Interest rates are the price lenders charge to use money we borrow. The riskier the loan, the higher the interest rate. That’s why different types of loans have very different rates.

- The Bank of Canada overnight rate (the rate banks are charged to borrow) is typically the lowest rate.

- Because mortgages are secured by your home, they are relatively low risk with rates currently around 3-5% for the “best” qualified customers, depending on the term.

- Secured personal loans and lines of credit will typically cost about 6% to 10%.

- Unsecured loans and personal lines of credit will cost from 7% to 12% at a bank.

- Credit cards charge interest in a range of 10% to 29.99%

- Overdraft charges at most major banks run 21%.

- Finance company loans range from 21.99% to 31.99% plus admin fees and charges.

- Quick cash installment loans advertise 6% to 59.99%

- As of January 2018 payday loan companies in Ontario are restricted to $15 for every $100 over a two week period. If you are curious, that works out to 390% annually.

Table of Contents

What is the Criminal Interest Rate in Canada?

Section 347 of the Criminal Code of Canada sets the maximum allowable annualized interest that may be charged at 60% – interest charged above that level is considered usury and is a criminal offence.

However payday loans are exempt from Canada’s usury laws. In 2007, Section 347.1 was added to the Criminal Code that exempted payday loans from Section 347. Instead authority to regulate payday loans was assigned to the provinces.

Ontario Maximum Payday Loan Costs

In Ontario the Payday Loan Act was passed in 2008 and brought into force on December 15, 2009. As of 2018, the Act limits the amount an individual may be charged to $15 per $100 borrowed for a two week period. That makes the simple annual interest rate equal to 390%.

Here’s how payday loan interest works:

You borrow $100 for a period of 2 weeks and pay $15 in fees (under Ontario law).

Assuming you renew that loan each week – you can’t by law but we will so we can calculate the real interest rate – you only borrow $100 for the entire year because you repay the old loan with the new loan. So to borrow $100 for 26 periods through a payday loan you pay a total of $390 in fees.

$15 per period times 26 weeks = $390 in fees or roughly 390% per year on the $100 you borrowed.

However, payday loan costs don’t necessarily max out there. The law says that the $15 is inclusive of admin fees, but excluding default charges.

If you default on a payday loan they may charge you additional fees that push the annualized interest rate even higher!

Payday Loans Not A Small Loan Anymore

A payday loan is defined as a short term loan for a small sum of money in exchange for a post-dated cheque, pre-authorized debit or future payment of a similar nature. At the time the changes were implemented in 2009, the government thought the average loan was for about $300 and repaid in two weeks or less.

The problem is, someone experiencing financial problems will often take out much larger loans. Based on a study of our insolvency clients and their use of payday loans, the average loan size was $1,311 in 2018.

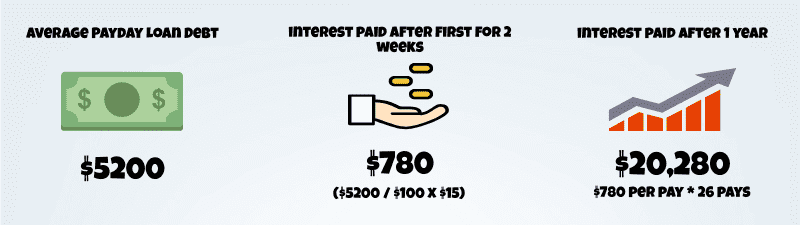

The average person using payday loans to keep afloat also tend to visit more than one payday lender. The result being that our average client owes almost $5,200 on 3.9 outstanding payday loans.

Using the maximum allowable charges (assuming no defaults) the interest charges for two weeks would run $780. That’s before any repayment of the actual loans. If the loans were to remain outstanding a full year the interest charges would total $20,280! Oh, and they’d still owe the $5,200 they borrowed.

What To Do When Interest Consumes Your Paycheque

If you find yourself in this situation you need a way off the payday loan debt treadmill.

If you do find yourself in need of temporary short-term borrowing, consider these 8 alternatives to payday loans.

But…

If you are like most of the people we see, payday loans are the final straw that breaks your back – by the time you turn to payday loans no other lender will help you. In that case it’s time to talk to someone about how to eliminate payday loan debt – your debts won’t go away by themselves and you can’t afford to keep paying all of this interest.

Find out what your debt relief options are. Contact us for a free consultation with a local debt expert. You don’t have to decide what to do right away, but knowing your options if the first step to getting out of debt.