Table of Contents

Do I lose my RRSP or pension if I file bankruptcy in Canada?

Many people are worried that if they file personal bankruptcy they will lose their RRSP and other pension savings.

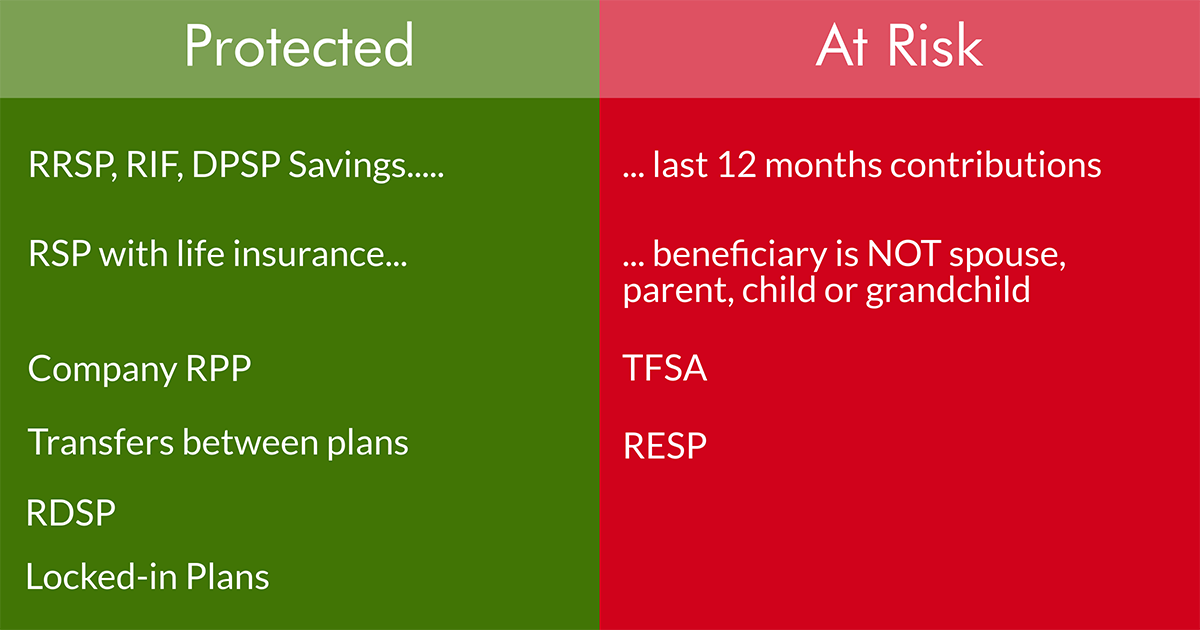

In Canada, most Registered Retirement Savings Plans (RRSPs) are protected in bankruptcy and so, in general, you can keep your RRSP savings after filing bankruptcy.

The Bankruptcy and Insolvency Act (BIA) under section 67 (1) (b.3) exempts RRSPs from seizure for your creditors except for any contributions made within the last 12 months.

The BIA also states that creditors are not entitled to any assets that are exempt from execution or seizure by provincial law. In Ontario:

- A Registered Pension Plan is governed by the Ontario Pension Benefits Act is exempt from seizure in a bankruptcy. Ontario protects company-sponsored or government-sponsored registered pension plans (RPPs). All pension assets under these plans are protected, regardless of when the contribution was made. Both employer and employee contributions are safe from seizure.

- The Insurance Act of Ontario protects RSPs that have a life insurance component if the beneficiary is a spouse, parent, child, or grandchild. In this case, all contributions are safe.

Let’s look at three common examples:

Example 1: Your employer takes 5% of your pay and puts it in a registered company pension. All contributions are yours to keep, even those made within the last year and those matched by your employer.

Example 2: You have a Registered Retirement Plan with an insurance component with a company such as Sun Life and your spouse is a beneficiary. These plans are yours to keep, including contributions made in the last year.

Example 3: You contribute 3% of your pay every payday to your own individual RRSP through an automatic savings program. Contributions made to your RRSP in the last 12 months before filing bankruptcy are at risk of seizure by the trustee.

Download our free PDF guide: How Does Bankruptcy Affect Registered Savings Accounts & RRSPs

Trustee has same rights as plan holder

The trustee cannot be granted any more rights to assets in the plan than the plan holder, including for recent payments. If the plan contains terms that prevent the plan holder from requesting payment until a specific event such as termination, death, or retirement, the trustee is not entitled to seize what the plan holder cannot withdraw.

What about transfers between RRSPs?

A transfer is not the same as a contribution. If you transfer funds from one RRSP to another company, then these are not new contributions in the last 12 months and as such cannot be seized by your trustee.

What about a spousal RRSP and bankruptcy?

The BIA applies to RRSPs you own and control. If you file bankruptcy, contributions you made to your spousal plan are not subject to seizure by the trustee. If your wife goes bankrupt, the maximum exposure for her spousal RRSP is the contributions you made in the last 12 months.

What about a RRIF and bankruptcy?

A Registered Retirement Income Fund (RRIF) is treated the same as an RRSP. Normally individuals withdrawing funds from a RIF are not making current contributions, however if they do, their maximum exposure is contributions made within the past 12 months.

Bankruptcy law in Canada protects RRSP savings. Only the last 12 months contributions are at risk. You can ‘buy back’ recent contributions from the trustee. In a consumer proposal you keep all assets, including recent contributions. Don’t drain RRSP savings to repay large debts. Talk with a Licensed Insolvency Trustee about your options.

What about an RDSP?

While there is no specific provision in the BIA to deal with a Registered Disability Savings Plan (RDSP), a recent British Columbia Supreme Court ruling held that funds in a RDSP cannot be seized by a Licensed Insolvency Trustee in a bankruptcy for the benefit of creditors.

What happens to a DPSP and bankruptcy?

A Deferred Profit Sharing Plan (DPSP) is treated the same as an RRSP in a bankruptcy. The maximum exposure is any contributions made in the last 12 months. Most DPSP plans have terms that the employee cannot withdraw these funds while still an employee for that company, therefore the full amount in the DPSP could be protected.

Locked-in pension plans

Pension plans that are designated as a Locked-In Registered Plan are exempt from bankruptcy or seizure. The trustee has no entitlement to money in this plan, including recent contributions.

What about TFSA and bankruptcy?

While a Tax-Free Savings Account (TFSA) is a registered savings vehicle, it is not a RRSP and as such is subject to seizure.

What happens to an RESP if I file bankruptcy?

Because the plan holder (usually the parent) can cash out a Registered Education Savings Plan (RESP) at any time, an RESP is considered to be an asset of the plan-holder. Therefore, if the plan-holder is bankrupt, an RESP is subject to seizure by the trustee.

Tips to protect at risk assets even if you go bankrupt

In truth, most people who are considering personal bankruptcy have ceased to make any contributions to their RRSP because they are using most of their income to make debt payments. However, if you do have exposure to recent contributions here is how we advise clients.

Our first step is to review your RRSP documents to determine how much you have contributed in the last 12 months. If you contribute through your paycheque at work we can generally get this information from your paystub. If you have an RRSP through a bank or investment advisor, they will provide a statement.

If you have made no contributions in the last 12 months, no further action is required; you can keep your RRSP.

If you have made contributions in the last 12 months or have other seizable assets like RESPs, you have three options:

- You may request that the trustee contact the bank or investment company and withdraw the contributions from the prior 12 months. It is the trustee’s responsibility to pay the tax owing on that withdrawal, so you have no further costs or obligations.

- You may decide to contribute an extra amount to your bankruptcy to “buy back” your RRSP contributions for the last 12 months. For example, if you have contributed $1,000 and you are in a 30% tax bracket, the trustee would recover a net amount of $700; so you could pay the trustee an extra $700 and keep the full amount of your RRSP. The same applies to any assets you have in an RESP or TFSA. A payment plan matching the term of the bankruptcy can be arranged.

- If you have significant seizable assets, you could decide to file a consumer proposal. In a consumer proposal you don’t lose your RRSP or any assets.

As a final planning point, if you are not worried about having your wages garnisheed, you could stop contributing to your RRSP now while you catch up on rent, utilities or other current bills, so that contributions in the last 12 months are reduced.

Protect your retirement from bankruptcy

One of the most common, and costly, financial mistakes we see is people who drain their RRSP savings to keep up with debt payments when they are in financial trouble.

If you have significant debts, draining your RRSP (a protected asset) to fund debt obligations only serves to delay the inevitable. You should not use your RRSP savings to pay down debt without first speaking with a Licensed Insolvency Trustee about your options. Since RRSPs are protected in a bankruptcy, it makes sense to preserve these funds for your retirement.