No, you do not lose everything when you file for bankruptcy in Canada. There are assets you can keep even if you go bankrupt. These are known as bankruptcy exemptions. Some exceptions to what you surrender in a bankruptcy are provided under federal law, others by provincial legislation. Ontario bankruptcy exemptions are set out in the Execution Act of Ontario.

Bankruptcy Exemptions in Ontario:

For individuals, the following are exempt from forced seizure in a bankruptcy:

All necessary clothing for you and your dependents with no dollar limit

Household furnishing and appliances up to $14,180

Tools and property used to earn a living to a maximum of $14,405

One motor vehicle not exceeding a value of $7,117

Equity in your home if that amount is less than $10,783

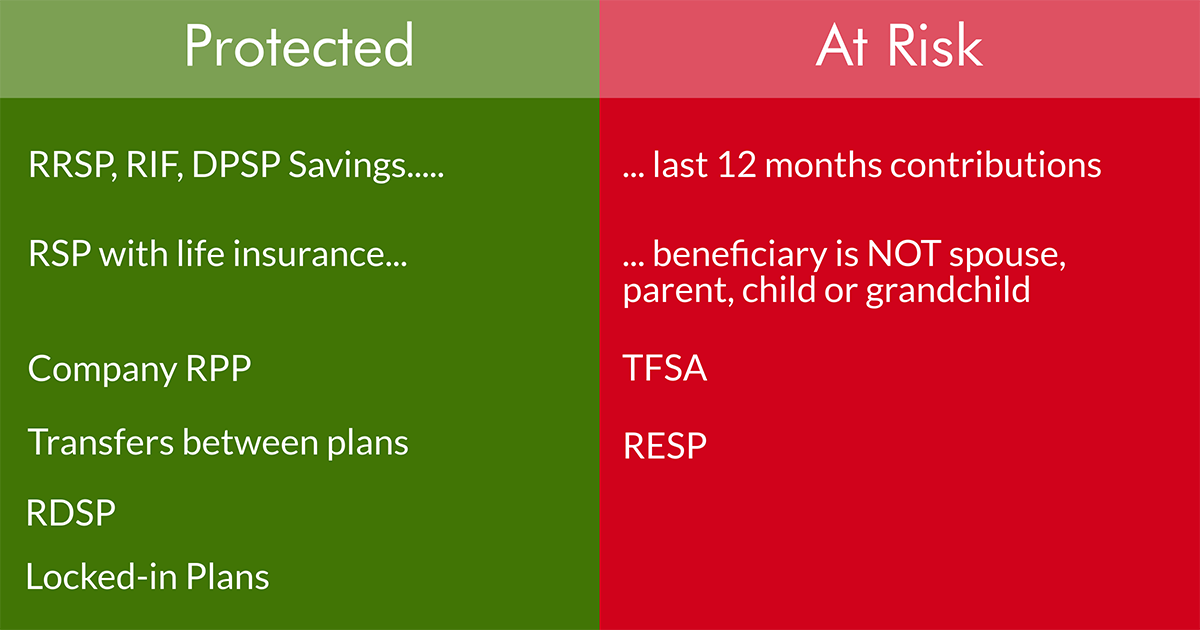

RRSP and RRIF savings, except contributions made within the last 12 months

It is important to understand that the prescribed limits set out by Ontario law are based on resale value on an as-is basis. Your work tools for example are likely used, and have wear and tear. For bankruptcy purposes, they are valued based on what they would sell for as-is, not based on replacement value.

The same valuation applies to your vehicle. You can keep one vehicle (a car or truck), up to the set value limit. This is based on what you could sell the car for. The trustee will usually use the black book value to estimate the value of your vehicle and determine if it is exempt.

There is a financial cost to bankruptcy, and it’s different for every person who goes bankrupt. That’s because the government has decided that the more you earn and the more you own, the more you have to pay to your creditors. First let’s look at the cost based on your income. The government knows you need income to live on, so they allow you to keep a portion of your income for living expenses. The amount you get to keep is based on your family size, the bigger your family the more you get to keep. Earn income over this threshold and you have to pay half of this surplus income to your creditors. The second cost of bankruptcy is based on the assets you own. In a bankruptcy you don’t lose everything, just like with your income, the government created rules of what you can keep and what your creditors can have. The rules differ by province, but in Ontario you can keep most personal possessions and household furnishings, tools you need for work, 1 motor vehicle depending on its value, most pension and RRSP savings except recent contributions to an RRSP. There are dollar limits on the value of assets you keep, but in most cases, people find the limits high enough to protect their basic belongings. Your creditors are entitled to any equity in your home, investments and other assets, RRSP contributions you have made in the last year, tax refunds you might be entitled to up to the year you go bankrupt. If you have a lot of assets or a high income you should talk to your trustee about a consumer proposal. You can negotiate a plan to settle your debts and keep your assets. If you don’t have any assets and don’t earn any income, you might not even have to file bankruptcy. But if you do, you will need to make payments to cover the cost of administering your bankruptcy. Your situation is unique, to get an estimate of what your bankruptcy might cost, please call or email us to arrange a no charge initial consultation with a Hoyes Michalos professional.

It is still possible to keep your car, truck, work tools, and other assets valued over any exemption limit. You can make an arrangement to ‘buy back’ the value over any exemption limit from the trustee. This amount is added to the cost of your bankruptcy.

Questions About Bankruptcy and Exempt Assets

What happens to my wages in bankruptcy?

You keep your wages in a bankruptcy. You will be required to submit proof of income and expenses monthly to your trustee. Your trustee will use this to determine your average net income for the purposes of calculating “surplus income”. If your income exceeds the government set threshold limit, you will be required to make surplus income payments during your bankruptcy. If your wages are being garnisheed, bankruptcy will stop most garnishments.

Can I keep my bank account if I’m bankrupt?

We strongly advise anyone considering bankruptcy to open a new bank account at a different bank prior to declaring bankruptcy. This will avoid the risk of your bank seizing funds for unpaid debts once you file.

While any funds in your bank account are not exempt assets, typically you are allowed to keep a small amount of cash on hand in your new bank account to cover living expenses like rent, food, etc. for a short period of time.

What happens to my tax refunds?

Your licensed insolvency trustee will file two tax returns for the year that you declared bankruptcy:

a pre-bankruptcy return (Jan 1 – day before bankruptcy)

a post-bankruptcy return (date of bankruptcy – Dec 31)

Any tax refunds applicable to the date of bankruptcy and on your post-bankruptcy return will be sent to the trustee. Any taxes owing on your pre-bankruptcy return are included in your bankruptcy. Any taxes owing on your post-bankruptcy return must be paid by you. While you lose your income tax refunds, you keep your HST cheques and Child Tax Benefits.

Can I keep my leased vehicle?

Leased vehicles are treated differently than owned vehicles. Technically you do not own your leased car. You have the right to use the car in exchange for your obligation to make lease payments. If your lease payments are current, you can keep your car, no matter the value. You can, if you prefer, also surrender your leased vehicle and include any shortfall debt as a debt to be eliminated in your bankruptcy. This is a good option if you can’t afford your lease payments.

Can I keep my house if I file bankruptcy?

In Ontario, you keep your house in bankruptcy unconditionally if the equity in your home is under $10,783 and your mortgage payments are current. Above that amount, you can arrange to buy back the equity in your home.

What happens to my RRSP in a bankruptcy?

You keep all RRSP, RRIF and DPSP (Deferred Profit Sharing Plan) savings except contributions made in the 12 months before your bankruptcy. RESP, TFSA and other investment savings are not exempt. Read more about this asset in our post: RRSP and bankruptcy law in Canada

What about lottery winnings, inheritances and other windfalls?

Inheritances received, or due to you, as a result of the death of someone during bankruptcy become an asset of the bankruptcy.

Lottery winnings and similar windfalls received during your bankruptcy also vest in the trustee for the benefit of your creditors.

Bonuses and commissions from employment would be considered income and not subject to seizure by the trustee however they will impact the calculation of surplus income.

File a Consumer Proposal and Keep Everything

If you have assets that may be subject to seizure in a bankruptcy because they are not exempt, or because their value exceeds the permitted exemption limits, you may want to consider a consumer proposal as an alternative to bankruptcy.

The most important thing to realize is that you do not lose all your assets if you file bankruptcy in Canada. If you do have assets that must be surrendered to the trustee, you still have options like a consumer proposal to keep those assets.

To discuss your specific situation, contact us to talk to a Licensed Insolvency Trustee about how your assets may be treated in a bankruptcy and if a consumer proposal is a better way to preserve any assets you may wish to keep.

Do I lose my RRSP or pension if I file bankruptcy in Canada?

Many people are worried that if they file personal bankruptcy they will lose their RRSP and other pension savings.

In Canada, most Registered Retirement Savings Plans (RRSPs) are protected in bankruptcy and so, in general, you can keep your RRSP savings after filing bankruptcy.

The Bankruptcy and Insolvency Act (BIA) under section 67 (1) (b.3) exempts RRSPs from seizure for your creditors except for any contributions made within the last 12 months.

The BIA also states that creditors are not entitled to any assets that are exempt from execution or seizure by provincial law. In Ontario:

A Registered Pension Plan is governed by the Ontario Pension Benefits Act is exempt from seizure in a bankruptcy. Ontario protects company-sponsored or government-sponsored registered pension plans (RPPs). All pension assets under these plans are protected, regardless of when the contribution was made. Both employer and employee contributions are safe from seizure.

The Insurance Act of Ontario protects RSPs that have a life insurance component if the beneficiary is a spouse, parent, child, or grandchild. In this case, all contributions are safe.

Let’s look at three common examples:

Example 1: Your employer takes 5% of your pay and puts it in a registered company pension. All contributions are yours to keep, even those made within the last year and those matched by your employer.

Example 2: You have a Registered Retirement Plan with an insurance component with a company such as Sun Life and your spouse is a beneficiary. These plans are yours to keep, including contributions made in the last year.

Example 3: You contribute 3% of your pay every payday to your own individual RRSP through an automatic savings program. Contributions made to your RRSP in the last 12 months before filing bankruptcy are at risk of seizure by the trustee.

The trustee cannot be granted any more rights to assets in the plan than the plan holder, including for recent payments. If the plan contains terms that prevent the plan holder from requesting payment until a specific event such as termination, death, or retirement, the trustee is not entitled to seize what the plan holder cannot withdraw.

What about transfers between RRSPs?

A transfer is not the same as a contribution. If you transfer funds from one RRSP to another company, then these are not new contributions in the last 12 months and as such cannot be seized by your trustee.

What about a spousal RRSP and bankruptcy?

The BIA applies to RRSPs you own and control. If you file bankruptcy, contributions you made to your spousal plan are not subject to seizure by the trustee. If your wife goes bankrupt, the maximum exposure for her spousal RRSP is the contributions you made in the last 12 months.

What about a RRIF and bankruptcy?

A Registered Retirement Income Fund (RRIF) is treated the same as an RRSP. Normally individuals withdrawing funds from a RIF are not making current contributions, however if they do, their maximum exposure is contributions made within the past 12 months.

Bankruptcy law in Canada protects RRSP savings. Only the last 12 months contributions are at risk. You can ‘buy back’ recent contributions from the trustee. In a consumer proposal you keep all assets, including recent contributions. Don’t drain RRSP savings to repay large debts. Talk with a Licensed Insolvency Trustee about your options.

While there is no specific provision in the BIA to deal with a Registered Disability Savings Plan (RDSP), a recent British Columbia Supreme Court ruling held that funds in a RDSP cannot be seized by a Licensed Insolvency Trustee in a bankruptcy for the benefit of creditors.

What happens to a DPSP and bankruptcy?

A Deferred Profit Sharing Plan (DPSP) is treated the same as an RRSP in a bankruptcy. The maximum exposure is any contributions made in the last 12 months. Most DPSP plans have terms that the employee cannot withdraw these funds while still an employee for that company, therefore the full amount in the DPSP could be protected.

Locked-in pension plans

Pension plans that are designated as a Locked-In Registered Plan are exempt from bankruptcy or seizure. The trustee has no entitlement to money in this plan, including recent contributions.

What about TFSA and bankruptcy?

While a Tax-Free Savings Account (TFSA) is a registered savings vehicle, it is not a RRSP and as such is subject to seizure.

What happens to an RESP if I file bankruptcy?

Because the plan holder (usually the parent) can cash out a Registered Education Savings Plan (RESP) at any time, an RESP is considered to be an asset of the plan-holder. Therefore, if the plan-holder is bankrupt, an RESP is subject to seizure by the trustee.

Tips to protect at risk assets even if you go bankrupt

In truth, most people who are considering personal bankruptcy have ceased to make any contributions to their RRSP because they are using most of their income to make debt payments. However, if you do have exposure to recent contributions here is how we advise clients.

Our first step is to review your RRSP documents to determine how much you have contributed in the last 12 months. If you contribute through your paycheque at work we can generally get this information from your paystub. If you have an RRSP through a bank or investment advisor, they will provide a statement.

If you have made no contributions in the last 12 months, no further action is required; you can keep your RRSP.

If you have made contributions in the last 12 months or have other seizable assets like RESPs, you have three options:

You may request that the trustee contact the bank or investment company and withdraw the contributions from the prior 12 months. It is the trustee’s responsibility to pay the tax owing on that withdrawal, so you have no further costs or obligations.

You may decide to contribute an extra amount to your bankruptcy to “buy back” your RRSP contributions for the last 12 months. For example, if you have contributed $1,000 and you are in a 30% tax bracket, the trustee would recover a net amount of $700; so you could pay the trustee an extra $700 and keep the full amount of your RRSP. The same applies to any assets you have in an RESP or TFSA. A payment plan matching the term of the bankruptcy can be arranged.

If you have significant seizable assets, you could decide to file a consumer proposal. In a consumer proposal you don’t lose your RRSP or any assets.

As a final planning point, if you are not worried about having your wages garnisheed, you could stop contributing to your RRSP now while you catch up on rent, utilities or other current bills, so that contributions in the last 12 months are reduced.

Protect your retirement from bankruptcy

One of the most common, and costly, financial mistakes we see is people who drain their RRSP savings to keep up with debt payments when they are in financial trouble.

If you have significant debts, draining your RRSP (a protected asset) to fund debt obligations only serves to delay the inevitable. You should not use your RRSP savings to pay down debt without first speaking with a Licensed Insolvency Trustee about your options. Since RRSPs are protected in a bankruptcy, it makes sense to preserve these funds for your retirement.

Everyone thinks that a house provides both stability and financial security, but on today’s show, I’ll explain why that is not always the case. I’ve meet with thousands of homeowners over the last 20+ years who have filed a consumer proposal because their home started their downward debt spiral.

It is true that if you live in the same home for many years, you have stability. However today we are relying on our homes increasing in value enough to cover off any debts we accumulate. Here’s the one underlying problem with that assumption: real estate prices are both unpredictable and volatile.

If you purchase more home that you can afford you risk building up debt. Living expenses and other housing costs often get paid through the use of credit card debt when your mortgage takes such a big piece of your income. And there is no guarantee that the rising price of your home will bail you out.

Even if you manage your debt levels, life happens and not always they way we expect.

What happens if you change your job and this requires you to move? You pay real estate commissions when you move, but you also pay a penalty to break a fixed mortgage if you rent in your new location. And you have to pay moving costs. The true cost of selling your home and breaking your mortgage can be a lot higher than you expect. Even when rates are rising, if house prices are not increasing, the penalty to break your mortgage and closing costs can eliminate the profit on your house.

What happens if you lose your job? Can you afford to keep up with your high mortgage payments? If you have other debts this can sometimes be a problem. Refinancing is an option for some but it’s not an option for everyone. There is no guarantee that getting a second mortgage will solve your debt problems.

My point is, buying a home is not a financial certainty. Don’t let FOMO force you into a decision to buy a home assuming that it will provide you with financial security down the road. It may, but the decision to buy can also be just the beginning of your debt problems.

As everyone who listens to this podcast knows, last month I published a book called Straight Talk on Your Money. Federal law requires me, as a licensed insolvency trustee, to keep notes on my discussions with clients if they decide to file a consumer proposal or bankruptcy. I’ve met with somewhere between 10,000 and 20,000 people over the last 20 years, and a few years ago I started going through my notes to see if I could figure out the most common causes of money problems. I picked the top 22 myths and mistakes people make, based on my experience talking to my clients, and that became the book.

So guess which three chapters have generated the most controversy?

Guess which three chapters are most likely to come up when I’m interviewed in the media?

It’s the three chapters on real estate.

Real estate has almost become like a religion for many people in Ontario. Real estate prices have been going up for years, so people naturally assume that they will go up forever.

I’m not a real estate expert, so I’m not going to attempt to forecast the future price of real estate.

What I do know is that real estate prices are both unpredictable and volatile.

As I record this in October, 2017, real estate prices in Ontario peaked in April, dropped through the summer, and then depending on who you listen to in September they stopped falling as fast, or stabilized, or have started to recover. I don’t know. And neither does anyone else really.

What I do know is that, over the years, I have met with hundreds of people who spent too much on a house, and ended up getting into financial trouble.

When I ask people why they bought the house that they did, they give me many answers, but the most common answer is something like: “house prices go up, and I don’t want to waste my money on rent”; I’ll come back to that opinion in a future show, but there’s another reason people give for buying a house, and that’s the reason I want to talk about today.

My clients tell me that they bought a house because they wanted financial security, and stability.

That reason does make some sense.

I know lots of people who were renting, and then the landlord decided to sell the house, so they had to find another place to live. I know the Ontario government is looking at changes to the law that would prevent landlords from easily booting renters out of the house when they want to flip it, but regardless, if you sign a one-year lease, there’s no guarantee that the landlord will renew your lease at the end of the term.

Having to pick up and move is very disruptive.

Sometimes it’s simple things, like you have a dog or a cat, and it’s harder to find a place that accepts pets.

It’s even harder if you have kids in school. It’s disruptive if you can’t find a new place in the same school district, so now not only are you dealing with a house move, but you are also dealing with a school move.

And what if you have physical limitations? It’s more difficult to find a place if you need an apartment that is wheel chair accessible, or a house that is on one level so you don’t have to deal with stairs.

And it’s for reasons like those that people like to buy a house, instead of renting.

They can buy a house and know that no landlord can force them to move.

They can stay in the same school district for as long as they want.

They can do renovations to the house to make all the rooms accessible if they have physical disabilities, and the landlord can’t force them to move.

In simple terms, owning a house gives you stability.

It also gives you financial security, because once you do the renovations, that’s it. There’s no worry about needing to put in another wheel chair ramp to the front door ever again. Once it’s done, it’s done.

This all sounds great. Obviously if you have a pet, or kids in school, or if you have special needs, owning a house is the way to go. Maybe you just like to paint the walls whatever colour you want. Owning is better, because then you don’t have a landlord telling you what you can and can’t do.

We can argue over if real estate prices will go up or down in the future, but no-one can argue with the fact that a house gives you stability and financial security.

Well, sorry to burst your bubble, but there is another side to this story.

Stability is great, when you want stability, but sometimes flexibility is more important than stability.

I want to tell you a story, but before I do, let me refresh your memory as to what happens when you sell a house.

When you sell a house you have to pay real estate commissions, and legal fees, and, if you have a fixed or locked in mortgage, you have to pay a penalty to break the mortgage.

If you sell one house and buy another one, and the mortgage lender lets you port your mortgage from the first house to the second, you may not have to pay any penalties, but if you are going to sell your house and not buy another house, the penalties to break a mortgage can be substantial.

Most mortgages have, at the very least, a “three-month” penalty, where you are required to pay the interest for the next three months.

But most mortgages also have an “Interest Rate Differential” penalty, or IRD. When you break the mortgage and sell the house, the bank gets their money back, but since they had planned to lend it to you for the next 25 years, now they must find someone else to lend it to, since you broke the deal with them.

Now you may think, no problem, the Bank of Canada raised their benchmark interest rate by a quarter of a point in both July and September, 2017, and as a result mortgage rates have also increased, so if interest rates are higher now than when you borrowed the money, the interest rate differential is in the bank’s favour, so no problem. You wouldn’t have to pay any penalties.

That would make sense. Let’s assume you borrowed at 2.8%, and the current interest rate is 3%, so if you pay off your mortgage the bank can take your money, and instead of lending it to you at 2.8%, they can now lend it to someone else at 3%, so the bank is actually going to make more money now that you have paid off your mortgage, so great, no penalty.

That does make sense, but it doesn’t always work out that way, even when interest rates are rising.

Here’s why.

Some banks calculate the Interest Rate Differential not based on your actual rate, but on the posted rate.

So if, when you got the mortgage originally, the posted rate was 3%, but the bank “gave you a deal” and gave you the mortgage at 2.8%, the penalty will be calculated based on the posted rate back then, and the posted rate today, which may not be the actual rate.

So even though you got a five-year mortgage at 2.8%, and that was three years ago, so now you want to break it with two years left, and even though a borrower could negotiate a rate of 3% today, which is higher, so there should be no penalty, the bank may use the posted rate back when you got the mortgage, which was 3%, and the posted rate today of 2.9%, which is lower, so you end up paying a penalty.

See what happened there? The bank played a game, and switched the rates on you, so the Interest Rate Differential calculation works out in their favour. Even if rates are rising, they still win!

Now I know you are thinking I’m making this up, but I’m not. I’ll include a link in the show notes over at hoyes.com to a blog post written by a mortgage broker that gives some examples from one of the big banks, so you can see that this can happen.

So to summarize: when you sell a house and break a mortgage early, you suffer any drop in the value of the house, but you also pay real estate commissions, legal fees, and you may have to pay a substantial penalty to break your mortgage; it’s not just a three month’s interest penalty; the interest rate differential penalty could have you paying a substantial penalty to break your mortgage.

With that background, let me tell you the story of Jim.

He bought a condo when he was working in Toronto. Then, six months later, he was offered a great job in London, Ontario. It was too good an opportunity to pass up, but he knew he couldn’t commute every day from Toronto to London, and he couldn’t afford to keep two places, so he called his real estate agent about putting the condo up for sale. The agent told him that prices had dropped slightly from when he bought it, but no problem, they could still sell it quickly. The agent told Jim that prices had dropped about 2%, but Jim would also have to pay a 5% real estate commission, and because he had a locked in mortgage, he would have to pay a penalty to break the mortgage.

Jim did the math.

He paid $500,000 for the condo, and he could sell it today for $490,000, so that’s a $10,000 loss.

His real estate commissions would be $24,500.

The penalty to break the mortgage, because he was only 6 months into a 5 year fixed rate mortgage, would be another $10,000, mostly due to the interest rate differential calculation.

Not including moving costs, selling the condo would cost Jim almost $45,000.

Jim doesn’t have $45,000 sitting around, so what does he do?

Keep the condo in Toronto, and try to rent it out, and then wait to sell it when the mortgage comes up for renewal? Jim doesn’t want all of the hassles of being a landlord, particularly with him living two hours away, so he doesn’t like that idea.

He could buy another place in London, and if he can port his mortgage from his place in Toronto to the new place in London he can save some or all of the $10,000 fee to break the mortgage, but he’s still stuck with the real estate commissions and the loss on his place in Toronto.

What would you do?

Over the years I’ve helped lots of people like Jim, and in a lot of cases they decided to NOT take the new job, and keep the house and the job they’ve got, because the cost of selling the house and moving is just too much.

I understand. Paying a $45,000 penalty to take a new job in a new town is a lot of money. Even if the new job pays $10,000 a year more, it will still take Jim many years to “break even”.

And that, my friends, is why owning a house does not guarantee financial security. In fact, owning a house can do the exact opposite.

Owning a house can act like an anchor, keeping you in place when you want to move on.

Because Jim owned a house, he was not able to take a new, more challenging job. He is stuck.

So how do you decide if you should own or rent a house?

First, and most obviously, crunch the numbers. The cost of a house is more than just the mortgage payment, so consider all costs when making the buy vs. rent decision.

Second, consider your future. Pull out your crystal ball and ask yourself this simple question: what are the chances that I will want to move in the next few years. Will I want to get a new job? Will I be getting married, or will I be starting a family that will require a bigger place?

If you are already married with three kids and unlikely to be having any more, and if you have a stable job that you love and you have no intention of looking for another job, the risk of owning a house is a lot less for you. Owning a house may be the correct answer for you.

But, if you are in a job that is not stable, or you are in an industry that is not stable, tying yourself down with a house may not be a wise decision.

To summarize: the decision on if you should buy a house is not just a guess on whether or not real estate prices will go up in the future. Even if house prices do go up, owning a house could be a bad decision for you if you want to move, so it’s very important to consider how your future may unfold.

That’s our show for today.

More information on real estate, and links to everything we discussed today, and a full transcript can be found at hoyes.com, that’sh-o-y-e-s-dot-com

And if you want to read those three controversial chapters on real estate, my book is called Straight Talk on Your Money, and it’s available in better bookstores across Canada, and on Amazon, Indigo.ca, and as an audio book.

Thanks for listening, until next week, I’m Doug Hoyes, that was Debt Free in 30.

Joint or shared ownership in a family cottage is not uncommon. When one co-owner faces significant debts, enough to consider filing for bankruptcy, this raises substantial concerns with other owners about keeping the cottage “in the family”, and out of the hands of the bankrupt’s creditors. This is not an unusual scenario in our Toronto bankruptcy offices. This post will explain how the realization process works in a bankruptcy and what options you and your co-owners have if you wish to retain possession of a cottage, but file insolvency to eliminate your personal debts.

Bankruptcy and Real Estate

When someone files bankruptcy, their trustee is required to realize on all non-exempt assets to pay their creditors. This includes real estate, including a personal residence or cottage, whether it is owned solely by the bankrupt or jointly with a spouse, siblings, or other partners.

There are rules in Ontario that allow the bankrupt an exemption for principal residence if, and only if, the total equity in the property is less than $10,783. Not many properties fall into this category. However, in terms of your home, there are options that can allow you to keep your home even if you file bankruptcy.

Determining Fair Market Value of the Cottage

The first thing the trustee will do is determine the fair market value of the property. They will request an independent appraisal, and then deduct prior charges like mortgages and outstanding property taxes that would have to be paid if the cottage was sold. After these deductions, the equity in the property will have been determined.

If the bankrupt owns the property on their own, then this equity belongs to the creditors in full. If a property is owned jointly, or partially, the amount due to the creditors would be equal to the bankrupt’s share in the property.

Realization of Equity in Bankruptcy

Rarely are properties sold by the trustee. In the case of a jointly-owned cottage there are options:

Once the equity is determined, a negotiation will usually take place to sell the equity to the non-bankrupt owners or a third party. If the sale or amount is contentious, the trustee may obtain court approval of the sale. No one wants to take the family cottage away; the objective is to obtain the equity to pay the creditors.

Fraudulent Transfers

There are rules that prevent a person selling or transferring a property for less than fair market value on the “eve” of filing a bankruptcy. The courts will overturn and reverse these transactions. Selling or gifting your share of the cottage to your siblings to avoid having the asset realized in a bankruptcy is not advised. The bankrupt is required to answer questions about pre-bankruptcy sales of assets and could be charged with fraud if they provide false information on their bankruptcy forms.

Consider a Consumer Proposal

If the bankrupt wishes to retain ownership of his or her share of the family cottage, they could file a consumer proposal. In a proposal, the debtor maintains ownership and control over their assets. In exchange, they make a settlement offer that their creditors can agree to accept, or not. If the proposal is accepted, the debtor has a contract with his creditors to settle their debts.

As you can see, there are options to allow you and your family to retain ownership of a cottage or any shared asset even if one party needs to turn to bankruptcy to solve other debt problems.

In some cases it’s your fault, if your debt was a result of reckless spending but, in my experience, most people get into trouble because “life happens”. Many of my clients have debt problems caused by a job loss, or reduced income, or a life event like a relationship break-down or a medical condition that forces them to take time off work.

Whose Fault is it anyway?

If you, or someone you know, has serious financial problems, is it your fault?

The conventional wisdom, of course, is yes, if you have problems, it’s your fault.

In some cases, this is obviously true. If I stay up all night watching TV, and sleep in in the morning, and keep showing up late for work, and get fired, it’s hard to blame anyone else but me for getting fired.

If I rack up my credit card on a wild spending spree buying stuff I don’t need, again, it’s obvious that my actions are causing my debt.

But is it crazy spending that causes most financial problems?

Let’s step back a minute and look at some common definitions.

We often use the words ‘fault’ and ‘cause’ interchangeably.

‘Fault’ means to be responsible for a failure or wrong act.

‘Cause’ means something happens in such a way that something else happens.

My behavior might be the cause of my financial problems. It’s my fault. But it’s also likely that something else is the cause.

In other words, your financial problems may not be your fault.

Why is this even important?

Why does it matter whose fault it is if you have money problems?

It matters, because you can only fix what you can control. It is not productive to blame yourself for events beyond your control.

If I’m stopped at a red light and my car gets rear-ended, it’s clearly not my fault. There’s no point in blaming myself for my bad luck. Of course, I still have to deal with the outcome. I still have to take responsibility to get my car fixed, but it’s not my fault. My actions were not the cause of my car accident.

So back to the question about what causes a lot of financial problems.

Let’s pause and listen to Mary’s story. This is not one person’s story; it’s a combination of many people’s stories, and it’s based on typical people that I meet with all the time. This isn’t really Mary’s voice; I’ve asked someone to read it, but I think it paints the picture rather nicely.

Here is Mary’s story.

Mary’s Story (to be read by a female voice over artist):

My name is Mary. I’ve always believed in working hard. I was raised by a single mother, so money was always tight, and all through high school I worked part time jobs after school and on weekends.

I took a year off school after high school to work and save money, so I could build up some savings for university. I also qualified for some scholarships and grants. I worked hard to keep my scholarships, and this, combined with working part time, meant I was able to graduate from university with only $20,000 in student loan debt.

Unfortunately, after graduation I wasn’t able to find a job in my field, but I was able to find a job as a part-time, unpaid intern, which helped me gain some practical experience. I continued working nights and weekends at my part time job to make ends meet.

Finally, a year after graduation, I was hired, full time, in my field. I was thrilled!

The job involved travel within my city, so I needed a car. I did a lot of research, and decided to finance a new car, so that I would have a full warranty, so I wouldn’t have to worry about unexpected repair bills. My car payments were $400 a month, and because I was a relatively new driver in a big city my car insurance was $250 a month, but with my salary I could afford it.

Six months after I started working full time I was required to start making payments on my student loan, but that was OK, I was earning decent money. With my rent and car expenses and student loan payments cash was tight, but I was able to scrape by.

I was keeping my head above water, but then a major storm caused the drainage system in my apartment’s underground parking garage to back up. My car was severely damaged by the flood. That started a long dispute between my car insurance company and the insurance company for the building as they fought over who was responsible for the damage. I needed a car for work, so I used my credit card to pay for the extensive repairs, in the hopes that eventually I would get the money from the insurance company. The repairs, including a new engine, took four weeks, and I had to pay for a rental car while the repairs were being done.

Then I got even worse news: my employer was filing for bankruptcy protection. As one of the newest employees, I was laid off.

I’m a fighter, so I immediately started looking for a new job, and I went back to work at my old part time job. However, with no severance pay, and with the waiting period for unemployment insurance to start, I had to use credit to survive.

It took six months, but I was finally able to find another job making a bit less than I was making at my previous job.

In the meantime, the insurance company eventually agreed to pay for most of my car repairs, but not the rental car because they said that wasn’t part of the deal.

I’m now back at work, but I owe a lot on my credit card for the money I borrowed while I was off work, and I’m also behind on my student loan payments.

That’s Mary’s story.

Today, Mary has a job, but she owes around $20,000 on her student loan. She still has her car loan, and owes big money on her credit card.

So back to today’s question: whose fault is it?

Is it Mary’s fault that she owes money on her student loan and credit card?

Obviously, Mary was the one who borrowed the money, so legally she is responsible for the debts. There’s no doubt about that.

But, in hindsight, what could Mary have done differently?

I guess she could have chosen not to live in an apartment with underground parking that might have a water leak and might flood, but how could anyone reasonably anticipate that?

I guess she could have tried to find a job at a company that wouldn’t go bankrupt, but again, it took Mary a year to find that job, so how can she be blamed for taking the best job she could find?

The point is that Mary did everything right.

She took a year off before going to university to save money, so she could graduate with only a $20,000 student loan. That’s actually pretty good, because as we discussed back on episode #158 in September, the average student loan debt resulting from a four-year degree program in Canada is over $26,000, so Mary actually did a lot better than the average student loan debtor.

The conventional wisdom is that, with low interest rates, it’s better to finance a new car, with a full warranty, than to buy a used car, with no warranty, and with no dealer incentives you are likely to pay a higher interest rate at the bank. Mary followed the conventional wisdom, financed a new car, but in the end the repair costs and the loan payments became a burden.

It’s also not her fault that her employer went bankrupt.

The point is that life happens, and not always in the way that we hope or expect.

Often people have financial problems through no fault of their own.

I know, from our Joe Debtor study, that our average client has income that is around 40% less than the median income in Ontario. With reduced income, debt becomes a way to survive. Debt is not always used for spending on vacations and luxuries; like with Mary, debt is used to pay the bills during periods of unemployment, or while going through a marriage break up, or while recovering from an illness or injury.

Life happens.

So here’s my point: sometimes our financial problems are our fault. If they are, we should recognize the cause of our problems, and take steps to change our behaviour. Reduce your spending, get a second job to increase your income; do whatever it takes.

But if your money problems are caused by events beyond your control, don’t blame yourself. That’s not productive.

Your goal should be to eliminate your debt, and get back on a sound financial footing. Yes you are taking responsibility but the key is to look to the future; don’t focus on the past.

So if you have more debt than you can ever hope to repay, contact a Licensed Insolvency Trustee, like the professionals at my firm, Hoyes Michalos. As government licensed trustees we are required, by law, to assess your situation for free, and explain your options.

We will.

That’s why we say “give us 30 minutes”; in a 30 minute meeting we can understand your unique situation, and explain your options.

The recent interest rate increases from the Bank of Canada will affect many Canadians. But the question of the day is: Do you know how a 1% interest increase will affect your budget?

We tend to think that a 1% increase in our mortgage rate is no big deal but it is. A 1% increase in your mortgage from 3% to 4% actually increases the cost on your mortgage by 33%.

Today’s guest is Brent Hughes, who is here to discuss the impact of higher, or lower, mortgage rates, and how you can calculate the financial impact for your mortgage. There are two times throughout the life cycle of a mortgage that most people receive professional advice: the beginning of the renewal term, and the end. The problem is interest rates are constantly changing during your mortgage term. Brent’s company, Monitor my Mortgage, helps give people the information they need to make the right choices on renewing your mortgage mid-term by notifying you of the impact of a rate change compared to your potential penalty over different mortgage options.

How Interest Rates Affect Your Mortgage

It’s important to look at the big picture when when interest rates change. You need to look at not just the change in your monthly mortgage payment but how much more (or less) you will be paying over the lifetime of your mortgage. At renewal time that might be easy. You sit with your mortgage broker or lender and they can prepare a new amortization table to tell you the differences between your current mortgage rate and the rate you might get on renewal.

But what about mid-term changes?

If you want to take advantage of rate changes mid-term you must factor in your penalty. A variable penalty is usually about three months interest. But penalties vary by lender, some have extra fees written in on top of the rate differential. You have to know your contract and then compare this to any interest savings you might get by renewing at a different rate. Combine this with the fact that there are a lot of different rate options out there & this becomes difficult which is where Brent’s software comes into play.

Things to consider for in-term renewals:

How much longer do you have on your term?

Are rates rising or lowering? If rates are rising you might want to cancel a fixed rate mortgage and renew early. If rates are lowering maybe you want to lock in if you have a variable rate loan.

What’s your current credit look like? If it’s not good right now, it may be wiser to repair your credit before trying to renew mid-term even if rates are dropping since you may not qualify for a lower rate.

Did you change your job recently? A change in your employment situation can affect the way banks look at your situation when it comes time for renewal and might affect the rate you are offered.

Brent recommends constantly monitoring rate changes and the impact on your mortgage. Don’t just wait for your standard renewal date. That’s what his app helps you do. With this information you can make an informed decision about what to do as rates are moving.

Doug Hoyes: After many years of low interest rates, interest rates are now increasing and many experts believe we’ll see continued interest rates increasing in Canada well into 2018. If The Bank of Canada increases interest rates, mortgage interest rates will continue to go up. That’s not an immediate problem if your mortgage is locked in for the next five years, but if you have a variable rate mortgage or your mortgage is due for renewal in the near future, rising interest rates could have a significant impact on your monthly cash flow.

We tend to think that a 1% increase in your mortgage interest rate is no big deal. But if you have a mortgage at 3% interest, a 1% interest rate increase actually means that your interest rate is now one third higher, that’s one over three higher, and that’s 33%, which is huge. Here’s another way to look at it, if you have a $500,000 mortgage at a 3.25% interest rate, amortized over 25 years, you’re paying $2,430.83 a month, an increase to 4.25%, which is only a 1% increase or 100 basis points as the economists would say. That puts your monthly payment up to $2,698.30.

Now again, that might not seem like much but that’s an extra $267.47 a month, do you have an extra $267.40 per month in your cash flow? And just so you know an extra $267 a month over a 25 year mortgage is more than $80,000 in extra payments over the life of the mortgage. That’s huge and that’s why mortgage interest rate increases are such a big deal.

So, you want to keep your interest rate as low as possible but if your mortgage is coming up for renewal, how do you know if you’re getting the best deal? What if your bank just renews you at the rate they think they can get away with charging you? That could cost you a bunch of money in the future.

Today on Debt Free in 30 my guest has a new tech start-up that helps homeowners explore their mortgage options. He also has some thoughts on fixed versus variable rates and how new financial technology is impacting our financial decision making. So, with that background let’s get started. And meet my guest. Who are you and what do you do?

Brent Hughes: Hi, it’s Brent Hughes and our business is Monitor my Mortgage and we created a software platform app, software platform both desktop and mobile to manage a little bit different than where you were talking, manage in-term mortgages.

So, the industry chases the renewal or the net new mortgage, we assist consumers on a day to day basis for exactly what you were talking about as far as when rates change, how does that impact me today? I don’t want to wait five years. It hasn’t factored in what I may have as far as life changes, new baby, job change. So, we are very focused on the in-term mortgage part of the business.

Doug Hoyes: Interesting. Well, great thanks for being here Brent and I want to dive into that in a little bit more detail. But before I do I want to give my audience my standard disclaimer and that’s this, I don’t pay guests to appear on this show and guests don’t pay me to appear on this show. Debt Free in 30 is not an infomercial for my guests or for any products so I invite my guests onto the show because I think they have useful, practical information to share with my listeners. So, you’re not going to hear any affiliate links or anything like that mentioned in the show.

So, with that disclaimer tell us a bit more about this product. So, it’s called Monitor my Mortgage and you said it’s more targeted at not the renewal market but someone who has an existing mortgage, so explain what you mean by that. I mean if I’ve got an existing mortgage, why do I need any additional information?

Brent Hughes: Probably the simplest way to sort of explain why we created this software was I’ve done it as a consumer. So, one of the most frustrating things to me was to listen on the radio and hear Bank of Canada is changing its rate, which is great to hear but I don’t actually know how that impacted me over my different mortgages over the years. So, I quickly pick up the phone, call my broker, they would tell me to check on what my amortized value is and what my penalty was. And if at that point they had that information they would then be able to provide me a solution or a stay put type scenario.

So, that to me is frustrating because I’ve sort of abdicated responsibility for what generally is my largest liability in the hands of somebody else. I don’t think I’ve ever had a call from any of my lenders to tell me that I should be looking at my mortgage midterm. So, we designed the software to do the calculation of the penalties based on your current situation. So, you have the scenario you gave where potentially somebody could be up to another $265 a month and where is that money going to come from?

This way, based on your notification level, so you decide what’s the minimum savings that interest you to at least open the door to start to discuss changing your mortgage in-term or over the life of the term, what’s the savings target you’re looking for, not on a monthly basis but over the remaining term? Because there are times where the software may say we can save you a thousand dollars net after your penalty but you’re about to get on a plane and head off with the family for a vacation, probably not the greatest time for you to make that decision. Now when you return from that vacation it may be an interesting thousand dollars to save. But it provides you the savings and the notifications based on your specific circumstance and your specific mortgage.

So, it takes two to three minutes to put your current mortgage in, then the system runs, you can run it on demand by simply pushing a button or it runs automatically for you nightly and provides you notifications. And so this is a consumer driven piece of software.

If I can add one more item, that question I met with a professional mortgage, a long-term mortgage professional, and the drew me a very simple drawing and it was a horizontal line with a vertical line at each end and he said that’s the life of a mortgage. He said, and he did a circle at the beginning, and he said this is when consumers make decisions on mortgages and this is when they make decisions at the end.

And his business was related to renewal and net new mortgages. And I said to him put an X where your competitors are and he put an X across the beginning circle and put an X at the end. And I said to him our software manages in between that. So every day you’re ignoring your customers, we’re helping them. We’re providing them information on where their mortgage is every day. So I said and when it comes time for them to either make an early renewal there’s a purchase, you know, they’ve sold their house, they’ve got a net new purchase, they’ll have the up to date information of where their position is.

Because most people don’t even know what their penalty is or how to figure it out, a variable penalty is very easy to understand about three months interest. But if you’re trying to figure out the interest rate differential, then find the information on your lender’s website and then do the calculation, most people won’t do that. They won’t find that out until they’re sitting with their lawyer on the payout statement. So, this provides them the day-to-day piece of mind really of where they stand.

Doug Hoyes: So the way it works I go into the program, this app on my phone and I punch in some basic information, you know, how much is owing on my mortgage, what the interest is when it comes up for renewal. And then –

Brent Hughes: Who’s your lender?

Doug Hoyes: Who my lender is. And what else do I have to put into it?

Brent Hughes: That – so, those are your – obviously when it started, you know, what’s the term, what’s your frequency of payment. Lender is critical because as much as everybody thinks the lenders are fairly similar on their penalties, they’re actually not, there are some extra charges here and there. So once you have that information there’s defaults on your notifications so minimum savings per month, minimum savings over the term to be notified, early renewal, when you want to be notified on your renewal dates, rate changes. So, when The Bank of Canada makes a rate change you want to know and be notified. All of those are defaults but you can adjust them based on your circumstance. After that if it takes you three minutes, that would be the most. And then the system runs.

Doug Hoyes: Got you. So, I set up my alerts and it says oh, guess what? Because I can’t remember when it was in the summer whenever The Bank of Canada raised rates and then they did it again in September I’d get some kind of alert that says ding, ding, ding rates have gone up so here is some potential advice for you. So, the app might suggest that I’m with Bank ABC now and I’ve got three years left to go on my mortgage but if I switch to a different lender I could save money, is that the kind of practical thing it’s going to tell me?

Brent Hughes: In the end we’re not a mortgage broker so we wouldn’t make a lender-specific recommendation. What the system will do, the system recognizes the different available rates on the market across – I wish I knew, I probably should have the number but 70 plus different combination of different lenders and different rates. If it identifies an opportunity for you it allows you to connect to one of our vetted brokers across Canada who we have a relationship with.

Once you connect to that broker, the broker’s going to connect to you by email or phone. The broker now knows your current state mortgage so it knows here’s everything that you have in place. Here’s the information that created an opportunity for you so you’re on a current five year, you have two years left, the rate difference is going to be about two basis point at 20 basis points and your penalty’s been calculated, here’s the information. So, you don’t have to spend the first 10 or 15 minutes updating the broker on your current state or the opportunity you’re interested in.

Then the broker, the mortgage professionals, will do their job. Because they’re going to look and say lender A may have a better rate but you’ve just told me you’re changing jobs in the next year or you’re adding to the family and there’s just certain – you still have life circumstances that have to be factored in. You may have a windfall coming, whether it’s an inheritance or something. You don’t want to – if you have the ability to pay down a mortgage a little bit earlier, you want to make sure you’re working with a lender that gives you the ability at the lowest possible cost. The broker is the one that makes the recommendations.

Doug Hoyes: Got you. And so as a consumer, I’m not paying anything for this app, is that correct?

Brent Hughes: Correct, the app, the software is free.

Doug Hoyes: So how do you make money then?

Brent Hughes: We have a relationship with the brokers we have in place. Lenders pay brokers a finder’s fee for lack of a better term. So, the lender will pay the broker and we share in that split with the broker. So, there is a – you know, one of the challenges I have is when people have vested interest in trying to sell me something. In this case you can use the software from, you know, day one and never connect to one of our brokers, take that information back to your lender and say that I know my penalty is roughly X, I think I should be doing something and away you go. You can take it to your current broker and take the same information.

The question I would say is, you know, and I think I’ve written some blogs on it, when was the last time your broker or lender called you in term on your mortgage? And the answer is they don’t, they have a vested interest to keep you in the position you’re in. So, what our software does is say here’s a vetted broker, if you’d like to have a conversation there is no commitment, no cost, no hooks, at least have the conversation and understand your options. And if you use one of our brokers then the lender fee will be split between us and the broker.

Doug Hoyes: Got you. And obviously I’m the one making that decision if the broker can’t get me a better deal than what I can get somewhere else then I’m not going to do it. So, I’m completely in control I guess is what you’re saying. Okay, so that kind of makes sense and I get the business model. Your goal is that lots of people will be using it, lots of people will see that there’s potential savings, they’ll reach out to one of the people in your network to do it. But if they don’t, fine they can use it completely for free and do what they want with the information.

So, okay so let’s talk about well, I want to get into interest rates but before we do that, what you’re describing, this app that you’ve got I guess the current buzz word is “fin tech”, this is a fin tech application, a financial technology thing that – that’s the buzz word. If you want to start a company and raise a few million dollars in an IPO just call it fin tech. And just like the internet in the year 2000, right, everyone will jump on it.

Brent Hughes: If it were only that easy.

Doug Hoyes: There you go eh, I live in a simplified world obviously where I think everything is really easy. So, how do you see applications like yours or fin tech in general, impacting the way we make financial decisions? Because you described how it used to be. Once every five years I would walk into the bank and they would tell me what my new mortgage interest rate was going to be and I’d sign the piece of paper. That’s no longer the way it has to be. So, what do you see as the future for applications, not just in the mortgage area but, you know, fin tech applications in general and how we’re going to make financial decisions in the future and what that’s going to do to the financial industry in general?

Brent Hughes: Yeah I think it doesn’t just start with the financial industry for me. I mean if I’m looking to hire a taxi or a car to go to from A to B, we used to stand on the corner, wave our arms and hopefully somebody would stop. You know, obviously the largest of the players right now put in software into people’s hands that provide them visibility, access to information and a level of governance. So, I won’t state their name but they changed the way that people hire a car.

I think that’s ultimately what our goal was, if you can put information into people’s hands to make it easier for them to make an educated decision, it’s just a natural way to look. It may not always be about saving money. I mean I think that’s a little bit of a misnomer with some of the fin tech businesses that are out there it’s all about saving money. Sometimes – your description at the beginning talked about in five years, you know, changing rates today may not impact you but in five years they are. And where are you going to find that?

I always did a simple calculation when I close my eyes at night. And I say what are my total assets worth, what are my total liabilities worth? Close your eyes, as long as my assets are greater than my liabilities I should be able to get a good night’s sleep. Just by getting the information in people’s hands faster, I think they’re going to make better educated decisions. I know I have retirement goals coming up, the lenders, many of the banks are creating and the wealth advisors are creating tools that give me better visibility but in the end the decision’s still mine.

And that’s, I hope what the goal of these fin tech companies are. I think there’s always suspicion that there’s a vested interest but I think in the end, as long as the consumer recognizes it, it’s still their decision. So, give you good information, give you accurate information, give it to you quickly when you want it. I’ll take that any day of the week and then I can make a good decision. So, I think that should be the goal of most of those businesses and our business.

Doug Hoyes: Yeah and that’s an interesting way you describe it. So, I mean I understand what you’re saying with respect to in effect getting a taxi, I may not pay less for the new service then the old service or I may. But I’m able to see what kind of car is coming, I can say I want a big car or a small car, I know exactly when it’s going to arrive. So, it’s not just about the money, it’s putting a lot more information into my hands.

Okay, so let’s take the case then of somebody who has a variable interest rate mortgage. So, you already mentioned the case of somebody who has a fixed-rate mortgage, there’s still three more years to run on it but with your app it might tell me interest rates have gone down and it’s still better for me to get a different mortgage, pay the penalties, the interest rates will be lower, it’ll help me, does that thought process change at all when I have a variable interest rate mortgage? Or is it pretty simple, interest rates have gone down, you switch. How does it work with a variable rate?

Brent Hughes: So, it’s interesting because when we – the software was built over, over, you know, just over a year’s period and everybody said to us oh, if this software were only built a couple of years ago you would have had a lot more clients right off the start. And I said why’s that? And they said well when rates go down, that’s when savings are created. And I said it actually was created for the opposite, it was created when rates start to go up.

As we know debt levels, consumer debt levels, are high, bankruptcy risks are high so you – I want more information. A rising tide will float all boats is probably the nicest way to put it but everybody’s going to have a win/win when rates are going down. It’s when rates are going up that I want the most information in my hands with the recent Bank of Canada announcements, a couple of changes over, you know, the interesting one the first Bank of Canada announcement being in July, everybody was on vacation.

So, although you had an impact and our consumers were all notified, these rates changed, the activity by consumers was quite low. They – the system told them the rate went up, they had a variable rate, it immediately impacted them. So, anybody on a variable, immediately knows that the variable rates are changing, that the prime has changed. So, they have the information but there wasn’t a lot of activity because there was – it was in the middle of summer, we didn’t go through the greatest summer of the year so there was a lot of other things going on. The September announcement will be different and was different because all of a sudden that’s the second rate increase in over a period. So, now people are going to start taking note saying okay, what’s the next announcement going to look like?

So, the software will tell you right away there’s been a change, here’s how it impacts you specifically. The decision now comes down to the consumer to pick up the phone and call, you know, their lender, their broker, our broker and say here’s my circumstances, here’s my financial position, here’s my family position, here’s my goals, all those other things have to factor in so it’s just not an automatic where I think the great discussion after a rate announcement is “should I be on fixed or variable?”

And the answer is it’s different for everybody. So, are you down to the last few years of paying off your mortgage or are you just getting into the market. So, I think you – the software will tell you that it’s changed, it will give you the information specific to you, now you need to factor in the other variables to make a decision, do you go fixed, do you go variable? I don’t think either of us could tell the other person which is best.

Doug Hoyes: Yeah and I think that’s the key point is you got to think. And so, anybody who says oh well you should definitely go variable or you should definitely go fixed doesn’t really understand that it’s a multifaceted decision. And yeah I mean I guess for the last 10 years if you go back to, I don’t know, 2008 or whatever, that time period, yeah variable rates ended up being the correct decision for most people because interest rates kept going down and down and down.

But going into a variable rate in June of 2017, well, you know, with a couple of Bank of Canada rate increases and perhaps more to come, that has not been as good a solution. However as you correctly pointed out if I’ve only got six months left to go on my mortgage or a year or two even, then the variable rate is probably less than the fixed rate. That may or may not be true but that’s why it’s not as simple as yeah you pick one or the other.

How much longer you have to go on your mortgage certainly has an impact. Is there anything else that would impact the decision? I guess the credit worthiness of the borrower perhaps has an impact as well or is there anything else?

Brent Hughes: Absolutely, the credit worthiness is obviously going to be important, we’ve had a number of opportunities where our clients come through where you look at the rate that they were paying and at first you look and go how did they end up with such a high rate? You know, when you see the system, you see the opportunity that we pass onto the broker, it doesn’t make any sense. And it was the position they were in. It could have been a recent divorce, it could have been, you know, other financial challenges they were having. So, the opportunities now to get a better rate definitely exist for some of those people.

The big thing for me and people often, either they haven’t experienced it but I did experience it, is change a job when you’re within a year before your mortgage is down, the lenders they look at you very differently. And you can be with that same lender for years and all of a sudden you’ve changed jobs because it’s a new opportunity, it’s a better role, it’s a great opportunity and you’re six months into your new job and you go back to your bank and say okay it’s time to renew your mortgage and they say well, you’ve only been at your job for six months.

And you’re going wait a second, I’ve been with you for two mortgage renewals, I’ve been at my same old job for 10 years and now all of a sudden you look at me with a little bit of a concern, it just doesn’t make sense. So, I always, anybody that ever asks me I always say, make sure you’re looking at your renewal time frame before you change that job. I think that’s an interesting factor that gets overlooked.

Doug Hoyes: Yeah and we see that with credit reports even where you live. Now of course if you have a mortgage you’re probably living in the house you live in and so you’re not moving around frequently. But yeah you’ve lived at the same house for 10 years and then you move, that can have a negative impact on your credit score. Now if everything else is positive it’s not going to make a whole lot of difference. But you’re right if you’ve switched jobs and as a result, you know, moved to a different town and therefore you’re living in a different place, those are a couple of changes that may not be perceived favourably by the automated credit scoring machine that governs all of our lives. So, it’s certainly something you’ve got to be aware of.

So, okay so final point then and I think we’ve hit on some important things here, what final practical advice then do you have for people who are, you know, navigating what is becoming a much more volatile housing market and mortgage market and how we should go about weighing our options and making informed choices. Is it really as simple as you’ve got to think and look at all the alternatives?

Brent Hughes: Yeah, I think it really is probably the simple. And, you know, obviously our software provides you with a certain level of information. There’s other software, there’s other contact points, whether it’s just really staying informed is really all I can say is that if we’ve abdicated – well, one of the things that used to make me crazy is people would go crazy when their cell phone, their mobile went up by, you know, $10, $15, $25 a month. And they were quickly jumping on the so called loyalty line to have a discussion with their carrier and would be very frustrated.

And yet our largest, generally our largest liability and one of our largest payments every month, is going towards our mortgage. So, if there’s tools or information out there to keep you informed I would say don’t assume that others are watching out for your best interest. Become informed and at that point at least you have the tools to do something about it and then you need to decide, you know, which path you would go from there. But there are some great tools out there and I think the ostrich approach that we’ve all taken, now I can raise my hand around our mortgage of burying it in the bottom drawer of a file cabinet doesn’t need to be that way.

Let’s make sure we understand especially in changing rate environment whether we’re in the best situation we should be in for the coming years.

Doug Hoyes: Yeah and I think that’s a great way to end it. I totally agree you’ve got to look out for yourself. You are the most motivated person to look out for yourself. And you’re right your house is probably the biggest expenditure that you’ll ever make in your entire life and therefore your mortgage payments over the life of that are the most money you will ever spend. In fact you spend more on the mortgage than you spend on the house because you’ve got interest tacked onto it. So, keeping track of where that all pans out is critically important. So, that’s fantastic, so, Brent how can people find the app that we’ve been talking about today?

Brent Hughes: So, we’re available on both Google Play as well as and the app store. You can also – there’s a desktop version at our website. I’m not sure whether I can share that.

Doug Hoyes: Yes, go ahead, tell us what the website is.

Brent Hughes: It’s monitormymorgage.com, so, all one word monitormymortgage.com., but it’s available in all of the mobile stores and it’s free so we hope that it can help you. And if there’s anything that anybody sees that they would like to see enhanced, we’re always open to add and adjust the software based on recommendations.

Doug Hoyes: Excellent, well thank you very much, thanks for being here Brent.

Brent Hughes: I appreciate the time.

Doug Hoyes: Excellent, well once again Brent’s app Monitor my Mortgage can be found at monitormymortgage.com so that’s all one word and then of course if you search for that in the various different app stores you can find it as well.

I think the next year’s going to be much more volatile for mortgage interest rates than what we’ve seen for the last few years. So, whether or not you’re using Brent’s app I think being aware of your options is obviously very important.

So, that’s our show for today. Full show notes including a transcript and links to everything we discussed today including Brent’s app can be found at hoyes.com that’s h-o-y-e-s-dot-com. Thanks for listening. Until next week, I’m Doug Hoyes. That was Debt Free in 30.

Unlike RRSPs, there is no provision in the Canadian Bankruptcy and Insolvency Act to specifically deal with funds in a Registered Disability Savings Plan (RDSP) in the event the beneficiary files for bankruptcy. We discuss a recent case of an individual who went bankrupt and, after a court ruling, was able to keep their RDSP.

In addition to talking about whether you lose your RDSP in a bankruptcy, we talk with Alan Whitton about the ins and outs of RDSPs. This is a subject close to Alan as he and his wife found themselves having to set up an RDSP for their son.

RDSPs Exempt From Seizure in Bankruptcy in Canada

This matter was dealt with in a recent BC Supreme Court ruling that held funds in a RDSP can not be seized by a Licensed Insolvency Trustee (Trustee in Bankruptcy) for the benefit of creditors in the event the beneficiary of the RDSP declares bankruptcy.

What are RDSPs?

An RDSP is a registered savings plan designed to help Canadians with disabilities save for the long-term financial needs of a disabled person, including medical, care and living costs. RDSPs can only be setup for someone who is eligible to receive the Disability Tax Credit.

If this is for your child, you can only begin making contributions after your child is diagnosed with an eligible disability. You can also apply for an RDSP on your own behalf as an adult.

Like an RESP, an RDSP allows a disabled person, and their family members, to set aside funds in a separate trust account for a designated beneficiary – in this case the disabled individual. Contributions are not tax deductible but income earned on the funds are tax-deferred until they are withdrawn. The government provides additional support through matching grants and bonds.

RDSPs were introduced in 2008 as part of the Canada Disability Savings Act. Interestingly, in the same year the federal government made changes to the Bankruptcy and Insolvency Act to protect RRSP and RRIF contributions, but did not include RDSPs.

Facts in recent RDSP and bankruptcy court case

Ms. Alary was disabled and entitled to the disability tax credit under section 118.3 of the Canadian Income Tax Act. Mrs. Alary had an eligible RDSP with the Royal Bank of Canada, taken out in 2010. She was was the sole beneficiary and holder of her RDSP. The fund consisted of $6,800 in private funds provided by her parents in 2012. Once income growth and grants were calculated in, her funds held a total of $32,250 in trust.

In 2015, Ms. Alary filed an assignment in bankruptcy under the Bankruptcy and Insolvency Act. Her trustee notified the Royal Bank of her filing and requested Royal Bank to forward the private funds originally contributed to the plan to the trustee for the benefit of Mr. Alary’s creditors. The trustee made this claim because there was no specific provision in the Bankruptcy and Insolvency Act or the Income Tax Act governing how RDSPs should be treated during insolvency.

The Royal Bank refused to release the funds claiming that the money held in the plan was exempt from seizure. As such, they could not release the funds to the trustee.

Under the terms of section 146.4 of the Income Tax Act, funds held in an RDSP are held in trust “exclusively for the benefit of the beneficiary under the plan”. However the terms of the trust permitted the court the ‘discretion’ to direct that the funds be released for the benefit of creditors of the bankrupt.

Madam Justice Bruce found that there must be a balancing between the fact that the funds are held in trust for the benefit of the beneficiary and the rights of the creditors under the Bankruptcy & Insolvency Act. In this case, requesting the release of a portion of the funds permitted under the terms of the trust would trigger a requirement for Ms. Alary to repay a significant amount in the government-assisted portion of the fund. Madam Bruce found that the court should be guided by what was “just and equitable” and as such refused to order the release of any funds.

What this means for your RDSP

The court did not rule that all RDSPs are exempt from seizure. The court made its decision not to release the funds to the trustee based on the facts of this case. It is apparent that this means future cases will be dependent on the Court’s ability to exercise its discretion. In the absence of clearer legislative exemptions in the Bankruptcy & Insolvency Act, Licensed Insolvency Trustees will also likely exercise discretion in whether to seek court direction about the release on any RDSP funds to the estate.

Doug Hoyes: We’ve talked many times here on Debt Free in 30 about RSPs and RESPs but we have never before addressed another savings vehicle that is also known by a four letter acronym, RDSP. What is an RDSP? What happens to an RDSP if you go bankrupt? That’s today’s topic here on Debt Free in 30.

So, to get today’s show started let’s welcome back to the show a man who I consider to be an expert on this topic, the Big Cajun Man also known as Alan Whitten, Alan welcome back. So, let’s start with the basic question, what does RDSP stand for?

Alan Whitton: Registered Disability Savings Plan.

Doug Hoyes: Oh there you go.

Alan Whitton: The literal answer is always the easy one.

Doug Hoyes: It’s always the easy one. So, okay so Registered Disability Savings Plan, okay what is it, how does it work, who’s eligible for it? Just dump me what’s in your brain on this topic.

Alan Whitton: So, I’ll precurse this with what I told you before, which is the real expert on RDSPs is my wife who has done a lot of work on the Disability Tax Credit side of things and made sure that this is all well understood by me as well because I have a son that’s on the autism spectrum. So, this is the reason I have any expertise in this area.

What’s it for? It’s for either family or parents to put money away for a disabled family member or someone who is disabled to put money away themselves. I found that one out from a reader who sent me a really good email explaining a whole bunch of stuff that he had done.

Doug Hoyes: Now so I’ll just fire some questions and you can answer yes or no if you know the answer, if you don’t then we can skip over it.

Alan Whitton: Oh there won’t be any no’s, I’m an expert.

Doug Hoyes: There you go, that’s right, whether I know the answer or not I’m going to give you the answer.

Alan Whitton: I’ll make it up.

Doug Hoyes: So my understanding is you can contribute up to the age of 49, is that correct?

Alan Whitton: Yeah, it becomes an issue with when the money gets withdrawn for the person involved and after 55 or something like that because they’re close enough to collecting CPP there’s a whole bunch of interesting stuff so 49 seems to be the stop point.

Doug Hoyes: So there are complicated rules that –

Alan Whitton: It is possibly the most interestingly complicated savings plan I’ve ever seen in my life.