You’ve been planning your wedding down to the last small detail including the big question – how are we going to pay for this? Should you take out a wedding loan or use your credit card to cover some of the costs of your wedding or honeymoon?

Let’s consider the concept of good debt and bad debt. Money borrowed as an investment in your future is generally considered good debt. While clearly your wedding is the beginning of your future together, a wedding loan fails to meet one important criteria: this investment is not going to provide you with future monetary value. It’s important to think of your wedding as a consumable as once it’s over you will have great memories but no future financial benefit. Borrowing money to pay for a wedding is no different than paying for a vacation on credit. In other words, I’d say it’s bad debt.

Table of Contents

Wedding loan vs credit card debt?

But what about replacing money you might consider putting on your credit card with a lower cost personal loan or ‘wedding loan’? That’s a smart financial decision, right?

Again, I’d say no. Unless you have stellar credit, a bank or personal loan to cover your wedding costs is likely going to come with an interest rate of 12% to 14%. Yes, that’s better than the 20% or more charged on a credit card, but it’s still a hefty amount to pay and will only add to your total wedding costs.

A wedding loan will still come with a high interest rate

Let’s assume you decide to overspend on your wedding (in other words spend more money that you have) and you borrow $8,000 to cover the difference. You take out a 3 year term loan rather than carrying that much debt on your credit cards. You and your new spouse will now be making payments of $275 a month for the next three years to pay off that wedding loan adding a total of almost $1,850 in interest.

Piling wedding debt on top of pre-marital debts

4 in 10 marriages begin in debt

Here’s the other problem. If you are like most Canadian couples you probably already have debt. You or your new spouse, or both of you, may already be working to pay off student loans, a car loan or existing credit card debt. In fact, a study we conducted a couple of years ago revealed that four in 10 marriages begin in debt, and not just from their wedding. Do you really want to add to that burden? Are you willing to postpone your dream of buying a home and starting a family because you started out with so much debt to begin with?

1 in 5 bankruptcies are due to marital breakup

Starting a marriage with debt can jeopardize your future together. Almost one in five insolvencies in Canada list marital breakdown as the primary cause. For many, financial problems started long before the relationship troubles. It’s hard to say which caused the other.

Keep your wedding affordable

My best recommendation is to plan the wedding you can afford. Set a budget upfront and stick with it. Keep track of all your possible expenses as your planning your wedding, and look forward to a long and happy life together, free from unwanted debt.

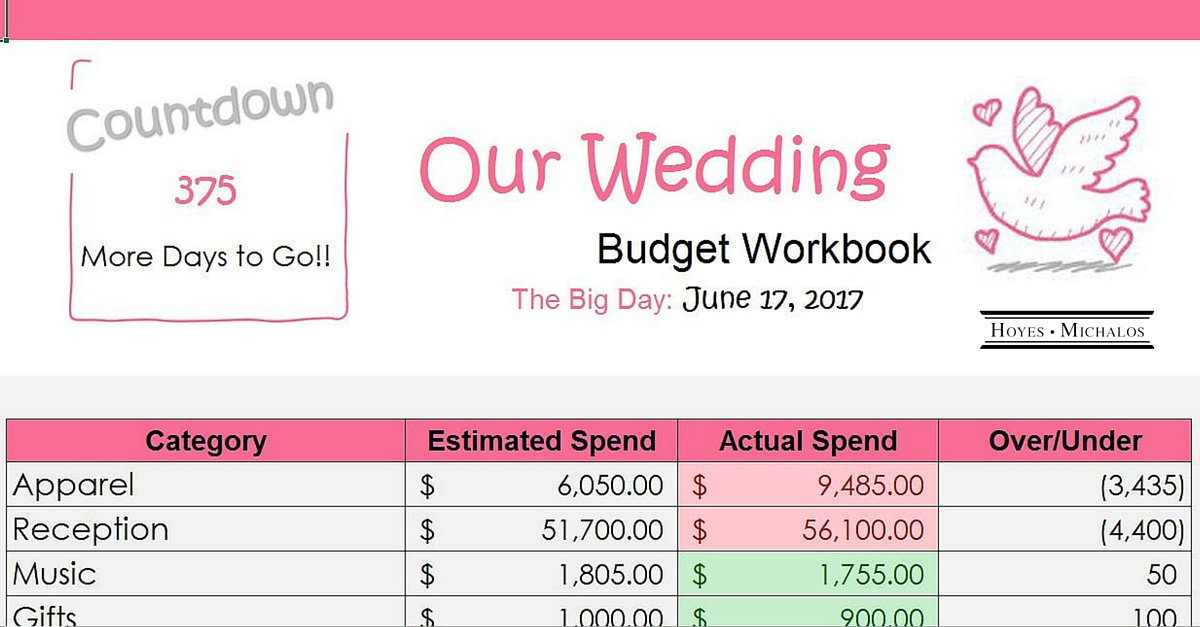

To help you keep track of your wedding costs, download our free wedding budget planner. It’s an excel spreadsheet complete with sections for all the possible expenses than might arise and room to add in anything special.