Our knowledgeable team of Licensed Insolvency Trustees provide information and expert advice to help you on your way to becoming debt free. Our extensive debt help resource centre includes articles, videos, and podcasts on how to get out of debt including commonly asked questions about consumer proposals, bankruptcy, and debt consolidation options. Become informed about credit rebuilding and other money management tips as you search for a solution to your debt problems.

One option for dealing with your debt is to talk to your bank first. In this post, we outline the ways in which your bank may help you get out of debt, tips for how to approach them when asking for help, and what you can do if your bank refuses to provide debt relief.

If you face an income loss, fall behind on proposal payments and the proposal becomes annulled, what are your options? We explain what a proposal annulment means for your debts, how to revive your proposal, and how to prevent a proposal annulment in the first place.

You may be overwhelmed by debt and considering a debt settlement. In this post, we walk you through how to determine an affordable offer, the dos and don'ts of settling with your creditors, how to reduce debt by up to 80% and when working with an LIT is the right option.

In this comprehensive post, learn how your credit score is impacted, what brings a credit score up and down, and get the facts on common credit score myths. We also outline what lenders consider when approving new credit applications.

You may be considering a consumer proposal and wondering if it will impact your spouse. To help you get a better understanding, we explain how joint debts work, how your marital assets may be affected and how your spouse may be involved in the process. Learn more.

What are your options if CRA says you were ineligible and must repay CERB, CRB or other pandemic related benefits? Can you file a bankruptcy or proposal if you can't afford to pay back CERB? Doug Hoyes explains.

Your bank may be your biggest creditor in a consumer proposal. In this post, Doug Hoyes discusses what banks look for when reviewing proposals and Hoyes Michalos' process for ensuring consumer proposals are accepted by creditors.

We know it can be hard to go without a credit card when you file a bankruptcy or consumer proposal. We explain whether it's a good idea to get a credit card during your filing or immediately after and if you do get a card, which credit card issuers are best to start with.

If you've recently completed your consumer proposal - congratulations. Now it's time to plan for life post-proposal. We explain what you can expect, the steps you should take after completing your consumer proposal, and best practices for rebuilding your credit.

There are a lot of misconceptions surrounding why someone is driven to file for bankruptcy. In this post, we share a realistic sequence of events that leads someone down a path of financial instability and into our office for debt relief. We also explain what you can expect when you declare bankruptcy.

Many people struggle to repay their student debt even years after graduating due to inconsistent income or lack of gainful employment. Falling behind on student loan payments is not uncommon but it should be dealt with, especially if your loans are now in collection. We explain what creditors can do and how to get relief.

If you're overwhelmed with debt, this post will help you decide whether you should file a bankruptcy or deal with your debts via a debt management plan by reviewing key questions, as you would in a real debt assessment with a Licensed Insolvency Trustee. Learn which debt relief option is right for you.

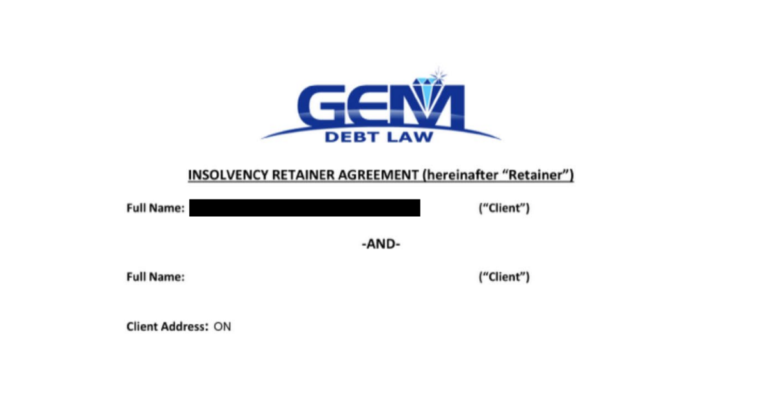

This is yet another case of an individual struggling with debt, told to pay exorbitant fees to a debt settlement firm to deal with their debts. This time, the company was GEM Debt Law. We review the terms of the contract and explain why these debt consultants should be avoided.

Ideally, in your 40s, you want to prepare for your transition into retirement. But being burdened with debt at this age can hold you back from building any meaningful wealth. Luckily, there are debt relief options available to help you take control of your future.

We know it can be stressful when you're unable to make your credit card payments. In this post, we help you understand the potential consequences if you fall behind on your credit card debt, as well as, options for eliminating debt.

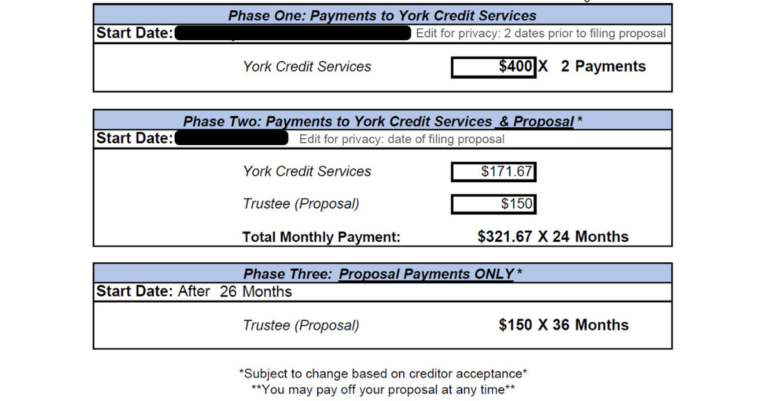

Struggling with debt? Go directly to a Licensed Insolvency Trustee. Unlicensed debt consultants like York Credit Services will charge you extra fees just for a referral to an LIT. Here's a real story of someone who was scammed into paying an extra $800 for nothing.

There is a common misconception that when you file for bankruptcy in Canada, you lose everything. But that's not true. In this post we outline exempt and non-exempt assets in a bankruptcy and how a consumer proposal actually allows you to keep everything.

Ever wanted a budgeting plan where you get to spend guilt-free? Look no further than zero-based budgeting, where every dollar is accounted for so you can rest knowing your money is well-managed.

Struggling to pay your mortgage or have you already fallen behind? Don't worry, you have options available, including refinancing problem debt, selling your home, or filing a consumer proposal to get rid of unsecured debt to allow for more comfortable payment of your mortgage.

If you decide you want to file for bankruptcy, that doesn't necessarily mean you can stop making debt payments. It'll depend on the debt and when you plan to file. Also, some debts can't be included in a bankruptcy. Learn which debts you can and can't stop paying before filing.