a more attractive option.

Doug Hoyes: Well, and it has to be something you can afford obviously. If you can only afford $300 a month, then them asking you for 500 doesn’t make a whole lot of sense. Now one of the criticisms I hear all the time is you license insolvency trustees, we know how this thing works. You get paid a percentage of the money that gets distributed to the creditors.

Ted Michalos: That’s true.

Doug Hoyes: So, we don’t get upfront fees, we don’t charge you money to come and talk to us. But once the proposal is up and running and it’s been accepted and we’re distributing money to the creditors, we get a percentage of the money that goes out. So, it would therefore seem that the higher the proposal the better for us ’cause we’re making more money. So, how do I as a debtor who comes into see Ted Michalos at Hoyes Michalos, know that you’re not recommending $400 a month in my proposal just so you can make more money, when really $300 would have worked.

Ted Michalos: Yeah, I mean a couple of common sense things. People in the community, word gets out pretty quickly if there’s someone asking you to pay more than you should have to pay, I mean I don’t expect you to go to the hairdressers or down to the pub tonight, and talk about you’re filing a consumer proposal, but word gets around. So, if a trustee is suddenly forcing people to pay more than they should on a regular basis, they won’t be doing many proposals. So, I guess one of the questions you could ask is: how many proposals do you file every month. If a trustee tells you one or two, as opposed to 10 or 20 or 30 or in our case a couple of hundred, that’s a pretty good indication that maybe they’re not experienced at it and maybe they’re asking for too much money.

The flip side of course is, if we ask for more than you can afford to pay then you won’t make the payments and we won’t make any money at all and the creditors won’t make any money. So, the creditors won’t be happy with us. So, there are checks and balances in the system.

But at the end of the day, you’ve got to be comfortable that the payment that’s being suggested is one that you can afford. And then the creditor’s got to decide is it enough money? And frankly, very few trustees would let you file a proposal that they don’t think would be accepted. It doesn’t serve any use or purpose to offer 10 cents on the dollar if we know the creditors want 20 or 25 cents on the dollar. So, if you find somebody that’s letting you do something that sounds too good to be true, it probably is too good to be true.

Doug Hoyes: You’re right, it has to work for both parties, that’s the name of the game. Excellent, thanks very much Ted for answering those two questions for us. That was the Let’s Get Started segment. I’ll be back to wrap it up in a minute right here on Debt Free in 30.

Announcer You’re listening to Debt Free in 30. Here’s your host Doug Hoyes.

Doug Hoyes: Welcome back. That’s our show for today. So, to find out more about walking away from your debts or how you can evaluate whether or not your consumer proposal will be accepted, please go to our website at hoyes.com, that’s h-o-y-e-s-dot-com for full show notes and links to everything we discussed today. Thanks for listening. Until next week, I’m Doug Hoyes. That was Debt Free in 30.

In a previous article, we compared the cost of 4 different debt relief programs and determined that in most cases a consumer proposal offers the lowest possible monthly payment, significantly better even than a debt management plan. Inevitably when we do this comparison the question comes up – but what about the impact on my credit score? A bankruptcy or consumer proposal will affect my credit so isn’t that bad?

There is a misconception that credit counselling, or a debt management plan, will not affect your credit score. In fact, it will.

Even though you are agreeing to repay your creditors in full through a debt management plan, it is still considered a repayment program that is reported to the credit bureaus.

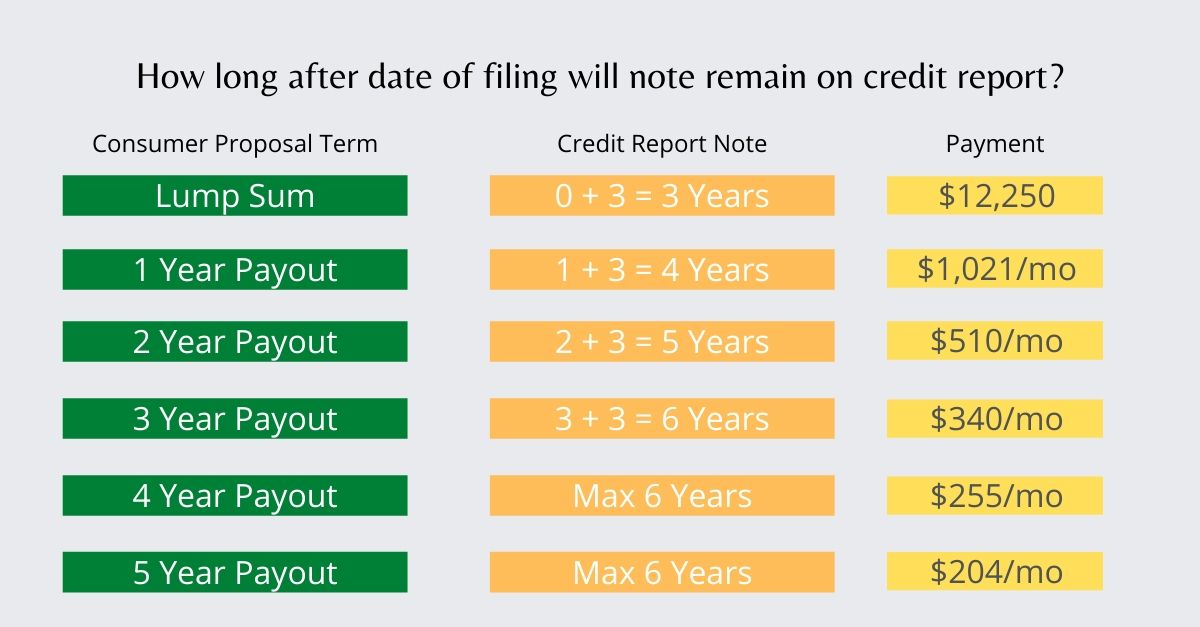

A debt management plan will appear as an R7 on your credit report. This note will remain for the lesser of 6 years from the date of filing or 3 years after completion.

A DMP through credit counselling has the same impact on your credit as a consumer proposal yet it is much more costly.

To help clarify the confusion, below is a summary of how the various debt relief programs will appear on your credit report.

How does a debt management plan appear on your credit report?

This rating will remain for a maximum of 6 years after default which is usually when filed.

It is removed the earlier of six years from filing or 3 years after completion.

Each debt included in your proposal will be marked as part of a consumer proposal.

The individual debt will be cleared 6-7 years after the date of default

In other words, both a consumer proposal and debt management plan have the same impact on your credit report. There is no difference in how these debt programs are reported and when the notice is removed.

The sooner you pay off your program, the sooner it is removed from your credit report.

The main benefit of a consumer proposal over a debt management plan is that you pay less than you owe. This makes your monthly payments much lower.

Let’s look at an example. If you owe $35,000 in credit cards, payday loans and other unsecured debt your payments under each program could be as follows:

5-year debt management plan: $642 a month (full payment plus 10% fees)

5-year consumer proposal: $204 (assuming your creditors settle for 35cents on the dollar)

If you have room in your budget, you can increase your proposal payments and pay off your proposal faster. Given the smaller monthly payments, this is more likely than being able to increase your debt management plan payments above $642.

Here is why this is important.

There is a direct relationship between how long it takes to pay off your consumer proposal, and how long this will impact your credit.

This holds true for both programs, but again since a proposal costs less than a debt management plan, being able to repay your proposal faster is more likely.

How does bankruptcy appear on your credit report?

A bankruptcy is listed as an R9 credit rating.

First time bankruptcy, no surplus income: 9 months + 7 years = just under 8 years

First time bankruptcy with surplus income: 21 months + 7 years = just under 9 years

Individual debts are purges after 6 – 7 years

The above addresses how long the notice of any debt relief program will appear in the legal section of your credit report. In addition, each debt is purged from your credit report after a period of 7 years for TransUnion and 6 years for Equifax.

Choosing a debt relief program is about getting out of debt in the best possible way. While the impact on your credit history may worry you, the determining factor should be which program makes the most sense for you financially.

If you need debt help, contact us today to book a free no-obligation consultation. We’ll explain the cost and impact of all options so you have the information you need to make an informed decision about what solution is best for you.

A consumer proposal is a safe and reliable way to get out of debt but it can also be the cheapest in terms of monthly payments. This is because a consumer debt proposal combines two substantial benefits over other debt repayment options:

Debt forgiveness; and an

Interest free repayment period.

To illustrate we will look at a typical debt situation and compare the financial cost of 4 different approaches to eliminate debt including a consumer proposal. A consumer proposal deals with unsecured debts and reduces your overall monthly payments substantially.

The Scenario:

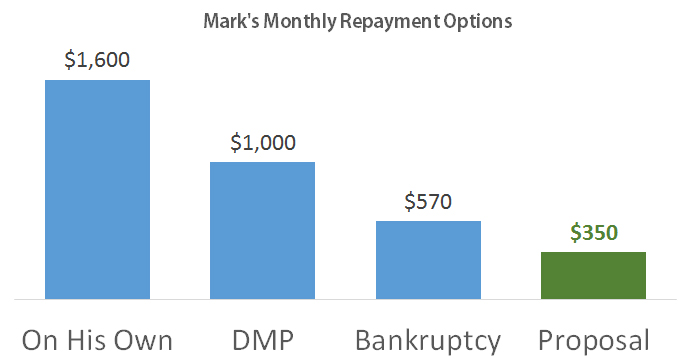

Mark owes $60,000 in consumer debt, a fairly typical amount for the average insolvent debtor.

His monthly minimum payments average $1,200 a month.

Mark is single and earns $3,200 a month after tax.

Mark owns no other assets that would have to be surrendered to his creditors.

In all repayment plans, we assume Mark would like to be out of debt in a minimum of 5 years.

Repayment Options

Repay on his own – cost $1,600 a month for 5 years.

If Mark want to pay off his credit card debt within 5 years he will have to increase his monthly payment to almost $1,600. That is the equivalent of half of his paycheque. He will have to make this payment amount every month for 5 years and during that time cannot incur any other debts as this will increase his interest costs further.

Debt Management Plan – cost $1,000 a month for 5 years.

A debt management plan, filed through a credit counsellor requires that you repay your debts in full. You can achieve interest savings, which is why Mark’s monthly payments in our example decline by $600 a month however there is no reduction in the total principal payments you must make.

Personal Bankruptcy – cost $570 a month for 21 months.

Bankruptcy costs are not based on the amount of debt you owe but rather how much you make and what assets you own plus a base contribution to cover the value of non-exempt small personal belongings and administrative costs. Based on his higher income, Mark would be required to make surplus income payments of approximately $570 per month, assuming his income does not change. As a first time bankrupt with surplus income his bankruptcy would last 21 months after which he would be discharged and his debts would be eliminated.

So in the case of Mark’s bankruptcy, he would be out of debt sooner than his expected timeline, and for significantly less than the cost of a debt management plan.

Consumer Proposal – cost $245 – $350 a month for 5 years.

In Mark’s case he wanted to be out of debt within 5 years. He has to option to file bankruptcy to meet this timeline but if he wants to lower the monthly cost of getting out of debt he can consider a consumer proposal.

A consumer proposal is a legal way to negotiate an arrangement with your creditors to repay a portion of your debt and spread those payments over time. The cost is based on what you can afford and what you can negotiate with your creditors. Creditors typically expect to receive slightly more than they would in a bankruptcy because you are spreading payments over a longer period of time. In addition, certain creditors expect to receive a minimum recovery on their debts. Some big banks (like RBC and CIBC) often expect recoveries in the 30 cents on the dollar range. While every situation is unique, since everyone’s cash flow needs and creditors differ, in our scenario Mark would likely be able to negotiate a repayment plan costing between $245 and $350 a month for 5 years.

As you can see this is substantially lower than the costs of any other debt relief program. It is for this reason that debt management programs only have a 43% successful completion rate.

In choosing a consumer proposal over bankruptcy, Mark would be making a tradeoff between getting out of debt sooner and lower monthly payments. In doing so his total costs over time are higher compared to bankruptcy yet are still much lower than those in a debt management plan filed through a credit counselling agency.

What this shows is that in most cases where debtors are dealing with substantial debts the debt forgiveness, combined with an interest free repayment period, make a consumer proposal the lowest cost option when comparing debt recovery programs.

It is true that a consumer proposal is not for everyone however if you are severely in debt it is worth exploring. We’re here to explain all your debt relief options and help you choose the right one for you.

It’s no secret that payday loans charge an outrageously high interest rate. In Ontario, as of 2018, payday lenders can charge $15 for $100. If you take out a new $100 loan every two weeks, you would pay $390 a year, that’s an interest rate is 390% on an annual basis. And therein lies the problem with these types of loans. But what is the solution?

On today’s podcast, I speak with Jonathan Bishop, a Research and Parliamentary Analyst at the Public Interest Advocacy Centre (PIAC) about Bill 156 and pay day loan regulation. The PIAC is a non-profit organization that conducts research into public service issues that affect consumers. The payday loan industry is something they have been investigating for well over a decade.

History of Payday Loan Legislation In Ontario

Before 2007 interest rates were limited to a maximum of 60% under the Criminal Code of Canada. The Criminal Code was amended in 2006 to allow payday lenders under provincial regulation rather than under the usury laws of the Criminal Code. Payday loans would be allowed to charge more than 60% as long as provincial legislation existed to provide set limits around the cost of borrowing even if this exceeded the criminal code rate. In reality Ontario payday loans were already operating at that time so the amendment to the law prior to 2007 permitted what was already occurring with payday loans in Ontario.

Ontario itself enacted the Payday Loans Act in 2008, limiting fees to $15 per $100 borrowed for two weeks as of January 1, 2018.

explore opportunities to increase protection for vulnerable and vetted consumers such as modernizing payday loan legislation.

PIAC responded to the initial call for comments with a 50-page policy analysis and a recent research report on debt collection practices. Bill 156 was the result of the consultation process.

One of the changes proposed in the bill will affect repayment time. If you get a third payday loan, the loan becomes an installment loan that has to be paid back over a period of 62 days instead of two weeks. This is to help break the payday loan cycle of someone trying to repay a payday loan with a payday loan from another payday loan lender.

As Jonathan says:

One of the other outstanding issues with a payday loan product is that onetime balloon payment in terms of the borrower has to pay it back all at once. There’s no kind of steps to doing it or planning. It’s just ‘here’s my paycheque. Oh here you go, you’re the first in line ’cause you have my paycheque, so I don’t have any choice’… rather than if you say two paycheques or three paycheques to pay it off.

Jonathan also mentioned that part of the challenge with payday loans is access:

Traditional financial institutions move out of a neighbourhood in a process called ‘redlining’ to focus on geographic areas and products offering a higher return.

Additionally, small ‘mom and pop’ businesses historically provided some of the basic services of a bank for a nominal fee, such as cashing a cheque. The proliferation of big box stores has squeezed small businesses out of the market, further reducing a community’s access to affordable financial services.

Payday lenders and alternative cheque cashing services move in to fill the void but at a high cost.

Possible Solutions to Payday Loans

A possible solution that Jonathan offered, was that a trusted authority such as the Ministry of Consumer Services could provide the community with the locations and business hours of alternatives that are within walking distance or within their neighbourhood.

In addition, another solution the PIAC put into its submission to the Ontario Government, was that the government should support legitimate micro-credited initiatives by partnering with local financial institutions to make this financial product available. The goal being that these micro-loans would be a competitive product that satisfies the need for immediate cash without trapping a person on in a payday debt cycle.

Other structural changes Jonathan would like to see in Bill 156:

some lengthening of the repayment period,

a limit on the number of payday loans a person can borrow in a given year

a reduction in the allowable cost of borrowing, and

lenders should be required to consider the borrower’s ability to repay the payday loan before granting credit.

He notes that in Manitoba, a payday loan cannot be more than 30% of the borrower’s net income. In British Columbia and Saskatchewan, the limit is 50% of the borrower’s next paycheck. The PIAC, recommends that the limit should be no more than 5% of the borrower’s monthly income to give the borrower enough money for other living expenses.

Doug acknowledges that some of the changes proposed in Bill 156 may help, but he is concerned that the bill isn’t addressing the underlying problem with payday loans – debt:

[Borrowers] are maxed out on their credit cards and they can’t borrow from a bank so they turn to payday loans. If we could address the underlying problems, one of which is excessive of debt, perhaps the need for payday loans would be greatly diminished.

Today we’re going to talk about a topic we’ve discussed here before on Debt Free in 30, payday loans. You’ve heard me give my thoughts on payday loans and I’ve other licensed insolvency trustees and credit counsellors on the show to discuss the evils of payday loans. We all know the problem, they charge very high interest rates. In Ontario, they can charge $21 on $100 loan so if you get a new $100 loan every two weeks you end up paying $546 a year, which on $100 loan is a 546% interest rate on an annual basis.

That’s the problem with payday loans but what’s the solution? Should the government have a greater role in regulating payday loans and short-term loans? Is that the solution? Would it work? If so, what should the government actually do? We already have laws regulating payday loans in Ontario, and most other provinces, and that hasn’t solved the problem so is the government the answer? That’s the question I want to ask my guest, who isn’t a licensed insolvency trustee or credit counsellor and he doesn’t work for a bank or payday lender.

So, let’s get started. Who are you? Where do you work and what do you do?

Jonathan Bishop: Good morning Doug. Thank you for having me. My name is Jonathan Bishop, I’m a Research and Parliamentary Analyst at Public Interest Advocacy Centre here in Ottawa. I do policy research on a variety of subjects, and including payday loans and financial service issues.

Doug Hoyes: Can you tell me what the Public Interest Advocacy Centre is? So, you – do you go by the initials, how do you refer to it?

Jonathan Bishop: Well, around the office we go by PIAC. Anybody that deals with us on a regular basis, that’s kind of what we’re known by. But the Public Interest Advocacy Centre is a non-profit organization and charity that provides legal and research services on behalf of consumer interests and particularly vulnerable interests concerning the provision of public services.

Doug Hoyes: So, you’re looking at people who – you’re doing research into issues that help real people. You’re not trying to figure out a way to make banks more profitable, you’re dealing with the actual real person is what you’re doing.

Jonathan Bishop: Yes.

Doug Hoyes: So, what kind of projects have you worked on in the past?

Jonathan Bishop: The past two or three years myself, I’ve worked on issues relating to wireless data roaming, the commissioner for complaints of telecommunication services, payday loans obviously, loyalty programs, online group buying, the amount of money you pay to receive a paper bill for communications or a financial institution bill on a month basis, things of that nature.

Doug Hoyes: So, a wide variety of things, so let’s talk then about payday loans. So, you’ve done some research into this area why don’t you start me off with a short history lesson then. So, what is the state of payday loan legislation, you know, in Canada and in Ontario whatever, wherever you want to start.

Jonathan Bishop: Sure, the Public Interest Advocacy Centre has been investigating payday loans for well over a decade. Prior to 2007 the maximum for all rates for all loans in Canada, according to the criminal code was 60%. However at that time an exemption to the criminal interest rate was passed to allow payday loans, which were operating in Ontario at that time, in provinces that opted to permit it. So, Ontario had them but they didn’t have any regulations around it. So, the amendment to the criminal code in 2007 kind of permitted what was already there. To my knowledge on Newfoundland and New Brunswick are the provinces remaining that don’t have active payday loan legislation.

Quebec for example has gone a different route than many of the provinces by limiting the criminal rate of interest to 35%. This has in effect curtailed the operation of payday lenders there.

Doug Hoyes: Just a question on that then, so in Quebec the maximum interest rate that can be charged I guess by any lender is 35% is that correct?

Jonathan Bishop: That’s my understanding, yes.

Doug Hoyes: And that’s curtailed payday lending just because it’s not profitable to do it.

Jonathan Bishop: That’s my understanding. I know there are still storefronts there but they’re not offering products on a similar basis as they do in other provinces.

Doug Hoyes: Got you. Whereas, where I said in the introduction at a place like Ontario here, the maximum interest rate, which is governed by federal law, as you said, which are governed by the usury laws I guess, is 60% but the payday loans get around that. Is it because of this specific provision that you talked about going back to 2007?

Jonathan Bishop: That’s right.

Doug Hoyes: That’s what it is, okay. So, they’re charging on an annual basis a higher rate of interest but there’s a special rule that allows them to do it is essentially what happened, okay.