Reviewing your credit report at least once a year is part of a healthy financial routine. What you should be on the lookout for is errors or out-of-date information.

Table of Contents

Why You Should Check Your Credit Report Annually

This annual routine is important because you don’t want inaccurate information to hold you back from achieving your financial goals. Here are some big reasons to check your credit report:

- Before making a major purchase with financing, like a house or car, the prospective lender will want to review your credit file. Inaccurate information may mean that you are declined or offered a higher interest rate.

- Identity theft is becoming more prevalent. You may not realize that somebody has obtained a credit card in your name until seeing the details on a credit report.

- Many employers require a credit check as part of the hiring process.

- Creditors and collection agencies may update one credit report, but not all. It is important to verify that your credit report is correct within each credit bureau, because a lender, employer or potential landlord could check any one report (and odds are they may only check one), impacting whether you will be approved.

Below are links on where to get your free credit report and how you can apply to have errors corrected. We also explain what the typical credit report looks like.

How To Get Your Free Credit Report

We recommend getting a copy of your credit report directly from TransUnion or Equifax, Canada’s two major credit bureaus. As an alternative, you can get a copy through your bank if they offer you that service for free in their app or online banking platform.

Companies like Credit Karma or Borrowell also provide free reports, but our experience is that these reports do not always agree with what the credit bureaus have on file, and their information may be somewhat out of date. Potential lenders don’t see reports from these FinTech companies. Lenders will look at either TransUnion or Equifax, so you want to check that these sources are correct.

Both credit bureaus will want to verify that you are who you say you are. They will require you to send copies of 2 pieces of ID with your application. If you have recently moved, a copy of a phone bill or lease agreement will provide evidence of your correct address.

Here’s how to get your credit report for free:

Online

FREE online credit reports are normally only available from TransUnion. However, due to the coronavirus, Equifax is currently making credit reports available for free.

- Follow this link to the TransUnion website

- Follow this link to the Equifax website.

You just need to answer a few personal questions to confirm your identity as well as provide your address and social insurance number. One your identity is confirmed, you will be able to immediately print your credit report.

Please note the online system does not work perfectly. You may need to request a copy by phone or mail instead.

Telephone

Calling each credit bureau is one way to obtain your credit report free of charge.

- Equifax Toll Free 1-800-465-7166

- Trans Union Toll Free 1-866-525-0262

Each credit bureau requires similar information: social insurance number, date of birth, address (including postal code), credit card number (even if it is no longer active).

Estimated Waiting Period: You would typically receive your credit report within one to two weeks.

Mail or Fax

This is the other free method. Mail and fax are technologies that may seem old fashioned, but they are still effective. You can complete the credit request forms for Equifax and TransUnion and then submit by mail or fax.

Equifax:

National Consumer Relations

P.O. Box 190, Station Jean-Talon

Montreal, Quebec

Fax: 514-355-8502

TransUnion

Consumer Relations Centre

PO Box 338 LCD1

Hamilton, Ontario L8L 7W2

Turnaround time is typically one to two weeks.

What If I Find An Error On My Credit Report?

Credit bureaus get their information from various creditors and sometimes mistakes are made in both reporting and recording. If you do find errors, it is important to get these mistakes corrected as soon as possible. You can follow the links to the dispute resolution procedures for Equifax and TransUnion. You will need to provide proof of the error and will need to be diligent in following up to ensure the issue is corrected.

If you have been bankrupt or filed a consumer proposal, the notice of your filing will be removed from your credit report after a certain period of time. If you believe your notice should be removed, use this dispute resolution process to contact the appropriate agency. Each bureau keeps records for a different length of time but generally the notice of your bankruptcy or proposal should be removed:

- A first bankruptcy will be removed after six to seven years following your discharge (depending on the credit bureau). This is extended to 14 years for a second bankruptcy.

- A consumer proposal will be removed from your credit report 3 years after all your payments have been completed.

Another common issue we see is that creditors will incorrectly report individual debts as ‘included in a bankruptcy’ when they may have been included in a consumer proposal. The correct legal proceeding is reported to the credit bureau by the Office of the Superintendent of bankruptcy and will appear in the legal section of your credit report. These debts should be purged from your report six years after the last activity. For some creditors this will be the last payment date, for others it may be the date of filing bankruptcy or a consumer proposal.

For more information on how to review your credit report try our Free Online Video Course on Rebuilding Credit. Get a step-by-step plan on how to manage your credit score, how to review your credit report and fix errors and discover what types of credit you need to rebuild credit.

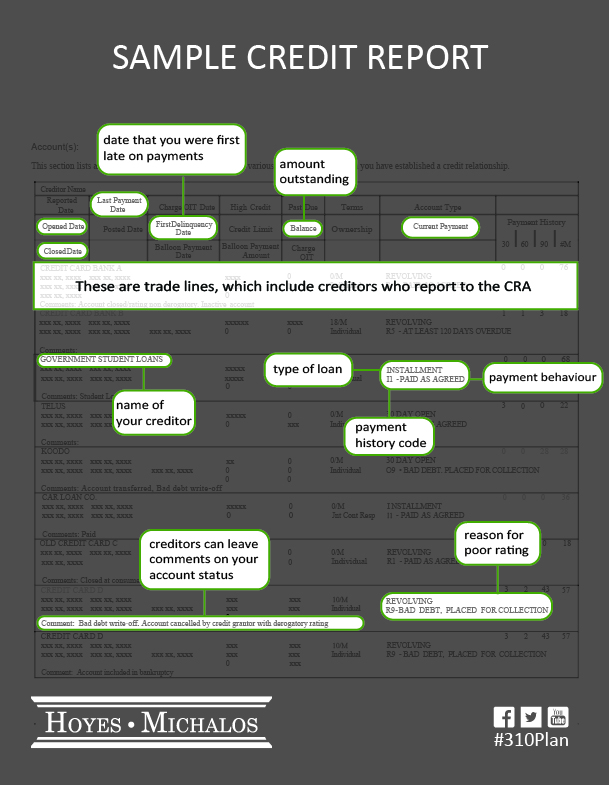

What Does A Credit Report Look Like?

Your free report won’t tell you your credit score. But since what you are doing at this stage is checking for inaccurate information, you don’t need your credit score.

Each creditor that reports to the credit reporting agencies will have their own line where they report on your payment history. These are called trade lines. Creditors will report your history with a letter followed by a number. The letters are loan codes and the numbers are payment history codes. Let’s decode them together:

Loan Codes

- I – Installment loan (repaid over time with a set number of scheduled payments e.g. car loan)

- O – Open credit (pre-approved loan amount that can be used repeatedly up to a limit, and paid back e.g. line of credit)

- R – Revolving credit (automatically renewed after debt is paid off e.g. credit cards)

- C – Sometimes used in place of revolving credit

- M – Mortgage loan

Payment History Codes

- 0 – Too new or approved, but not used

- 1 – Paid within 30 days or as agreed (on time)

- 2 – Late payment: one month behind

- 3 – Late payment: two months behind

- 4 – Late payment: three months behind

- 5 – Late payment: more than 30 months, but not yet rated “9”

- 7 – Making payments under a debt plan (could be a consolidation order, orderly payment of debts, consumer proposal or debt management plan)

- 8 – Repossession

- 9 – Written off as bad debt, sent to collection or bankruptcy

Your credit report will include your legal name, birth date, and a note about whether or not your social insurance number is on file. It will also include a list of all known addresses, employers, and phone numbers. All of these will be listed starting with your most recent, and ending with the oldest known entry.

Below is a sample of how your credit report from Trans Union will look.