Our knowledgeable team of Licensed Insolvency Trustees provide information and expert advice to help you on your way to becoming debt free. Our blog includes podcasts, videos, articles, case studies and Industry Insights about consumer proposals and bankruptcy in Ontario as well as personal finance, credit rebuilding and other money management tips for anyone looking to get out of, or stay out of, debt.

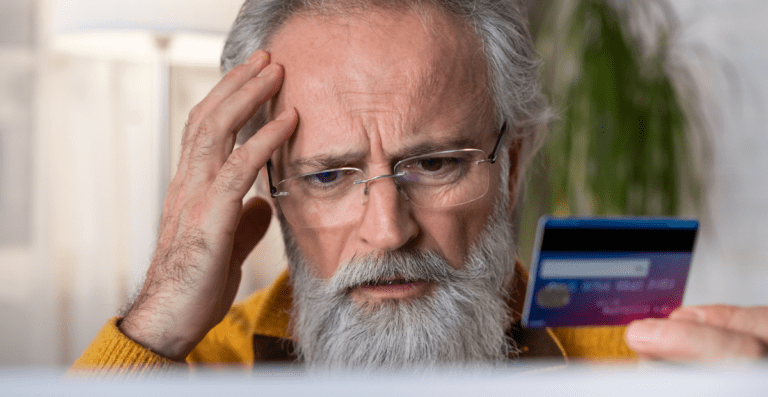

As a credit cardholder, one of your most important financial challenges revolves around credit card debt management. Your goals should be to keep outstanding balances low, avoid high interest rates, and pay your minimum payments... Read more »

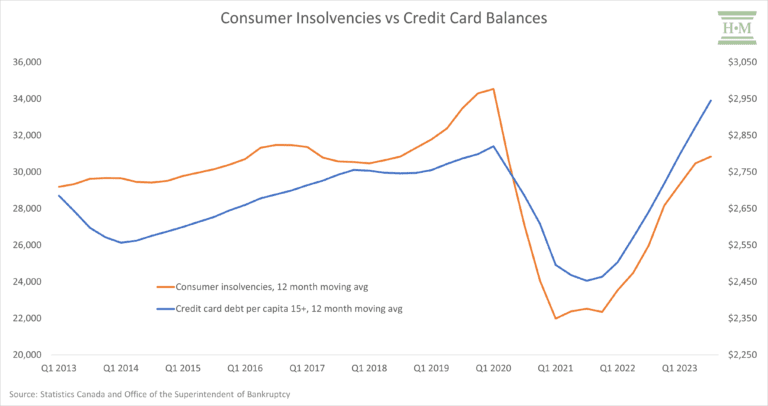

Hoyes, Michalos has been tracking and reporting on homeowner insolvencies since 2007. Our homeowner insolvency index peaked in 2011 at 29.1% and has fallen steadily, reaching a low of 1.6% in 2022 and rising to... Read more »

For Canadian homeowners, the mortgage renewal process is a significant aspect of their homeownership journey. While the prospect of mortgage renewal brings the promise of negotiating better terms, it doesn’t always go smoothly. Around 3%... Read more »

On March 10, Reddit exploded with reports of old City of Ottawa debts mysteriously appearing on credit reports. Based on reporting from CBC Ottawa, on January 12, 2024, the City of Ottawa signed a five... Read more »

Dealing with financial challenges often involves navigating through a web of debts, each with its own rules and consequences. Secured and unsecured debts pose different considerations, and understanding how a consumer proposal affects secured debt is crucial for anyone contemplating this debt relief option.

Consumer proposals in Canada are a debt relief solution for individuals drowning in debt, offering a structured plan for financial recovery. In this article, we'll explore how a consumer proposal works, explaining eligibility criteria, the filing process, legal protection, creditor considerations, and the pros and cons of this debt management strategy.

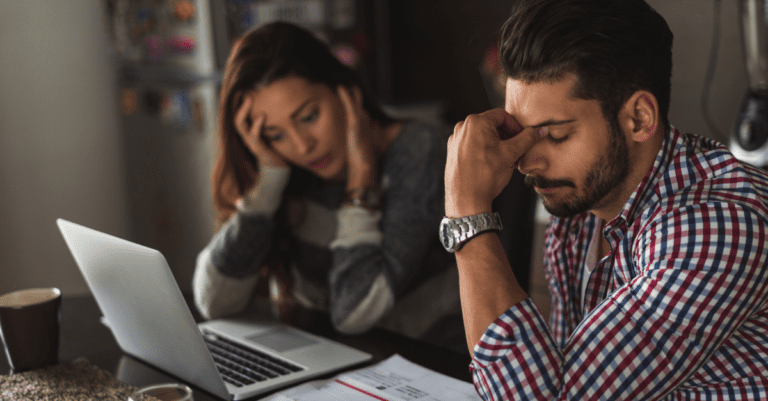

The past year has seen a steady erosion in financial stability for Canadian debtors. The result is that consumer insolvencies are rising rapidly. In my year-end post, I will outline what is behind the average Canadian debtor's re-accumulation of consumer credit and how that will impact consumer insolvency levels in the coming year.

The past year has seen a steady erosion in financial stability for Canadian debtors. The result is that consumer insolvencies are rising rapidly. In my year-end post, I will outline what is behind the average Canadian debtor's re-accumulation of consumer credit and how that will impact consumer insolvency levels in the coming year.

A payday loan may be tempting, especially when you are in need of an emergency expense but beware! They do more harm then good and can put you into serious debt. Doug Hoyes explains the pros and cons of using payday loans for emergencies.

A consumer proposal is an affordable way to eliminate overwhelming debt. While there is a fee to file, these fees are included as part of the proposal process. Doug Hoyes explains the costs of a consumer proposal and how payments are calculated to fit your budget.

No one wants to be a fraud victim. It causes tremendous stress and we have also seen it lead to serious debt problems in some cases. In this post, learn how fraudsters use tricks and deceptions to steal your hard-earned money so you stay protected.

In Canada, there are both bankruptcy lawyers and licensed insolvency trustees that can help with different types debt-related issues. In this post, Maureen Parent explains the key differences and who can help you depending on your situation.

Revolving credit means credit cards and lines of credit. You probably use it everyday but it's important to understand all of its benefits and risks so you avoid financial trouble. Doug Hoyes explains in this post.

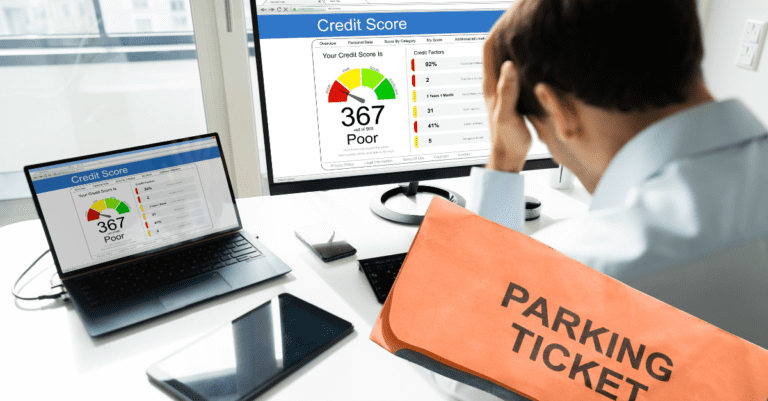

You're probably familiar with Canada's credit bureaus already. After all, they provide you with your credit report. But how do credit bureaus collect your information and what more should you know about credit reporting agencies? Scott Schaefer explains in this post.

We frequently meet with individuals who have a car loan. In this post, Doug Hoyes explains how a car loan is treated in a consumer proposal, whether you wish to keep your car or not.