In June 2016 Walmart Canada announced that they believe interchange fees charged by Visa are too high, so, starting with their three stores in Thunder Bay Ontario, they would no longer accept Visa cards at their stores in Canada. As of September, 2016 Walmart has not implemented this policy outside of Thunder Bay, presumably so they can continue to negotiate with Visa for lower fees.

On today’s Debt Free in 30 podcast we answer the question: what’s the real reason that Walmart doesn’t want to accept Visa credit cards at their stores?

The answer is not as simple as “Visa’s fees are too high”. Walmart is the largest retailer in the world, so with their bargaining power they are probably paying the lowest Visa fees of any retailer. They already have a cost advantage over every other retailer, so are high fees the true explanation for Walmart’s “anti-Visa” stance?

Perhaps, but I think there’s a better explanation: groceries and the Walmart Rewards™ MasterCard®, a credit card first offered by Walmart back in 2010.

First groceries. Groceries are a thin margin business. If Walmart wants to beat out the competition in terms of price, and accept credit cards as payment, then they will want the lowest credit card transaction fees they can achieve.

That get’s us to point number two – their own Walmart credit card.

Credit cards are big business, and a great source of profit. Walmart is an international company so they don’t release Canadian-only numbers, but I do know that Loblaws, a competitor of Walmart in Canada, will earn about $175 million this year from their “financial services” division. That’s big money.

Walmart wants to promote their own credit card, a MasterCard®, and what better way to do that than to ban the use of Visa? If you want to by groceries and other products at Walmart and use a credit card you may be forced to get a Walmart credit card, which will increase Walmart’s profit.

What Should Consumers Do?

My advice is simple: do your research. If a credit card makes sense for you because of the rewards you can earn, and if you can afford to pay it in full at the end of the month to avoid interest charges, great. However, be careful. The average person who files a consumer proposal or bankruptcy with Hoyes Michalos has more than $20,000 in credit card debt at the time they file, so avoiding credit cards reduces the chance that you will get into financial trouble.

Using credit cards? Read our post about why credit cards can be so dangerous available today or talk with a licensed insolvency trustee about your options.

Debit cards cost virtually nothing to use, and since the money is immediately withdrawn from your bank account you avoid debt.

Don’t let Walmart, or any other retailer, tell you what to do. You are the boss. Choose the payment method that works best for you.

Read the transcript for full details.

Resources mentioned in the show

- Walmart’s June 11, 2016 press release

- CBC News Story: Thunder Bay Visa Walmart Battle

- List of institutions that offer Visa cards

- Details on Visa’s Initial Public Offering in 2008

- Walmart’s website

- Walmart’s 2016 Financial Statements

- Walmart’s on-line grocery pick-up service

- Details on the Walmart Rewards Mastercard

- Annual interest rate on Walmart Rewards Mastercard

- Financial statements for Loblaws Canada

- Current merchant fees for Interac debit cards in Canada

FULL TRANSCRIPT show #106

Doug Hoyes: Last week I announced our new format here on Debt Free in 30. I said that some of our shows would be shorter than 30 minutes, and one of my goals was to use this new format to explore current topics, and that’s exactly what I’m going to do today.

I’m sure you’ve all heard that Walmart has announced that they plan to stop accepting Visa credit cards at their stores in Canada.

On June 11, 2016 Walmart issued a press release that said, and I quote:

Following an evaluation of credit card transaction fees in Canada and the rest of the world, we have concluded the fees applied to Visa credit card purchases remain unacceptably high.

Walmart’s purpose is to save customers money so they can live better. We are committed first and foremost to this purpose, which requires us to keep costs as low as possible.

To ensure we are taking care of our customers’ best interests and delivering on our promise of saving customers money, we constantly work to reduce our operating costs, including credit card fees. Unfortunately, Visa and Walmart have been unable to agree on an acceptable fee for Visa transactions. As a result we will no longer accept Visa in our stores across Canada, starting with our stores in Thunder Bay, on July 18, 2016. This change will then be rolled out in phases across the country.

To keep prices low we continuously assess opportunities to lower our operating expenses. Walmart Canada pays over $100 million in fees to accept credit cards each and every year. Lowering costs such as these is necessary for us to be able to keep our prices low and continue saving our customers money.

Customers will continue to be able to use other forms of payment including cash, Interac debit, MasterCard, Discover, and American Express.

We sincerely regret any impact this will have on our customers who use Visa and remain optimistic that we will reach an agreement with Visa.

Sure enough, in July, Walmart stopped accepting Visa cards at their three stores in Thunder Bay, Ontario, and the battle has begun. Walmart is taking the position that Visa charges high fees, and if Walmart passes on those fees to their customers that increases the cost of what they sell, and that’s not good for consumers.

Visa is fighting back, and has plastered billboards all over Thunder Bay, reminding customers that Visa is accepted at most stores in Thunder Bay, and around the world, and they have even started offering incentives for Thunder Bay residents to continue to use their Visa cards.

So what’s going on here?

Is this simply a dispute over money?

Is it as simple as Walmart saying “we are the biggest retailer in the world, and we are going to use our size and power to get the best possible deal from our suppliers, including Visa?”

Sure, that’s a part of it, but I think there’s more to it than that, so let’s break it down and examine what’s really going on with credit card fees, and let’s consider what all of this means for you, the consumer.

Walmart has stopped accepting Visa cards at their three stores in Thunder Bay, and is threatening to stop accepting Visa at all of their other stores in Canada, but they have said they plan to continue accepting cash, debit, and credit cards from MasterCard, Discover, and American Express.

So what’s really going on?

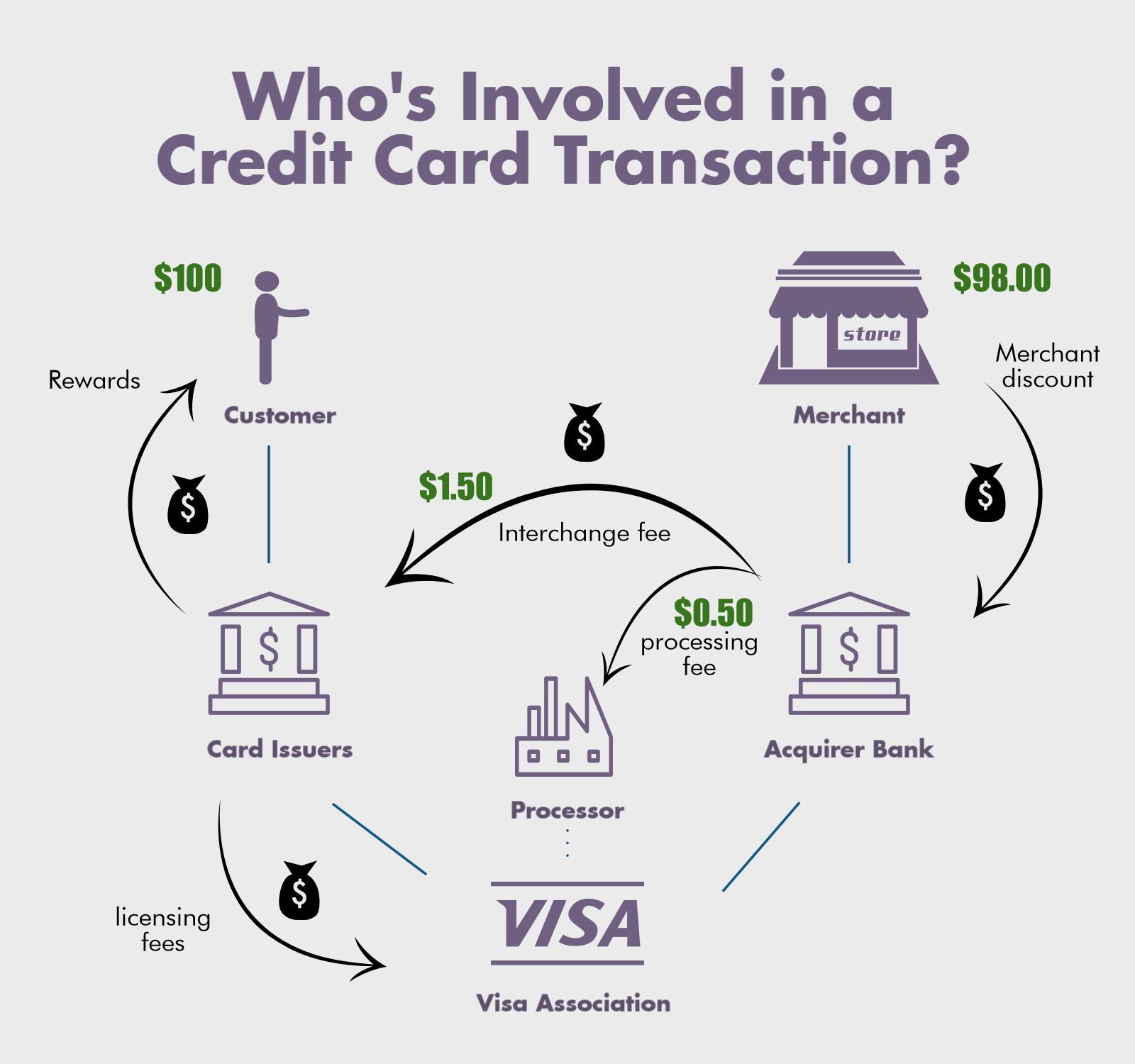

Let’s break down how credit cards work, because there are lots of different players in this story. It’s not just Visa and Walmart; there are actually six different participants in this story.

Obviously there’s the retailer, Walmart in this case.

Then there’s you, the cardholder, and when you look at your credit card you see two logos; you see Visa, and you see your Issuer, which is probably your bank.

So you have a credit card, but it also has the name of one of the other issuing institutions in Canada, which include most of the big banks, including:

- CIBC

- Royal Bank

- Scotiabank

- TD

But also includes smaller banks like:

- Citizens Bank and

- Laurentian Bank

- And other institutions including:

- Chase Canada

- Home Trust Company

- Le Mouvement Desjardins and

- Vancouver City Savings Credit Union

So that’s the first four players:

You, the merchant, Visa, and your bank.

There are two other participants:

The “Acquirer”, which is the merchant’s bank, and then the electronic payment system, called Visanet, which links it all together.

Okay, so there are lots of players, what’s the point?

The point is that every player wants to make money, so everyone is either charging or paying a fee along the way.

It starts with the merchant, Walmart in this case, who pays a fee to it’s acquirer bank. It’s called a merchant discount fee, and it would typically be in the range of 1.5% to 3.0% of the total transaction.

So if you buy something for $100 at a store, the store may only get to keep $97, with the other $3 being retained by the merchant’s bank. That fee covers the costs of the Visa terminal, and fraud protection, and the interchange rate.

What’s the interchange rate? It’s another fee, and it’s the fee the merchant bank pays Visa. This fee allows the merchant bank the right to access the Visa network, and pays for the cost of the transactions and other services, like fraud management and return management.

So in my example where the merchant pays $3 to their acquirer bank, that $3 in fees is shared between the merchant bank and Visa.

What about your bank? If you have a TD Visa card, how does TD make money?

Well, that’s easy: they charge interest and fees.

Some credit cards charge a monthly or annual fee, and that goes directly to the bank that issued your card. Your bank’s biggest source of revenue is from the interest they charge on unpaid balances on your credit card.

So it’s easy to see how the system works but if you’d like to see a graphic of all this check our our hoyes.com blog post about this podcast.

You, the consumer, get the convenience of a credit card. You don’t have to carry cash, and you don’t even have to have the money available when you buy something, because you can charge it on your credit card.

The big advantage of a network like Visa, MasterCard or American Express is that they are accepted in literally millions of establishments around the world. That’s a big advantage, because I don’t need to carry a separate card for each store I shop in.

The consumer benefits, but obviously so does the merchant. Stores are willing to pay a fee to Visa because they know that by accepting Visa they increase their sales. If a store only accepted cash, their sales would be lower, so it makes good business sense to accept credit cards, even if there is a fee involved.

Visa and Mastercard earn the interchange fees, and your bank makes lots of money from their share of merchant fees, and of course from credit card fees and interest.

And just so you know, Visa makes a lot of money.

When Visa first started it was owned by the credit card issuers, but in March 2008 Visa itself became a publicly listed company on the New York Stock Exchange, with the initial public offering priced at $44 per share

The ticker symbol is “V”, and on it’s first day of trading on March 19, 2008 it finished 29% above the offering price, closing at $56.86

Obviously there were a lot of investors who wanted a piece of the action, and Visa has turned out to be a great investment, with Visa trading up into the $80 range here in 2016.

So this is a good news story, right?

Everybody wins?

The consumer is happy, Visa and the merchants, even the investors, are making money, it’s all good?

Not quite. There is a seedy side to this story.

We’ve looked at the Visa business model from the point of view of the banks and Walmart, but what about the most important person in this story:

You, the consumer.

The dirty little secret is that nothing in this world is free.

If you get points on your credit card, someone has to pay for them.

If you get fraud protection, someone has to pay for it.

That someone, of course, is you.

The interchange rate and the merchant fees differ based on the type of card. If you have a basic credit card with no features, the interchange rate is low, but if you have a reward card with points, or cash back, the interchange fees and merchant fees will be higher.

Nothing is free.

The credit card business is very competitive. You’ve got lots of choice. It’s easy to switch, and Visa and Mastercard and American Express know that, so they have to offer lots of perks to keep their good customers.

But there’s a cost, and the cost is included in all of the goods and services we buy.

If a merchant is paying 3% in Visa fees, they probably need to increase their prices by 3% to cover their Visa costs.

Makes sense. If I’m a business that makes chairs, and if it costs me $100 to make that chair, and earn a slight profit, I may be willing to sell that chair for cash for $100, but if I sell it to you and you pay with your Visa card and I only get $97 because of the $3 Visa fee, I’m losing money, so I have to raise my price higher than $100 to cover all of my costs.

That’s how credit cards make goods more expensive.

So let’s go back to Walmart.

Walmart’s website says their goal is to “sell more for less”. Walmart is a discount store, so price matters. You shop at Walmart for the price.

I happen to be a chartered accountant so I reviewed Walmart’s 2016 financial statements, and they have an operating income of about 5% of revenue.

So if they sell something for one dollar, the actual product they sold cost them about 75 cents, and then their other operating, selling and administrative expenses cost them another 20 cents, so they have 5 cents left over as operating profit.

And for those of you listening who are accountants, that 5 cents isn’t Walmart’s total profit. From that they still have to pay interest on their debt, and taxes, so their actual profit ends up being around 3 cents per dollar of revenue, but let’s not complicate things.

My point is this: if you are a retailer, your margins are very thin. You only make 5 cents on every dollar of sales, so if you have to pay 3 cents to Visa, that’s a big deal. That’s more than half of your profit.

Now Walmart is the biggest retailer in the world, so they are probably getting the best possible deal from Visa, so I doubt they are paying anything close to 3%, but you can see that it’s still a significant expense.

But this is nothing new. Walmart has accepted Visa for many years. Why now, all of sudden, are they going to war with Visa?

My guess: groceries.

You can now buy groceries at Walmart, and there’s no doubt that they want to expand their grocery business.

In 2015 they launched an online grocery pickup service in Ottawa, and they expanded that service to 12 Toronto area stores in early 2016. Those customers can place an order on line, and then drive to the store and their groceries are ready and waiting for them, and all you pay extra is a $3 fee.

Groceries is a very low margin business.

I checked. I looked up the financial statements for Loblaws, one of Canada’s largest grocery chains, and in the most recent reporting period their operating income was just slightly lower than Walmart’s, about 4.8 cents per dollar of revenue.

If you want to accept credit cards in the grocery business, you must keep your costs as low as possible.

So it could be that as Walmart expands their grocery business they want to keep their credit costs as low as possible. That could be the reason for the fight with Visa now.

It could be, but I don’t think that’s the whole reason. Walmart has about the same cost structure as Loblaws, and we aren’t hearing stories about Loblaws fighting with Visa, so there must be something else going on, and I think there is.

I think Walmart wants to compete directly with Visa.

That’s why, in 2010, they launched their Walmart Rewards MasterCard. https://www.walmartcanada.ca/our-story/our-business

With your Walmart Rewards MasterCard you earn 1.25% of your purchases in Walmart Rewards when you shop at Walmart in Canada, and 1% when you shop anywhere else that the card is accepted.

Walmart rewards cannot be redeemed for cash, they are only good at Walmart, so it’s a great deal for Walmart. The more you buy, the more you come back to buy from Walmart. That’s how you redeem your rewards. It’s an endless cycle.

Store credit cards are very profitable.

Walmart is an international company so I don’t know how much their MasterCard earns them in Canada, but I do know from Loblaws’ financial statements that their Financial services segment generated $44 million in earnings before interest, taxes, and depreciation and amortization, what accountants call EBITDA. That would project out to over $175 in profit for the year, and that’s an increase of over 15% from last year, so it’s a growing source of income.

And that’s the simple answer to why Walmart doesn’t want you to use Visa cards in their stores. They want you to use their own Mastercard so that not only can they save the Visa fees but they can also earn extra revenue from the card itself.

If you want to shop at Walmart, and you want to use a credit card, what choice will you have? For many customers the easy choice will be to get a Walmart Mastercard.

It could be a big win for Walmart.

Or not. If you like your Visa card and decide not to get a MasterCard, Walmart could lose customers. We shall see.

My guess is that this is both a test and a negotiating tactic for Walmart. They’ve proven to Visa that they are serious, but they only shut Visa out from three stores, so it’s not costing them much. It’s also a great test. Walmart now knows how many customers they lost in Thunder Bay by not accepting Visa. If it’s not many, they may expand the experiment. If they lost a lot of customers, they will want to make a deal with Visa.

In their press release back in June Walmart said

To ensure we are taking care of our customers’ best interests and delivering on our promise of saving customers money, we constantly work to reduce our operating costs, including credit card fees.

Are they really taking care of your best interests? Of course not. They are a business, and their objective is to make money for their shareholders, not look out for your best interests.

If Walmart really wants to save me money, and if they really think credit card fees are too high, why don’t they offer me a discount for paying with cash or a debit card?

The fees that a merchant pays when I use my debit card are very low, about 2 cents per transaction. So if I buy $100 worth of stuff on my Visa card Walmart might have to pay $2 in fees, but if I use my debit card they may have to pay 2 cents in fees. That’s practically nothing, and probably less than the cost of counting the cash and hauling it to the bank, so both cash and debit have virtually no cost for Walmart.

So why doesn’t Walmart offer me a 2% discount if I pay by cash or debit? If it’s all about saving money they should. They should pass the savings on to me.

But they don’t.

Why?

Because it’s not about saving me money. It’s about Walmart making money.

They don’t want to encourage me to pay with cash or debit, because there’s no extra profit in them for that.

They want to encourage me to use their own Mastercard, where they save the Visa fees and earn extra money from Mastercard fees and interest they can charge me, the customer.

Walmart is implying that by lowering Visa fees they will pass the savings on to me, the customer, in the form of lower prices, but that can’t be true. If that was true they would already be offering you and me a discount for paying with cash or debit, and they don’t.

So what’s the solution?

One approach would be to add the credit card fee to your credit card bill, so that you could see exactly how much the retailer had to pay to Visa when you used your credit card.

Would you keep using a credit card with a 3% fee just so you can earn 1% in points?

Maybe you would, because as the system works now you pay the same at Walmart, or most other stores, whether you use Visa, Mastercard, debit or cash, so if the cost to me the consumer is the same it’s to my advantage to use my credit card and earn the points.

I would love to see stores start offering cash discounts.

What would happen if every store had a credit card cost machine?

Just like stores have price checking scanners, where you can scan the item to confirm it’s price, what would happen if they had the same thing with credit cards?

You go to the cashier and scan your credit card, and the cashier says “that credit card charges us 3% in fees, so if you pay cash or debit today we’ll split the difference with you and give you a 1.5% discount”. That would be interesting.

Of course that’s not practical, you can’t have everyone scanning their credit cards, and you can’t have a separate discount for everyone.

But the simple solution would be to have a standard discount if you pay by cash or debit.

Every retailer knows, on average, what percentage they pay in credit card interchange fees, so it wouldn’t be difficult for them to come up with a standard cash discount. If store ABC is currently paying 2% in credit card fees, they could easily offer a 1% cash/debit discount, and everyone wins.

The store increases their profit margin by the 1% they are saving, and you the consumer get a 1% discount.

Of course you wouldn’t earn points on your credit card if you paid cash, but at least you, the consumer, would get to decide what’s in your best interests.

If the store gives me a 1.5% cash discount I’d be willing to forgo earning 1% in rewards on my credit card. If they only want to give me a half a percent cash discount, I would probably still use my credit card, but it would be my choice.

Now as regular listeners to this show know, I’m not a big fan of credit cards. They make it too easy to make a purchase, and if you don’t have the cash in the bank to pay the bill at the end of the month you get hit with very high interest charges, and that’s a big problem.

The average person who files bankruptcy or a consumer proposal with my firm owes over $20,000 on their credit cards when they file. The average person also owes money on bank loans and often income taxes, student loans and payday loans, but the largest single category of debt for someone who goes bankrupt is credit cards.

If you don’t use credit cards, you reduce the likelihood that you will go bankrupt. It’s as simple as that.

So here’s my most important piece of advice:

If you use a credit card, they should be a substitute for cash, not a way to borrow money.

I get it. If I’m going to the store to buy something for $1,000, I don’t want to carry $1,000 in cash in my pocket. A credit card is more convenient, and safer because I’m not worried about having my credit card stolen; it’s easy to cancel.

Credit cards are convenient, and if I’ve got $1,000 in my bank account, using a credit card is a good strategy. I pay for the purchase at the store with my credit card, then I go home and transfer the $1,000 from my bank account to my credit card, and I’m done. No risk, and no interest costs.

The problem, of course, is if I buy something for $1,000 and don’t have the money in my bank account. I’m using the credit card as a way to borrow, and that’s dangerous.

Last time I checked the Walmart Rewards MasterCard carries a standard annual interest rate of 25.99%

If I buy something on my credit card for $100 and take a year to pay for it, that stuff just cost me $125. That’s a big cost, and that’s why credit cards should not be used for borrowing.

Here’s my final piece of advice:

You are the boss. You don’t work for the credit card company, or the bank, or the retailer. They work for you. You are the boss, so you should decide how to spend your money.

If a credit card makes sense for you, fine.

If cash or debit is better for you, great.

Do your own research, and make your own decisions. Don’t let any special offers or discounts entice you into getting a credit card you don’t want, to buy something you don’t need, at a cost you can’t afford.

You are the boss.