A Canadian consumer proposal must be filed with a Consumer Proposal Administrator, who is also a Licensed Insolvency Trustee. No-one else can administer consumer proposals in Canada. Not a lawyer, not an accountant, and not a debt consultant.

Now that we have that out of the way, let’s move on to what a consumer proposal administrator does.

Table of Contents

What does the consumer proposal administrator do?

A consumer proposal is a legal debt settlement option filed under the Bankruptcy and Insolvency Act of Canada. That means that you receive all the creditor protection afforded in bankruptcy while avoiding declaring bankruptcy.

A consumer proposal administrator is a person licensed by the federal government to administer consumer proposals in Canada.

Your Consumer Proposal Administrator will:

- Conduct your initial assessment to help you determine if you qualify for a consumer proposal. Your trustee will ensure you meet the debt limit in a proposal, and review options like comparing the differences between bankruptcy and a consumer proposal, to help you decide if a consumer proposal is the right debt relief solution for you.

- Help you determine how much to offer to your creditors and handle any negotiations that are needed. An experienced administrator knows what different creditors are looking for and will make sure your proposal is acceptable to both you and your creditors.

- File the official paperwork with the Office of the Superintendent of Bankruptcy, which begins the consumer proposal process and provides your stay of proceedings.

- Communicate the terms of your proposal to your creditors by sending a copy of the document to each creditor. A consumer proposal is an arrangement made with your unsecured creditors. Secured creditors will be notified, but filing will not affect your mortgage or car loan if you choose to continue with those payments.

- Notify anyone necessary to ensure any wage garnishments and collection actions stop.

- Collects, records, and approves claim forms submitted by your creditors, used in the voting process in a consumer proposal and to determine the payout share for each creditor.

- 45 days after the filing of your proposal, your Consumer Proposal Administrator counts the votes received for and against your proposal.

- If a creditors’ meeting is called, the trustee will act as an administrator at the meeting and can help you negotiate additional payment terms if that is necessary.

- Once your proposal is approved, they complete all administration duties, including collecting payments, dealing with your creditors, arranging for your credit counselling sessions, and making payments to your creditors in settlement of your debts.

- Upon successful completion of your proposal, your Consumer Proposal Administrator will issue you a Certificate of Completion.

Most importantly, your Consumer Proposal Administrator will work with you to find a debt repayment plan that you can afford. After looking at your financial situation, they can help you decide if a consumer proposal is your best option. If it is, they will explain how a consumer proposal works and help you make an informed decision.

Licensed insolvency trustees

Licensed Insolvency Trustees act as consumer proposal administrators in a proposal. They are regulated by the Office of the Superintendent of Bankruptcy. This government agency enforces guidelines and rules about what a consumer proposal administrator can and cannot do and what their fees can be.

The options trustees offer, including a consumer proposal, are court-approved, so it will be binding on creditors and prevent legal action from being taken against you. If they cannot assist you, they can offer some advice on how to deal with your problem.

How are trustees paid in a proposal?

Consumer proposal administrators are paid by a tariff, with fees set by bankruptcy legislation. Fees are paid out of your agreed proposal payments. In effect, they are deducted from monies paid to the creditors. The administrator is paid 100% of the first $1,500 on receipts in the proposal (to cover administrative costs) and 20% of payments after that.

Who cannot administer consumer proposals?

I could stop there, but I know it’s still hard to verify who you may be working with when you approach someone for help with your debt. I say this because of all the ads I’m seeing on Facebook and Google today advertising what appears to be consumer proposals, aka government debt programs. It’s a topic I’ve ranted about before, but it bears repeating.

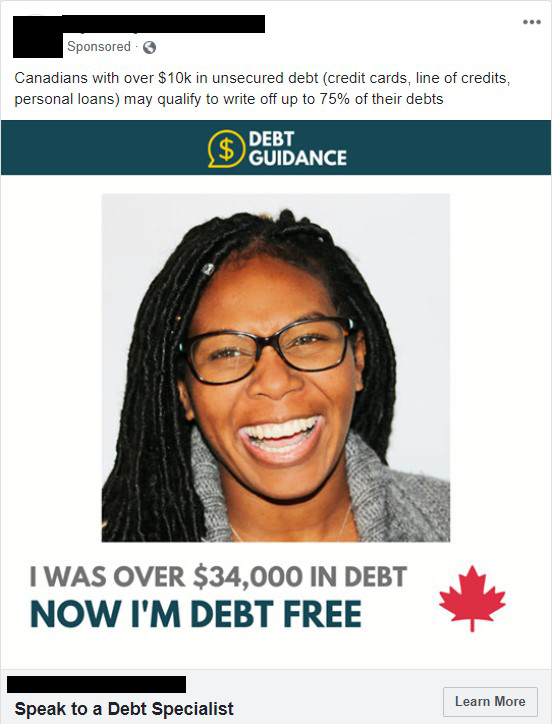

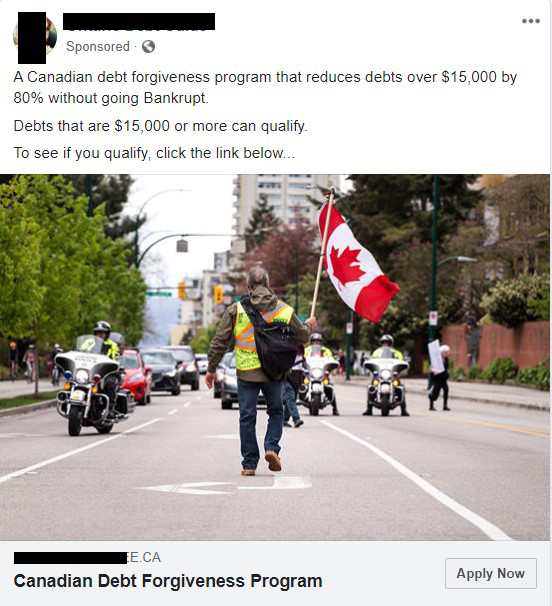

Here is a typical ad example:

Notice the heavy use of the Canadian flag, and words like Canadian debt forgiveness program, write off 70% or 80% of your debts but not much else about who they are. What they are really advertising is a consumer proposal.

Here is where you need to exercise some caution: most of these advertisers are not licensed debt professionals. Often in the footer you will read that they will refer you to someone else. The problem is, you as the consumer have no idea who is going to call you. It could be a Licensed Insolvency Trustee (who can do consumer proposals), or it could be a debt consultant or debt management company (who cannot).

So step number one when you get the call is to ask that question of the company that calls you. Is your company a Licensed Insolvency Trustee?

How to find a consumer proposal administrator

Back to the issue of advertising, and how to find help if you are facing severe financial problems.

It is important to note that you do not need a referral to see a Consumer Proposal Administrator. All reputable trustees offer a FREE, initial, no-obligation consultation.

Trustees are required to advertise and advise consumers that they are Licensed Insolvency Trustees or LITs. If you click through on an ad for debt help, you should see:

- The name of the company and their business logo

- The fact that they are Licensed Insolvency Trustees

- Look for legitimate reviews like Google Reviews from real people, not just text or fancy icons and badges

- Read the company about us page

- If you are not sure, look up the name of the firm on the OSB website. For example, here is the Hoyes Michalos listing of all our approved offices. Click on any office to see the name of the Licensed Insolvency Trustee authorized by the government for that location.

If you follow an ad that mentions a government program, reduce debts by 70% or 80% – be sure to check for the above signals that they are licensed to provide consumer proposal services. If all you see is a single page sales pitch, no mention that they are a licensed insolvency trustee firm, do more research.

Hoyes Michalos & Associates provides consumer proposal services in the following locations:

Other service areas

We offer the convenience of phone and video-conferencing services in the following additional locations: