Does Debt Consolidation Hurt Your Credit?

Discover how debt consolidation affects your credit score in Canada. Learn about consolidation methods, their pros and cons, and alternative debt relief options from a Licensed Insolvency Trustee.

Gain valuable insights into responsible borrowing practices and loan management in Canada. Learn about different types of loans, including personal loans, lines of credit, and secured vs. unsecured loans. Understand key factors that affect loan approval and interest rates, such as credit scores and debt-to-income ratios. Discover strategies for comparing loan offers and identifying predatory lending practices. Get information on how to read and understand loan agreements, including terms and conditions. Learn about the impact of borrowing on your overall financial health and credit score. This section provides essential knowledge to help you make informed decisions about loans and borrowing to avoid future debt problems.

Too much debt already? Schedule a free consultation with Hoyes Michalos. Our Licensed Insolvency Trustees will conduct a free debt assessment and help you find debt relief.

Discover how debt consolidation affects your credit score in Canada. Learn about consolidation methods, their pros and cons, and alternative debt relief options from a Licensed Insolvency Trustee.

The credit impact of a bankruptcy or consumer proposal does not have to prevent you from getting a mortgage. Discover steps that can help you get a mortgage even if you have bad credit.

A payday loan may be tempting, especially when you are in need of an emergency expense but beware! They do more harm then good and can put you into serious debt. Doug Hoyes explains the pros and cons of using payday loans for emergencies.

Revolving credit means credit cards and lines of credit. You probably use it everyday but it's important to understand all of its benefits and risks so you avoid financial trouble. Doug Hoyes explains in this post.

Do you know what a rise in interest rates could mean for you? Learn about the interest rate patterns in Canada, how a rise affects your finances, and what you can do to move forward confidently.

What is the point of making extra loan payments? Here we explain how making more payments can save your money and help you pay off your debts much earlier.

Do you ever wonder if the debt you have accrued is more than you can handle? Or what is considered a ‘normal' debt-to-income ratio of someone in your financial situation? Find out more in this post.

Does my credit profile expose me to risks when applying for loans? Use this guide to help you understand what your borrower risk profile is, and how to navigate your lending options.

Predatory loans are the causative agent of 40% of filings for bankruptcy or consumer proposals in Canada. Read along for Doug Hoyes’ tips on how to spot this form of lending and how to protect yourself.

Trying to figure out if a joint loan is your best option? Learn here, about the pros and cons of having a joint consolidation loan with your partner and debts that may be a bad idea to consolidate.

If you are unable to meet your tax payments, you may be considering borrowing to reduce long term interest and penalties. Learn if taking out a loan to pay taxes is a good choice for you.

Considering borrowing against your vehicle to help deal with some debts? Find out how car title loans work, the advantages and disadvantages, and other options you have to pay off debts.

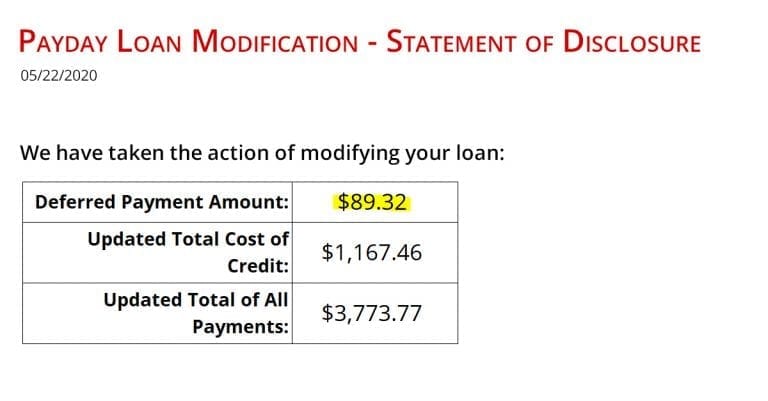

Payday lenders will try anything to collect. Loan modification agreements do not alter the ability of your bankruptcy or proposal to wipe out these debts. Learn about these traps from Ted Michalos.

Thinking about applying for a debt consolidation loan, but don’t have good credit? A cosigner can help you get approved but there are risks. Learn the pros and cons, and alternatives if you are not successful.

Debt consolidation loans are one of the several debt relief options consumers can use to help them deal with debt. Explore how these loans work, pros and cons, and if consolidation makes sense for you.

Are you trying to quickly pay off some credit card debts or old bills with a cash loan? Here is our expert opinion on why these credit instalment loans might not be such a good idea.

Debt consolidation loans can help you consolidate debt but before you approach a lender review the possible costs and risks of using this option for debt relief.

Getting a debt consolidation loan to pay off debt seems like a simple solution, but it may not be. In this detailed guide, we explain everything you need to know before applying for a consolidation loan.

Companies can be very creative with scamming individuals looking for loan, especially those with poor credit. Learn about advance fee loans and how to identify, avoid, and report loan scams.

Has your bank sent you a pre-approved credit limit increase and you’re not sure if you should accept it? Find out what the pros and cons of an increase are, and what decision is right for you.

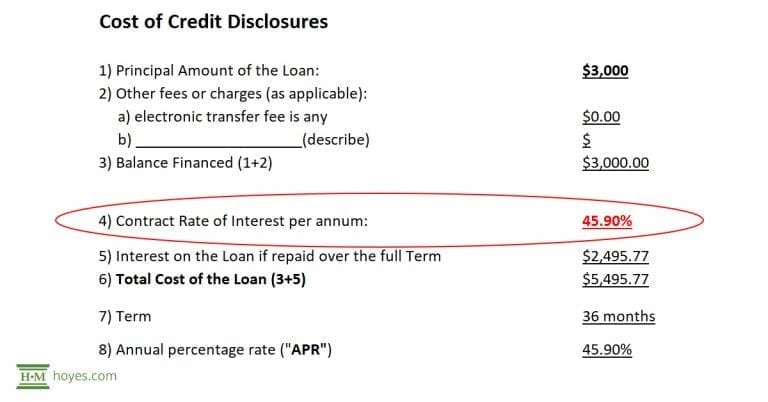

Interest depends on the types of loans you borrow. Ted Michalos explains what the criminal interest rate is in Canada, how payday loans are a trap and what to do if you have overwhelming monthly interest.