UPDATE – Cash Store Financial Services Inc. Files for Bankruptcy Protection

The Cash Store’s problems continue, as they have now filed for bankruptcy protection (under the CCAA, a form of bankruptcy protection used by large corporations) and are likely to be delisted from the Toronto Stock Exchange.

On April 15, 2014, Regional Senior Justice Morawetz of the Superior Court of Justice—Ontario released his order granting Cash Store Financial Services Inc. protection under the Companies Creditors Arrangement Act, a form of bankruptcy protection for large companies.

The Cash Store will apparently “stay open for business,” but that will not include making loans in Ontario, which they are currently prevented from offering. The following is my original report on why Cash Store struggled under new payday loan restrictions.

Original Post – What happened?

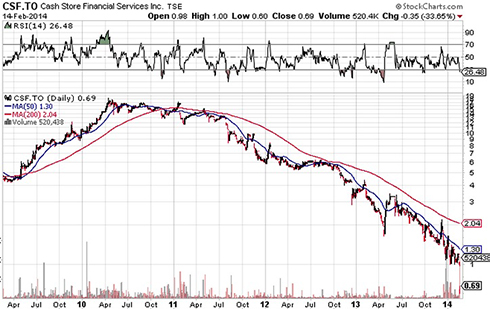

You don’t need to be a stock market analyst to understand the severity of Cash Store Financial Services Inc.’s current financial state. As you can see from the chart below, Cash Store shares have dropped from around $19 in early 2010 to a low of 60 cents on Friday. That’s a big drop.

The only payday loan lender listed on the Toronto Stock Exchange, the Cash Store operates 510 branches across Canada under the “Cash Store Financial” and “Instaloans” brands.

What happened?

Due to recent legislative changes, payday lending has become a less profitable business. Payday lenders are limited in what they can charge (no more than $21 for every $100 payday loan at the time, now $15 per $100) and are no longer permitted to continually “roll over” a loan, which happens when the borrower pays off one loan by taking out a new one.

Here’s the thing: if you want to make money as a payday lender, you need repeat customers. You won’t get rich on one $500 loan, but you can make a lot of money if you can loan $500 every payday. The borrower uses this week’s loan to pay off the loan he got last payday. Unfortunately for the Cash Store, if you can’t make new loans, your borrowers don’t have the money to pay off the old loans. Here’s what they said in their court documents:

“Since Cash Store is unable to make new loans in Ontario, its ability to collect outstanding customer accounts receivable has also been significantly impaired.”

Prior to filing bankruptcy, Cash Store began offering short-term lines of credit to counter this new legislation, hoping that these types of loans would not be subject to the payday loan rules. The Province of Ontario took a different position, however, claiming that despite the name change, debtors were effectively using these as payday loans.

The province of Ontario has been scrutinizing Cash Store Financial. This began with a charge and subsequent guilty plea by Cash Store to operating as payday lenders without a license in Ontario. Then, the province claimed that these new ‘lines of credit’ were effectively payday loans in disguise.

The Ontario Superior Court of Justice agreed with the Ministry of Consumer Services and in a ruling released on February 12 prohibited them from acting as a loan broker in respect of its basic line of credit product without a broker’s license under the Payday Loans Act, 2008 (the “Payday Loans Act”).

The Province took one step further by stating they want to deny new licenses to Cash Store Financial Services. According to a recent press release:

“the Registrar of the Ministry of Consumer Services in Ontario has issued a proposal to refuse to issue a license to the Company’s subsidiaries, The Cash Store Inc. and Instaloans Inc. under the Payday Loans Act, 2008 (the “Payday Loans Act”). The Payday Loans Act provides that applicants are entitled to a hearing before the License Appeal Tribunal in respect of a proposal by the Registrar to refuse to issue a license. The Cash Store Inc. and Instaloans Inc. will be requesting a hearing.”

It would appear that, for now, the Cash Store is not permitted to offer any payday loan or line of credit products in Ontario.

So what’s my take on this?

I am not a fan of payday loans. They are very expensive. Even with the new rules, a payday lender can still charge you $15 for every $100 you borrow, so over a two-week loan, that’s almost 390% in annual interest. From the debtor’s perspective, it’s very hard to generate enough cash to ever pay them off, so they end up borrowing and borrowing, and next thing you know they have four revolving payday loans (from four different lenders). This is why 40% of our client base owes at least one loan to a payday-style lender.

I’m pleased that the government is enforcing the rules, but I don’t think you need the government to protect you from payday lenders. You can protect yourself quite easily by following this one simple step: Never take out a payday loan.

If you have a short-term cash crunch, find alternatives to payday loans, like talking to your creditors about deferring your payment until the next payday; that’s a lot cheaper than paying 390% interest.

If you have more debts than you can handle and are already on the payday loan treadmill, call us immediately, and we’ll show you how to get help with payday loans and get off the payday loan hamster wheel.